I. Sector Landscape and Outlook

The New Zealand Commerce Commission is doing a market study into the retail grocery sector to control the rising cost of groceries and make sure shoppers pay a reasonable price at the counter. In the year to September 2021, over $22 billion was spent at supermarkets and grocery stores. In the year to June 2019, food was the 2nd most significant expenditure for NZ households, with average spending of $234 a week on it.

Retail Spending Increased in December 2021 Quarter

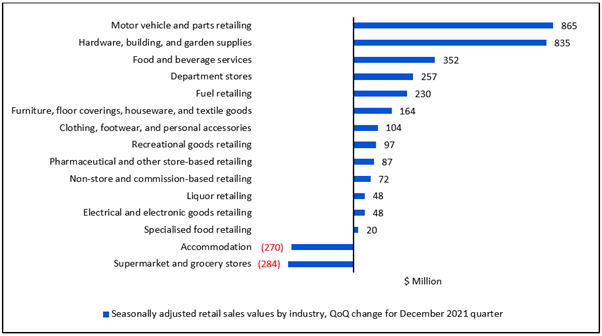

As per Stats.NZ's total retail sales volume increased 8.6%, total retail sales value (with price effects included) grew 10% ($2.6 billion), and 14 of the 16 regions indicated increased sales values for the December 2021 quarter versus September 2021 quarter. As per industry category, motor vehicle and parts retailing grew 24% ($865 million), hardware, building, and garden supplies increased 35% ($835 million), food and beverage services increased 13% ($352 million), and department stores grew 21% ($257 million).

Exhibit 1: Seasonally Adjusted Retail Sales Values, QoQ Change for December 2021 Quarter

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

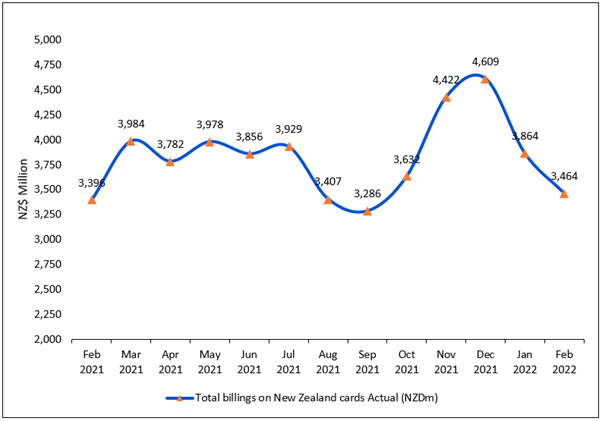

Rise in Total Billings of NZ Cards in February 2022 over February 2021

As per RBNZ, actual total billings in NZ stood at $3.5 billion during February 2022, up 2.0% YoY. The actual domestic billings on NZ issued cards were $3.2 billion, up 0.3% YoY, and actual overseas billings stood at $291 million, up 25.4% YoY.

However, on a month-on-month basis, the credit card billings in NZ fell in February 2022 as Omicron spread, and the downturn was similar to August 2021, at the time of Alert level 4 lockdown. Seasonally adjusted total advances outstanding at the end of February 2022 were $5.8 billion, down 0.9% from January 2022. Compared with one year ago, advances outstanding fell 6.5% from $6.2 billion. The weighted average interest rate effective on personal interest-bearing increased from 18.2% in December 2021 to 18.3% in January 2022, the highest effective rate since March 2009.

Exhibit 2: Trend in Total billings on New Zealand cards (Actual)

Data Source: This work is based on/includes rbnz data which are licensed by rbnz.govt for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

Investments Aimed at Creating Efficiencies Through the Supply Chain

As per Commerce Commission New Zealand, the markets have been more competitive recently, hence calling for innovations and investments to improve efficiency in the supply chain and other logistical aspects to benefit consumers. eStores Woolworths NZ is developing a new purpose-built 38,000 sqm lower North Island distribution centre. Foodstuffs NI has recently invested over $100 million to construct a 77,500 sqm central distribution centre in Auckland to stocks groceries for over 150 of its stores.

