1. Sector Landscape and Outlook

As per Situation and Outlook for Primary Industries, presented by the Ministry of Primary Industry indicates, export revenue for the food and fibre exports is expected to reach $49.1 billion in FY22, led primarily by robust demand for dairy, forestry, and horticulture products. The growth momentum is expected to continue year on year which will drive export revenues to reach $53.1 billion by FY25. Overall export revenue for the current year ended June 2021 continued to be strong, with the only decline of 1.1% forecast. This has been driven by strong farmgate milk prices, elevated avocado and kiwifruit crops, and higher Chinese demand for logs. This indicates a remarkable result despite challenges due to COVID-19 and is a testament to the sector’s ongoing resilience.

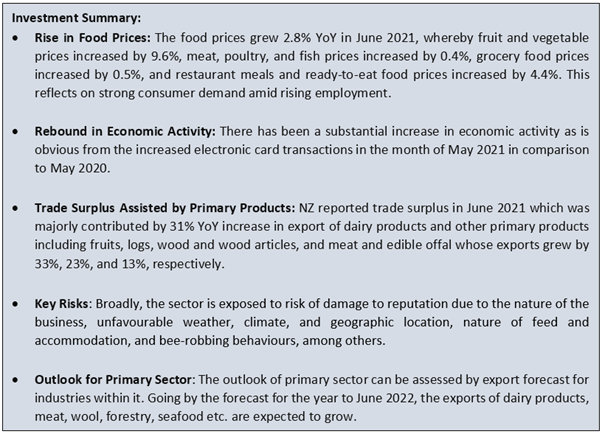

The Food Price Index Continue to Increase in June 2021

As per Stats.NZ, the food prices grew 1.4% in June 2021, where fruit and vegetable prices increased 9.4% (up 7.3% after seasonal adjustment), followed by meat, poultry, and fish prices that increased 1.0%. Further, grocery food prices grew 0.1% (up 0.1% after seasonal adjustment) and restaurant meals and ready-to-eat food prices increased 0.4%. However, non-alcoholic beverage prices decreased 0.7%.

Meanwhile, the food prices grew 2.8% in the year ended June 2021, where fruit and vegetable prices grew 9.6%, followed by restaurant meals and ready-to-eat food prices that grew 4.4%. Further, the non-alcoholic beverage prices grew 0.7%, grocery food prices rose 0.5%, and meat, poultry, and fish prices rose 0.4%.

Exhibit 1: Monthly Index Points Contribution to Food Price Index

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

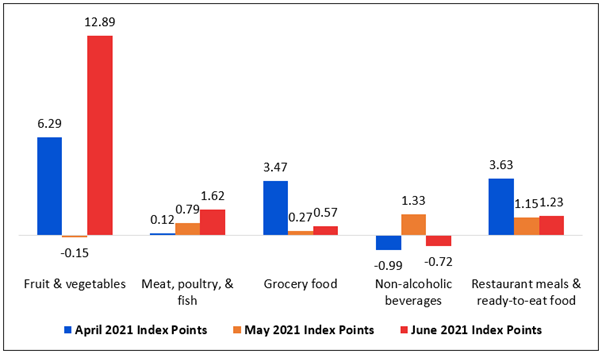

Rise in Electronic Card Transactions in May 2021

As per Stats.NZ, the electronic card transactions series includes all debit, credit, and charge card transactions with New Zealand-based merchants. This measure could be used to understand the changing pattern in consumer spending and economic activity. For the month of May 2021 over April 2021 indicates that spending in the retail industries increased 1.7% ($103 million) and spending in the core retail industries increased 1.8% ($95 million).

Meanwhile, the card transactions for May 2021 versus May 2020 indicates that specialized food rose $46 million (26%), and liquor rose $2.5 million (1.5%), while supermarket and grocery stores fell $86 million (4.4%). Meanwhile, food and beverage services increased $430 million (76%), and accommodation services increased $102 million (187%).

Therefore, it is indicated that the period witnessed a sharp rise in electronic card transactions growth across consumables sub-industry, durables sub-industry, hospitality sub-industry, and non-retail sub-industry. This could be attributed to low base effects as New Zealand was under alert level 3 and 2.

