Sector Landscape and Outlook

NZ’s financial system has been resilient and extends its support to households and businesses in managing their way through the pandemic. The banking system’s earnings have grown over the past year. Amid dividend restrictions and lower risk-weighted asset growth, has resulted a rise in banks’ capital ratios to their highest levels since the current risk-based approach to capital regulations was introduced. Banks are at decent position to fulfil higher requirements arising due to capital review, and to grasp any impacts from Alert Level restrictions that have been in place since August 2021.

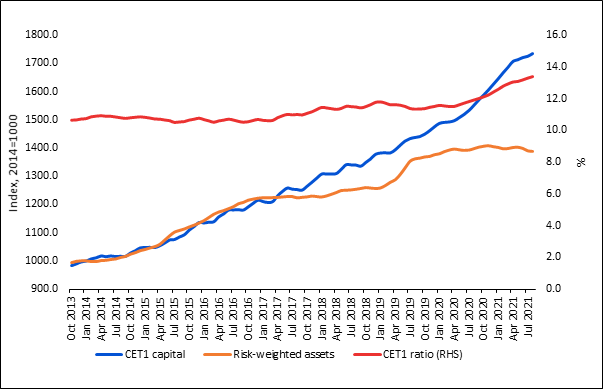

Robust Capital Buffer Sufficient to Meet Minimum Capital Requirement

As per the Reserve Bank of New Zealand (RBNZ), the banks in NZ have extended their capital buffers over the past six months, supported by moderate underlying profits and dividend restrictions that restricted payouts to shareholders. The rise has also been underpinned by reduced risk-weighted asset (RWA) growth primarily led by the decline in business lending. Higher capital ratios put banks in a stable position to strengthen the economy through a downturn. Also, the banks are well positioned to fulfil the new capital requirements arising from the Capital Review. If banks pay out only 50% of earnings as dividends, this will facilitate in capital requirements. However, higher profit retention may be required to meet minimums capital requirement in the final year.

Exhibit 1: Trend in Common Equity Tier 1 Capital of Locally Incorporated Banks in NZ

Data Source: This work is based on/includes rbnz data which are licensed by rbnz.govt for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

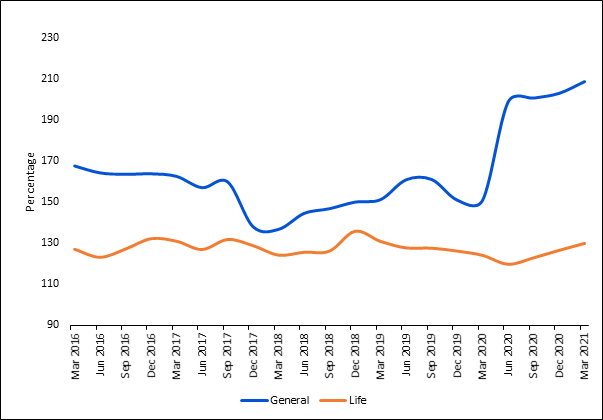

Insurers have Maintained Decent Capital in the Wake of Economic Uncertainty

As per RBNZ, general insurers account for the largest part of NZ’s insurance sector, comprising ~59% of total gross premium revenues, life insurers ~29%, and health insurers ~12%. The solvency ratio for general insurers grew materially during 2020 primarily led by dividend restrictions and remains higher in March 2021. This has also been strengthened by broadly stable earnings. By March 2021 only few insurers have been through a reporting cycle due to the relaxing of dividend restrictions. The solvency ratio for life insurers is less but has been more stable. The solvency ratio for health insurers continued above 300%.

Exhibit 2: Trend in Solvency Ratios of New Zealand Life and General Insurers

Data Source: This work is based on/includes rbnz data which are licensed by rbnz.govt for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

Stress Tests Indicates Improving Bank Resilience

The RBNZ conducted two complementary stress tests for retail banks. The Solvency Stress Test that tests the resilience of banks’ capital; and a Liquidity Stress Test that tests banks’ liquidity and funding resilience. The results of the regular Solvency Stress Test indicated that the New Zealand banking system has a sound level of resilience than a year ago, due to higher capital levels, and is well positioned to support the economy. The Liquidity Stress Test assessed the resilience of the 10 largest banks for unique liquidity shocks that cause in a phenomenal outflow of deposits and limits on access to market funding. The stress test was framed to test the extent of banks’ capacity to meet customer withdrawals under very severe assumptions.