Index Performance:

The S&P/NZX All Consumer Discretionary Index generated a 5-year return of ~69.89% versus ~17.13% by the S&P/NZX 50 Index. Therefore, S&P/NZX All Consumer Discretionary Index overperformed S&P/NZX 50 Index by ~52.76% in 5-year.

Exhibit 3: S&P/NZX All Consumer Discretionary Index vs S&P/NZX 50 Index

Source: REFINITIV

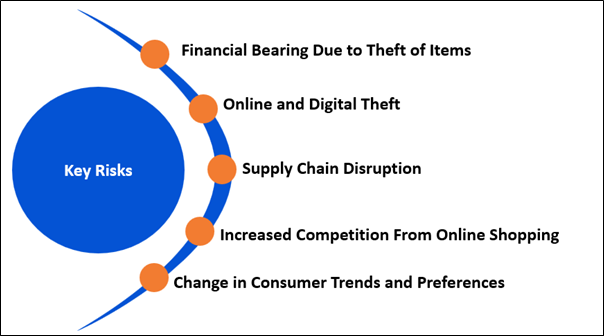

Key Risks and Challenges:

As per COMCOM, the retail market is open to an expected rise in prices in the future if some suppliers plan to exit the market, thereby decreasing competition between the remaining suppliers. Meanwhile, the consumers could benefit from private label products through reduced prices and multiple choice. This will favour private label products in the short term, but there is a risk that the rise of private labels could crowd out supplier branded products. This may lead to a loss of consumer choice and higher prices in the longer term.

Exhibit 4. Key Risks in Consumer Discretionary Sector:

Source: Analysis by Kalkine Group

Outlook:

Most NZ consumers purchase groceries at the retail grocery store. However, there has been a rise in online sales due to the COVID-19 pandemic. NZ Post reflected that online sales of speciality food, groceries and liquor grew by 47% to $1.3 billion between 2019 and 2020, versus a rise in sector sales of 10%. At the same time, the total number of online consumers rose significantly by 54% to 1.09 million. Customers also carried out over 41% of online transactions in 2020, and online basket size grew by 5%. The pandemic has changed consumer purchasing pattern, some permanently. The availability of e-commerce and hygiene consciousness is rising store switching behaviour, resulting in consumers shifting away from their primary store.

Apart from the sector-specific factors, we have also analysed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

1. Briscoe Group Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$1.29 billion, Gross Dividend Yield: 6.510%)

Business Description:

Briscoe Group Limited (NZX: BGP) acts as the holding company for its retail stores that operate within two retail sectors, namely, homeware and sporting goods, under different brand names viz; Briscoes Homeware, Living & Giving, and Rebel Sport.

Outlook:

The company sees a decrease in footfall across bricks and mortar networks. However, a significant rise in the mix of total sales is being filled by online sales. Further, the pandemic-related trading circumstances have invariably resulted in a strong recovery from pent-up consumers. Meanwhile, the company is extending the product range by introducing new online products shipped directly from suppliers, which has been introduced across 15 suppliers. The company is excited about the growth potential of this initiative and the opportunity to offer additional products not held in-store or part of its traditional range.

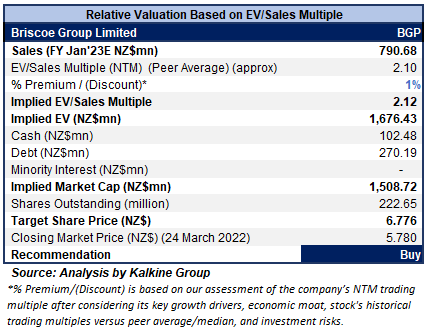

Valuation Methodology: EV/Sales Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using an EV/Sales multiple-based illustrative relative valuation and has arrived at a target price that reflects a rise of low double-digit (in % terms). A slight premium has been applied to EV/Sales Multiple (NTM) (Peer Average) considering its outstanding FY22 sales performance, robust financial performance despite Covid-19 related circumstances and strong outlook.

