This report is an updated version of the report published on 16 June 2022 at 5:36 PM (GMT +12)

1. Sector Landscape and Outlook

As per the ‘Fortnightly Economic Update’ released by The Treasury Department of New Zealand, the economic activity in March 2022 indicates that the country realised a fall in exports and manufacturing while a rise in construction. Further, the OECD and World Bank downgraded their global projection for 2022 and 2023. Meanwhile, the direction of oil price, which is trading over ~US$100 per barrel, will direct the broad-based policy change by the government and subsequent impact on consumer spending. In the Wellbeing Budget 2022, the government allocated $11 million in operating costs for progress on a key recommendation from the Commerce Commission’s review of the grocery sector by eliminating barriers to new retailers entering the market.

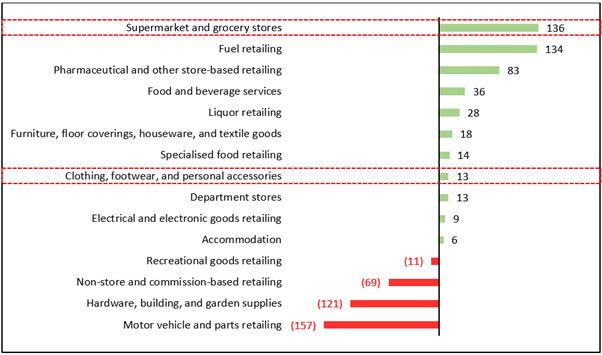

Rise in Retail Sales in March 2022 Quarter

As per Stats.NZ, the total value of retail sales increased 0.5% to $133 million, as 12 of the 16 regions indicated higher sales values in March 2022 quarter versus December 2021 quarter. The supermarket and grocery stores increased by 2.3% to $136 million, followed by fuel retailing, which grew by 5.8% to $134 million during the same period. The total value of the stock as of 31 March 2022 stood at $9.3 billion, up 12%, or $1 billion, versus March 2021. The highest rise came from hardware, building, and garden supplies, which increased by 26% ($304 million), followed by motor vehicle and parts retailing, which increased by 16% ($276 million).

Exhibit 1: Trend in Retail Sales Values by Industry from December 2021 Quarter to March 2022 Quarter (NZ$ billion)

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

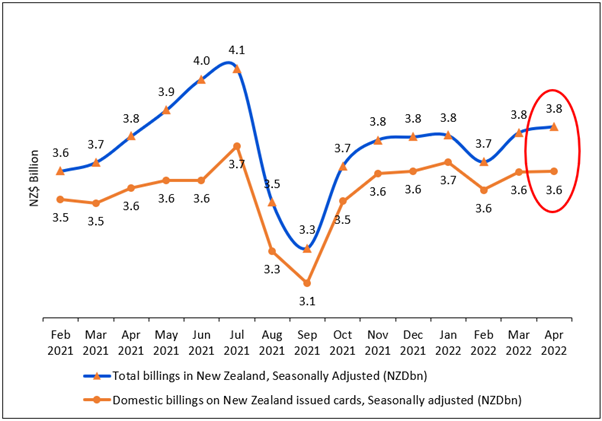

Continued Rise in Billing in April 2022

As per RBNZ, seasonally adjusted total billings in NZ stood at $3.8 billion in April 2022, up 0.7% MoM, and seasonally adjusted domestic billings on NZ issued cards stood at $3.6 billion, like in March 2022. Further, the overseas billings (actual) on NZ issued cards increased to $0.4 billion in April 2022, as overseas travel restrictions minimized while keeping COVID-19 norms under control. Seasonally adjusted total advances outstanding at the end of April 2022 stood at $5.8 billion, down 6.7% YoY from $6.2 billion. Moreover, total credit limits continued to slide to $21.4 billion (not seasonally adjusted), down 3.8% YoY. The weighted average interest rate on personal interest-bearing advances decreased from 18.4% in February 2022 to 18.3% in March 2022.

Exhibit 2: Trend in Total billings on NZ cards (Actual)

Data Source: This work is based on/includes rbnz data which are licensed by rbnz.govt for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

Rise in Retail Trade and Accommodation

As per Stats.NZ, total sales in retail trade and accommodation stood at $29 billion, up $133 million (0.55%) in March 2022 quarter from the December 2021 quarter. Actual purchases grew $2.2 billion (11%), and salaries and wages increased by $282 million (8.0%) in the March 2022 quarter versus March 2021 quarter. The sales movements for the industry were as follows: retail trade up $224 million (0.9%), and accommodation and food services grew by $33 million (0.9%).

Index Performance:

The S&P/NZX All Consumer Discretionary Index generated a 5-year return of ~40.96% versus ~3.66% by the S&P/NZX 50 Index. Therefore, S&P/NZX All Consumer Discretionary Index overperformed S&P/NZX 50 Index by ~37.30% in 5-year.