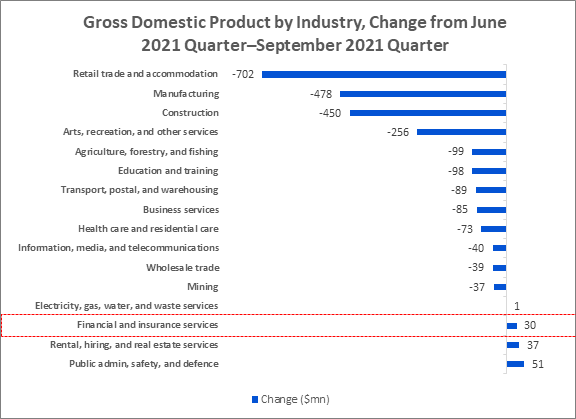

Positive Contribution by Financial & Insurance Services in September 2021 Quarter

As per Stats.NZ, economic activity decreased 3.7% in the September 2021 quarter as measured by GDP. This follows an increase of 2.4% in the June 2021 quarter. Average annual GDP increased 4.9% through the year to September 2021. Service industries decreased 2.7%, goods-producing industries decreased 7.3%, and primary industries decreased 3.1%. However, in value terms, the Financial and insurance services industry reported a growth of $30 million in the September 2021 quarter from the June 2021 quarter driven by the positive sentiments of the market participants.

Exhibit 3: Financial & Insurance Services Reported Growth in September 2021 Quarter GDP

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

Index Performance:

The S&P/NZX All Financials Index generated a 1-year return of ~26.05% versus ~-2.24% by the S&P/NZX 50 Index. Therefore, S&P/NZX All Financials Index overperformed S&P/NZX 50 Index by ~23.81% in 1-year.

Exhibit 4: S&P/NZX All Financials Index vs S&P/NZX 50 Index

Source: REFINITIV

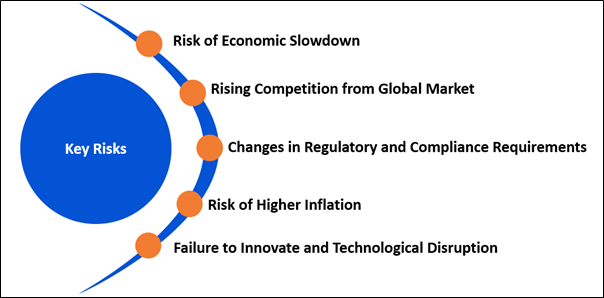

Key Risks and Challenges:

The international economy continues to face challenges due to COVID-19 related circumstances. Ongoing supply chain disruptions are creating additional costs for businesses, thereby resulting in higher inflation. Further, higher global interest rates could impact asset prices.

Robust demand for housing is resulting in price pressure. As a result, the buyers are borrowing more relative to their income. Loan-to-value ratio (LVR) restrictions are the crucial tool to address risks related to the housing market. Further, climate change indicates both long-term risks and opportunities to financial institutions. Therefore, gauging and managing climate-related circumstances is required to strengthen ongoing financial stability.

Exhibit 5. Key Risks in Financial Sector:

Sources: Analysis by Kalkine Group

Outlook:

The short-term outlook for global economic growth has deteriorated somewhat, primarily due to the spread of the Delta variant, rising energy prices, ongoing supply chain issues, and signs of a slowdown in the Chinese real estate market. Rising inflationary pressure is forcing some central banks to start gradually decreasing monetary stimulus, while others are looking current inflation levels as largely transitory and that current levels are needed to augment growth. Increasing public and corporate debt burdens will grow economies’ sensitivity to interest rates. In the recovery phase, as fiscal policy turns to supporting a resumption of economic activity, governments will be required to ensure that fiscal strategies are sustainable and growth enhancing.

Apart from the sector-specific factors, we have also analysed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

1) Westpac Banking Corporation (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$85.11 billion, Gross Dividend Yield: 5.982%)

Business Description:

Westpac Banking Corporation (NZX: WBC) is one of four major banking organizations in Australia and one of the largest banks in New Zealand. The company offers a spectrum of consumer, business, and institutional banking and wealth management services.

Outlook:

WBC continues to advance on its Fix, Simplify and Perform strategic priorities and is expected to lower its cost base in 2022 as it heads towards its $8 billion cost target from completion of programs under its Fix priority and realise the benefits from divestments. Further, the management forecasts loan growth to remain sound as the economy rebounds, while the net interest margins will be weighed down by the impact of low interest rates and competition. Besides, WBC has announced an off-market share buy-back of up to $3.5 billion, in order to return surplus capital and lower the number of shares outstanding.