Considering the facts above, we give a “Buy” recommendation on the stock at the closing market price of $5.78 per share, up 0.35% as of 24th March 2022.

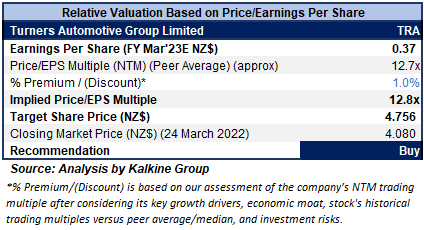

2. Turners Automotive Group Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$351.16 million, Gross Dividend Yield: 5.474%)

Business Description:

Turners Automotive Group Limited (NZX: TRA) was formed through the 2014 merger of NZ's largest vehicle and machinery retailer, Turners Auctions, and leading consumer finance and insurance business, Dorchester Pacific.

Outlook:

Amid strong Q1FY22, solid trading post L4 lockdown, and anticipation that L3/L2 restrictions will ease in the coming months, the company anticipates FY22 NPBT to be between $40-$42 million. Further, the company expects full-year fully imputed dividends of a minimum of 22 cents per share. Meanwhile, the company continues to develop a competitive moat through this time, positioning it for solid performance in FY23 and FY24. The conviction level for FY24 NPBT of $45 million is very high.

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using P/E multiple based relative valuation (on an illustrative basis), and the target price so arrived reflects a rise of lower double-digit (in % terms). Accordingly, a slight premium has been applied to P/E Multiple (NTM) (Peer Average), considering robust guidance for FY22 and significant financial performance in H1FY22.

Considering the facts above, we give a “Buy” recommendation on the stock at the closing market price of $4.08 per share, up 0.49% as of 24th March 2022.

3. Just Life Group Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$79.80 million, Gross Dividend Yield: 4.115%)

Business Description:

Just Life Group Limited (NZX: JLG) provides drinking water, water coolers, and filters to homes, offices, and organisations throughout New Zealand. It is also a prominent player in supplying natural lighting, heating, and ventilation products.

Outlook:

The company anticipates a challenging future ahead due to COVID-19 related circumstances. A positive point for the company is that the consumers are more focused on their health and wellbeing in this difficult time of uncertainty. The long-term intention remains to provide growth and dividend yield to investors, driven by organic growth and acquisitions. The company is systematically looking at opportunities in two strategic segments, Healthy Living and Healthy Homes, to expand further.

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

Considering the facts above, we give a “Hold” recommendation on the stock at the closing market price of $0.81 per share as of 24th March 2022.

4. NZ Automotive Investments Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$40.09 million, Gross Dividend Yield: 10.48%)

Business Description:

NZ Automotive Investments Limited (NZX: NZA) is an integrated used automotive group operating across NZ through 2 divisions: Automotive Retail and Vehicle Finance.

Outlook:

The company anticipates lower than expected revenue for FY22 due to decreased car, finance and insurance product sales in December 2021 and early January 2022. The underlying net profit after tax for FY22 is anticipated to be $2.3-$2.7 million, down on the prior comparative period of $3.8 million. The actual net profit after tax is projected to be $3.2-$3.6 million. The company remains in a strong financial position with cash balances of $5.8 million and net debt of $5.4 million as of 26 January 2022.

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

Considering the facts above, we give a “Hold” recommendation on the stock at the closing market price of $0.88 per share as of 24th March 2022.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and geopolitical tensions prevailing. Therefore, it is prudent to follow a cautious approach while investing.

Note 1: The reference data in this report has been partly sourced from REFINITIV.

Note 2: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the analysis has been achieved and subject to the factors discussed above alongside support levels provided.

Technical Indicators Defined: -

Support: A level where-in the stock prices tend to find support if they are falling, and downtrend may take a pause backed by demand or buying interest.

Resistance: A level where-in the stock prices tend to find resistance when they are rising, and uptrend may take a pause due to profit booking or selling interest.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is authorised to provide general advice only. The information on this website does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...