Exhibit 3: S&P/NZX All Consumer Discretionary Index vs S&P/NZX 50 Index

.png)

Source: REFINITIV

Key Risks and Challenges:

The retail and consumer market are exposed to intense competition due to the entry of e-commerce companies, new brands and stores, creating pressure on margins and rising working capital requirements to maintain the inventory level as per the need and season. Small start-ups compete with well-established players in terms of modern technology and highly skilled talent backed by government support, including tax incentives and progressive attitudes.

Exhibit 4. Key Risks in Consumer Discretionary Sector:

Source: Analysis by Kalkine Group

Outlook:

Multiline retail and speciality retail companies are shifting their focus toward online shopping due to rising competition and the convenience of shopping online. Though the percentage contribution from online sales is small, the pace of growth in online sales is higher than in-store sales. Consumer shopping behaviour could migrate to such an extent in the foreseeable future that most well-established players will benefit more from online shopping than physical presence of stores in malls and independent outlets. Innovation in tech-driven services at a competitive cost and new product launches (SKUs) would decide the market leaders, who would then determine the trends and market standards. The online sales of speciality food, groceries and liquor increased by 47% to $1.3 billion between 2019 and 2020, versus a rise in sector sales of 10%. Further, online consumers increased by 54% to 1.09 million, indicating a strengthening business line. Customers also completed over 41% of online transactions in 2020, and online basket size grew by 5%.

Apart from the sector-specific factors, we have also analysed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

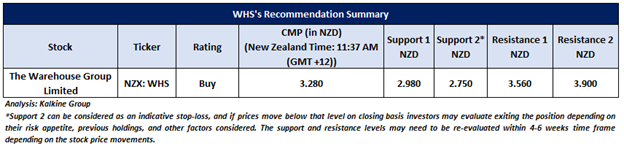

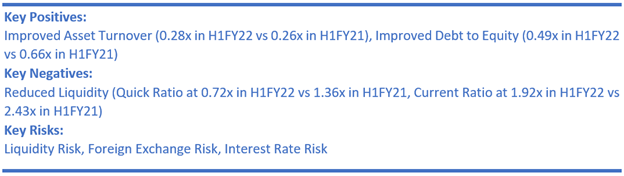

1) The Warehouse Group Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$1.15 billion, Gross Dividend Yield: 11.68%)

Business Description:

The Warehouse Group Limited (NZX: WHS) is one of the largest retailing groups in New Zealand. It consists of six core retail brands: The Warehouse, Warehouse Stationery, Noel Leeming, Torpedo7, 1-day and, TheMarket.

Outlook:

TheMarket.com platform stays on track to achieve over $100 million in Gross Transaction Value for FY22. Meanwhile, product supply concerns persisted in Q3FY22 due to continued challenges in the supply chain. While stock continued to flow, shipping costs stayed very high, and the company took longer than usual to move products to their shelf, which COVID-19-driven team member absences have added to some availability gaps in the store. Meanwhile, the company projects shipping schedules to remain under pressure for Q4FY22 and FY23.

The FY22 year-end results will be announced on 28 September 2022.

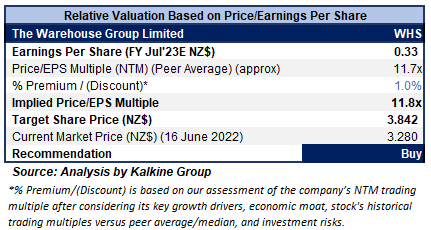

Valuation Methodology: Price/Earnings Per Share Multiple Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using P/E multiple-based illustrative relative valuation, and the target price so arrived reflects the potential rise of low double-digit (in % terms). A slight premium has been applied to P/E Multiple (NTM) (Peer Average), considering its acceleration in online sales, the uptick in gross margin in Q3FY22 and strong financial position.

Considering the facts above, we give a “Buy” recommendation on the stock at the current market price of $3.28 per share as of 16 June 2022 (New Zealand Time: 11:37 AM (GMT +12)).

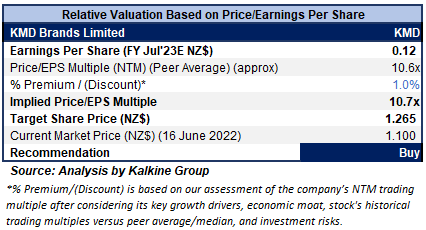

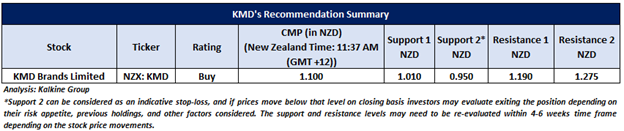

2) KMD Brands Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$794.08 million, Gross Dividend Yield: 5.505%)

Business Description:

KMD Brands Limited (NZX: KMD) is an outdoor, lifestyle and sports company with three well-established brands: Kathmandu, Rip Curl and Oboz and a solid international presence.

Outlook:

Despite the COVID-19 circumstances, the forward demand for its Rip Curl and Oboz products stayed at record levels and entered the traditionally strong winter season with all preparation. It will extend its investments in strengthening global brands in H2FY22 through Kathmandu online sites in Europe and Canada and the merging of Canada and UK fulfilment centres for all brands.