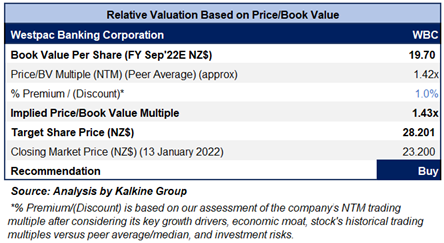

Valuation Methodology: Price/Book Value Based Relative Valuation (illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

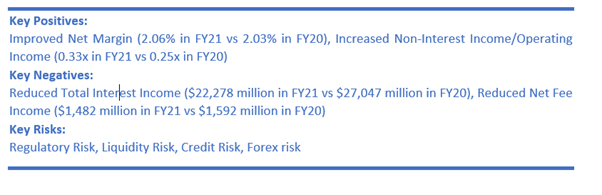

The stock has been valued using a P/BV multiple based illustrative relative valuation method. The target price so arrived reflects the potential rise of low double-digit (in percentage terms). As a result, the company might trade at a slight premium to its peers’ average, considering robust growth in cash earnings in FY21 as well as strong balance sheet and a better non-interest income/operating income at 0.33x in FY21 versus an industry median of 0.23x.

For the valuation purpose, we have taken peers such as National Australia Bank Ltd. (NAB.AX) and Commonwealth Bank of Australia (CBA.AX), to name a few.

Considering the facts above, we give a “Buy” recommendation on the stock at the closing market price of $23.20 per share as of 13 January 2022.

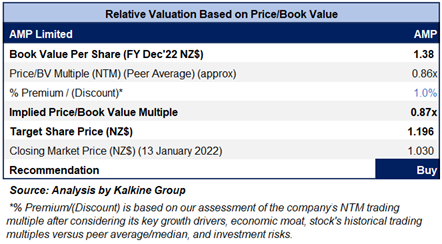

2) AMP Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$3.54 billion, Gross Dividend Yield: 0.00%)

Business Description:

AMP Ltd (NZX: AMP) is engaged in the wealth management business. Its business is bifurcated into three areas viz: AMP Australia (wealth management, advice, and bank), AMP Capital, and New Zealand wealth management services.

Outlook

AMP is witnessing certain positive signs of growth and innovation, mainly in its bank and platforms businesses where it is launching new services for its clients. The company’s demerger planning remains on track. It has charted a deadline to establish and separate the AMP Capital Private Markets business in FY21 and complete the demerger in H1FY22. Importantly, its plan is on track to deliver A$300 million annual run-rate cost savings by FY22. Further, the board follows a conservative method to capital management to assist the transformation of the business. Meanwhile, the company recently announced that it will delist from the New Zealand Exchange (NZX) Main Board and will remain in a sole listing on the Australian Securities Exchange (ASX) in February 2022.

Valuation Methodology: Price/Book Value Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using a P/BV multiple based illustrative relative valuation method. The target price so arrived reflects the potential rise of low double-digit (in percentage terms). As a result, the company might trade at a slight premium to its peers’ average, considering its resilient business performance in Q3FY21, cost reduction initiatives, and strong capital position.

For the valuation purpose, we have taken peers such as Westpac Banking Corp (WBC.NZ), Australia and New Zealand Banking Group Ltd (ANZ.NZ), to name a few.

Considering the facts above, we give a “Buy” recommendation on the stock at the closing market price of $1.03 per share, as of 13th January 2022.

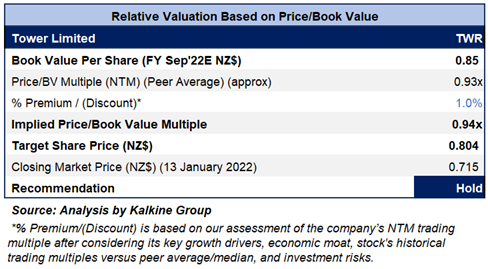

3) Tower Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$301.48 million, Gross Dividend Yield: 3.472%)

Business Description:

Tower Limited (NZX: TWR) is a New Zealand-based insurance company that operates across New Zealand and the Pacific Islands. It is engaged in providing insurance for houses, cars, content, businesses, and more.