Exhibit 2: Change in Seasonally Adjusted Card Transaction Values by Industry ($m), MoM

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

Export of Milk Powder, Butter, and Cheese Led the Export Rise by Revenue in June 2021

As per Stats.NZ, goods exports increased $871 million or 17% YoY to $6.0 billion in June 2021, and goods imports increased $1.1 billion or 24% to $5.7 billion in June 2021. This resulted in a monthly trade balance surplus of $261 million. On June 2021 quarterly basis, goods exports increased 9.5% or $1.4 billion to $16.0 billion, and goods imports increased 5.6% or $875 million to $16.6 billion, resulting in a June 2021 quarterly trade deficit of $601 million.

Meanwhile, for exports in the June 2021 month, milk powder, butter, and cheese drove the rises in total export values, up $384 million or 31% YoY whereas preparations of milk, cereals, flour, and starch led the falls, decreased by $44 million or 23% YoY.

Exhibit 3: Overseas Merchandise Trade of June 2021

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

Index Performance:

The S&P/NZX All Consumer Staples Index generated a 5-years return of ~57.40% versus ~50.49% by the S&P/NZX All Index. Therefore, S&P/NZX All Consumer Staples Index overperformed S&P/NZX All Index by ~6.91% in 5 year.

Exhibit 4: S&P/NZX All Consumer Staples Index vs S&P/NZX All Index

Source: REFINITIV

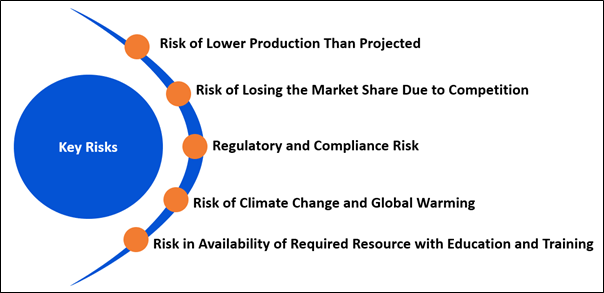

Key Risks and Challenges:

Dairy production could be impacted by the shortage of feed and fodder, breeding system, education and training, health and hygiene, marketing, and pricing of the product, among other factors. Further, the Global Dairy Trade Index is trading at 1,167 as of close 3 August 2021, which has come down from 1,346 as of close 2 March 2021.

This fall indicates that international dairy prices are trading lower driven by supply chain disruptions. We have the situation wherein governments becoming hesitant regarding opening borders amid spread of alfa variant of the pandemic. Besides, there has been change in consumption pattern as well largely impacted by decline in individuals’ earnings because of slowdown in economic activities. In addition, the movement in GDT index also indicates that there are high export push dairy products by exporting countries, led by a fall in internal sales, coupled with higher processing of less labour-intensive milk products, such as milk powders, to minimize the risk of labour shortages, also weighed on global milk prices.

Meanwhile, the bee colony losses in New Zealand continue to be below many international players. Key challenges faced by the industry include queen problems (like death, disappearance, or not laying eggs), management of the varroa mite, anticipated starvation of bees (due to weather and other causes), and wasps and other bee-robbing behaviours. Most of the losses are seen in winter because of lower nectar sources at this time of the year. Bees are primarily dependent on the stocks of honey they have collected in summer or supplementary feeding from beekeepers. These factors result in lower production of honey, thereby impacting the operations of the company.

Exhibit 5. Key Risks in Consumer Staples Sector:

Sources: Analysis by Kalkine Group

Outlook:

As per the Ministry of Primary Industries, the food and fibre sector has exhibited strong growth so far despite the challenges due to COVID-19 circumstances. Export revenue for the year ended June 2021 is expected to fall 1.1% to $47.5 billion. However, for the year ended June 2022, export revenue is expected to reach $49.1 billion as demand begins to pick up for main export market products and destination markets. Meanwhile, dairy export revenue is expected to rise by 7.2% to $20.4 billion, meat and wool export revenue is expected to rise by 0.4%, forestry export revenue is expected to grow to $6.4 billion, horticulture export revenue is expected to grow by 2%, and arable exports revenue is expected to grow by 3.7%. However, seafood export revenue is expected to grow with rising prices and mostly stable production. Besides, processed foods and other products is expected to decrease 2.6%.

As per the Ministry of Primary Industries, honey exports for the year to June 2022 are anticipated to drop to ~11,500 tonnes as international demand is expected to drop back from current very high levels.