Besides, the company anticipates the gross margins in H2FY22 to remain in line with last year due to continued pressure on international freight costs and currency impacts. However, the company is well capitalised and invested in the long-term international expansion of its global house of brands.

Valuation Methodology: Price/Earnings Per Share Multiple Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using P/E multiple-based illustrative relative valuation and the target price so arrived reflects the potential rise of low double-digit (in % terms). A slight premium has been applied to P/E Multiple (NTM) (Peer Average), considering the positive rebound in Q2FY22, record-forward demand for its products, and strong balance sheet position.

Considering the facts above, we give a “Buy” recommendation on the stock at the current market price of $1.10 per share as of 16 June 2022 (New Zealand Time: 11:37 AM (GMT +12)).

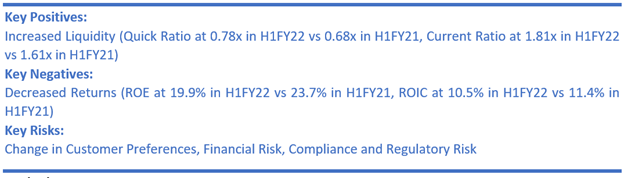

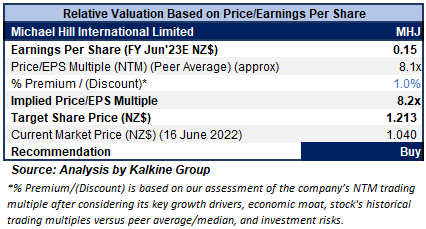

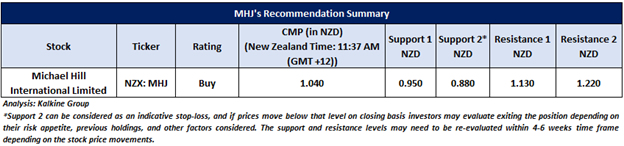

3) Michael Hill International Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$407.70 million, Gross Dividend Yield: 9.174%)

Business Description:

Michael Hill International Limited (NZX: MHJ) is an international retail jewellery company. The group operates through a network of stores spread globally across Australia, New Zealand, and Canada. The group has its global headquarters and wholesale and manufacturing divisions in Brisbane, Australia.

Outlook:

The company is focusing on its strategies to augment growth and margin by strengthening its brand, a members loyalty program, a push towards digital-first, and culture mechanisms. Also, the company is looking for new markets, new channels & new service propositions as well as cost management. In the first eight weeks of H2FY22, the same-store sales were flat, all store sales were up +14%, and the gross margin remained strong.

Valuation Methodology: Price/Earnings Per Share Multiple Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using P/E multiple-based illustrative relative valuation and the target price so arrived reflects the potential rise of low double-digit (in % terms). A slight premium has been applied to P/E Multiple (NTM) (Peer Average), considering the Q3FY22 solid results despite the significant disruption, healthy cash position and decent progress on its strategic priorities.

Considering the facts above, we give a “Buy” recommendation on the stock at the current market price of $1.04 per share as of 16 June 2022 (New Zealand Time: 11:37 AM (GMT +12)).

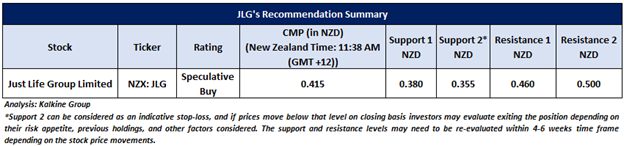

4) Just Life Group Limited (Recommendation: Speculative Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$41.39 million, Gross Dividend Yield: 8.130%)

Business Description:

Just Life Group Limited (NZX: JLG) provides drinking water, water coolers, and filters to homes, offices, and organisations throughout New Zealand. It is also a prominent player in supplying homes with natural lighting, heating, and ventilation products.

Outlook:

The company's focus continues to be on the business growth and dividend yield to investors and the organic and inorganic route for growth. Further, it continues to explore opportunities within its two strategic segments, Healthy Living and Healthy Homes. However, the company anticipates a challenging future due to COVID-19-related circumstances, and consumers would be more focused on their health and well-being.

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

Considering the facts above, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.415 per share as of 16 June 2022 (New Zealand Time: 11:38 AM (GMT +12)).

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and geopolitical tensions prevailing. Therefore, it is prudent to follow a cautious approach while investing.

Note 1: The reference data in this report has been partly sourced from REFINITIV.

Note 2: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the analysis has been achieved and subject to the factors discussed above alongside support levels provided.

Technical Indicators Defined: -

Support: A level where-in the stock prices tend to find support if they are falling, and downtrend may take a pause backed by demand or buying interest.

Resistance: A level where-in the stock prices tend to find resistance when they are rising, and uptrend may take a pause due to profit booking or selling interest.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is authorised to provide general advice only. The information on this website does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...