Outlook

The company is well capitalised with a robust balance sheet and solvency margins. AMP remain focus on generating shareholder value through accelerating growth and innovation. Further, it sustains its investment in digital and data platform to drive efficiency and support growth. Meanwhile, the company expects to achieve underlying NPAT in the range of $21 million – $25 million in FY22 and has guided dividend of 5 cents per share.

Valuation Methodology: Price/Book Value Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using a P/BV multiple based illustrative relative valuation method. The target price so arrived reflects the potential rise of low double-digit (in percentage terms). As a result, the company might trade at a slight premium to its peers’ average, considering improved guidance for FY22 along with its robust capital position.

For the valuation purpose, we have taken peers such as Westpac Banking Corp (WBC.NZ), Suncorp Group Ltd. (SUN.AX), to name a few.

Considering the facts above along with current trading level, we give a “Hold” recommendation on the stock at the closing market price of $0.715 per share, down 0.69% as of 13th January 2022.

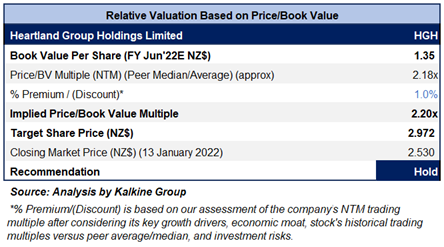

4) Heartland Group Holdings Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$1.49 billion, Gross Dividend Yield: 5.968%)

Business Description:

Heartland Group Holdings Limited (NZX: HGH) is a financial services group. In New Zealand, the group operates a bank and is registered as Heartland Bank Ltd, whereas in Australia it is a dedicated player in providing reverse mortgage loans and funding to partners in the small business and consumer lending sectors. In New Zealand, it focuses on only banking products across three key markets which include household, business, and rural.

Outlook

HGH’s board remains assured in the company’s ability of delivering robust growth and profitability driven by its strategy to provide frictionless service at the lower cost, thereby lowering the company’s cost to income ratio. Thereby, this will enable the company in passing the benefits t customers by way of lower pricing. The company forecasts its NPAT to remain between $93 million to $96 million in FY22. On 8 October 2021, Fitch Rating has affirmed the Long-Term Issuer Default Ratings (IDR) of HGH as well as Heartland Bank Limited (NZX: HBL) at 'BBB' and the Long-Term IDR of Heartland Australia Group Pty Ltd (Heartland Australia) at 'BBB-' with the outlooks remain Stable.

Valuation Methodology: Price/Book Value Based Relative Valuation (illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation:

The stock has been valued using a P/E multiple based illustrative relative valuation method. The target price so arrived reflects the potential rise of low double-digit (in percentage terms). As a result, the company might trade at a slight premium to its peers’ average, considering a higher net interest margin at 4.35% in FY21 versus an industry median of 2.05% and a higher pretax ROE at 16.2% in FY21 versus an industry median of 10.1%.

For the valuation purpose, we have taken peers such as Westpac Banking Corp (WBC.NZ), Commonwealth Bank of Australia (CBA.AX), to name a few.

Considering the facts above and the current trading level, we give a “Hold” recommendation on the stock at the closing market price of $2.53 per share, down 1.17% as of 13th January 2022.

.png)

Note 1: The reference data in this report has been partly sourced from REFINITIV.

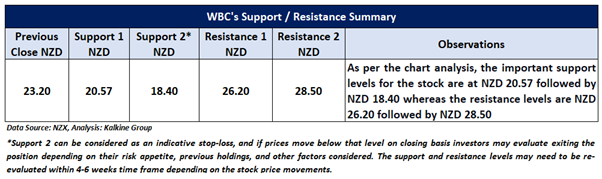

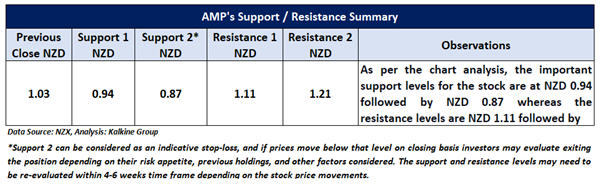

Note 2: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the analysis has been achieved and subject to the factors discussed above alongside support levels provided.

Technical Indicators Defined: -

Support: A level where-in the stock prices tend to find support if they are falling, and downtrend may take a pause backed by demand or buying interest.

Resistance: A level where-in the stock prices tend to find resistance when they are rising, and uptrend may take a pause due to profit booking or selling interest.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is authorised to provide general advice only. The information on this website does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...