Apart from the sector-specific factors, we have also analysed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

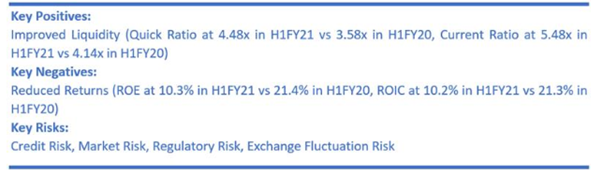

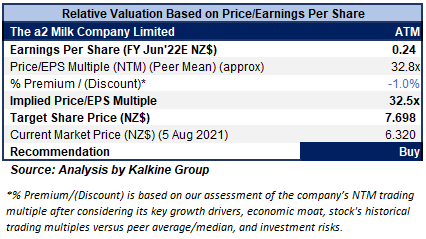

1) The a2 Milk Company Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$4.71 billion)

Business Description:

The a2 Milk Company Limited (NZX: ATM) improves the lives of its customers by providing the nutritional values of nature through the naturally occurring a2 MilkTM difference.

Outlook:

As per the outlook released on 10 May 2021, the management of the company is taking suitable action to address the elevated inventory imbalances to create a platform for future growth. In addition, it continues to invest in the brand and plans to further boost the level of marketing in Q4FY21 and into FY22. Moreover, it is targeting revenue for FY21 in the range of $1.20-$1.25 billion and EBITDA to sales margin for FY21 in the range of 11%-12% (excluding MVM transaction costs).

As per the release dated 30 July 2021, the company confirms the acquisition of 75% interest in Mataura Valley Milk (MVM), for total consideration of NZ$268.5 million. The acquisition has been funded through the existing cash reserves of the company.

Valuation Methodology: Price/Earnings per Share Based Relative Valuation (Illustrative)

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

We have applied P/E based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied a slight discount to P/E Multiple (NTM) (Peer Average) as the trading dynamics in the China infant nutrition market are under pressure for a2MC and many international competitors. Further, the level of channel inventory is higher than previously anticipated.

For the purposes of relative valuation, we have taken peers such as Synlait Milk Ltd. (SML.NZ), Sanford Ltd. (SAN.NZ), Murray Cod Australia Ltd. (MCA.AX), to name a few.

Considering the aforesaid facts, we give a “Buy” recommendation on the stock at the current market price of $6.32 per share, (New Zealand Time: 1:53 PM (GMT +12) on 5th August 2021.

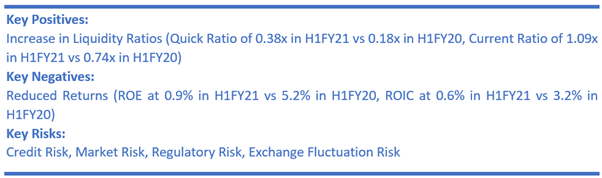

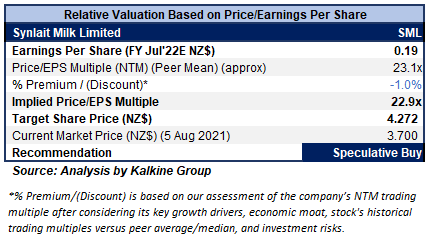

2) Synlait Milk Limited (Recommendation: Speculative Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$808.75 million)

Business Description:

Synlait Milk Limited (NZX: SML) is a producer and seller of nutritional milk products for its global customers by combining expert farming with state-of-the-art processing.

Outlook

As per the release dated 30 July 2021, the company has agreed terms to refinance its maturing syndicated banking facilities, with final documentation to be completed in coming weeks.

The company, on 31 May 2021, has raised its expected base milk price for the 2020-2021 season to $7.55 kgMS from $7.20 kgMS, driven by strong demand along with a relatively steady FX rate.

As per the revised guidance released on 24 May 2021, the company expects to post a net profit after tax loss in the range of $20-$30 million in FY21. The company has lowered its forecasts primarily due to prevailing shipping delays, prospects of attaining lower prices for ingredient products than earlier estimated, and a more conservative approach to year-end inventory volumes and valuation.

Valuation Methodology: Price/Earnings Per Share Multiple Based Relative Valuation (Illustrative)

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

We have valued the stock using a P/E multiple-based illustrative relative valuation and have arrived at a target price that reflects a rise of low double-digit (in % terms). We have assigned a slight discount to P/E Multiple (NTM) (Peer Average), considering the anticipation of ongoing shipping delays and elevated inventory levels.

For the purposes of valuation, we have taken peers such as The a2 Milk Company Ltd. (ATM.NZ), Sanford Ltd. (SAN.NZ) and Scales Corporation Ltd. (SCL.NZ) to name a few.

Considering the aforesaid facts, we give a “Speculative Buy” recommendation on the stock at the current market price of $3.7 per share, on 5th August 2021.

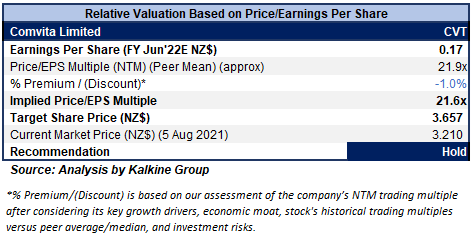

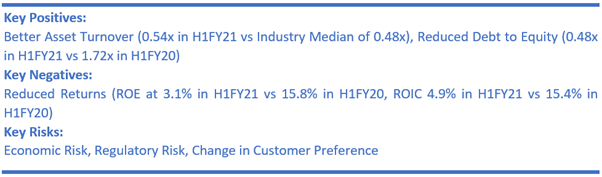

3) Comvita Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$226.37 million)

Business Description:

Comvita Limited (NZX: CVT) is one of the leading players globally in producing Manuka honey. The company has a wide geographical sales presence across Australia, New Zealand, China, and North America, among other countries.

Outlook

As per the full-year guidance released on 13 April 2021, the company expects operating EBITDA in the range of $22.5-$25.5 million in FY21 (the earlier guided range was $20-$23 million). The upgrade in earnings is mainly driven by continuing strong growth in its focused growth markets such as China and North America that offsets the challenges in ANZ and Hong Kong. Further, the benefits of strong performance in the digital channel, which currently contributes over 30% of CVT sales along with sustained efficiencies in production and better cost management are the reasons for the upgrade.

Moreover, as per the release dated 25 June 2021, the company’s total sales through the shopping festival in China increased +31.0% YOY indicating strong growth in consumer awareness and demand for CVT brand in the market.

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

We have valued the stock using P/E multiple-based illustrative relative valuation and have arrived at a target price that reflects a rise of low double-digit (in % terms). We have assigned a slight discount to P/E Multiple (NTM) (Peer Average) considering the challenges in ANZ and Hong Kong market and lower liquidity.

For the purposes of relative valuation, we have taken peers like Sanford Ltd. (SAN.NZ), The a2 Milk Company Ltd. (ATM.NZ), and New Zealand King Salmon Investments Ltd. (NZK.NZ).

Considering the aforesaid facts, we give a “Hold” recommendation on the stock at the current market price of $3.21 per share, (New Zealand Time: 12:40 PM (GMT +12) on 5th August 2021.

4) Allied Farmers Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$17.0 million, Gross Dividend Yield: 2.825%)

Business Description:

Allied Farmers Limited (NZX: ALF) operates through its subsidiary, NZ Farmers Livestock Ltd, Farmers Meat Export Ltd, and NZ Farmers Livestock Finance Ltd whereby its activities involve the sale of livestock agencies services, the procurement, and processing of calves, and livestock financing.

Outlook

As per the release dated 2 August 2021, the company stated that from New Zealand Rural Land Company Limited (NZL.NZX) a performance fee of $1.183 million has been calculated as payable to its manager, NZRLM for the period ending 30 June 2021. As per the management agreement, the performance fee is to be satisfied in NZL shares at the 30 June 2021 - Net Asset Value (NAV) of $1.3351 per share. The company confirms that the earnings (including the performance fee) from NZRLM for FY21 will be ~$1.1 million.

On 24 June 2021, the company announced that NZ Rural Land Management Limited Partnership (NZRLM) has decided to pay a cash dividend to its partners of $700k, of which $350k (50%) is payable to Allied Farmers. On 3 June 2021, the company stated that NZRLM considers that Allied Farmers’ attributable earnings from NZRLM is expected to be in the range of $500k-$600k pre-tax as at 30 June 2021.

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

Given the sustained focus on growth strategies towards improving and growing its existing business and the capital raised in the process, the company is well-positioned to tap further growth opportunities.

Thus, we give a “Hold” recommendation on the stock at the current market price of $0.590 per share, on 5th August 2021

Note 1: The reference data in this report has been partly sourced from REFINITIV.

Note 2: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the analysis has been achieved and subject to the factors discussed above alongside support levels provided.

Technical Indicators Defined: -

Support: A level where-in the stock prices tend to find support if they are falling, and downtrend may take a pause backed by demand or buying interest.

Resistance: A level where-in the stock prices tend to find resistance when they are rising, and uptrend may take a pause due to profit booking or selling interest.

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...