Summary:

Asset Management Companies, also known as AMCs, are companies that invest the funds collected from individual investors in different securities with the aim of best possible returns for the investors in exchange for a fee. AMCs maintain the range of portfolio by investing in both low-risk and high-risk securities like stock, debt, real estate, shares, bonds, etc.

Investing requires a lot of groundwork in terms of understanding the investment options available, determining their suitability for the needs of investors, and their value. It is not a one-time activity, but something that requires regular tracking, monitoring and suitable changes to the investment decisions based on socio-economic and political developments.

Steps in Investment Management:

Functioning of AMC: A Quick Look

An asset management company will collect funds from various investors that have different financial objectives. Now, it invests these large pool of funds in a very diversified portfolio and enjoys economies of scale, getting discounts on purchases. The return earned by the portfolio is then distributed among all the small retail investors.

In return, the AMC would charge a small fee called fund management fee. It is a key source of revenue generation for the AMC. A fund is expected to generate competitive returns in its category to maximize its subscribers and, hence, the revenues.

Investment Style

Overview of The Factors Affecting Investment

How Are the Funds Managed by an AMC?

Asset management companies follow a strict approach when it comes to the selection of stocks, and they make up the entire portfolio on the basis of the investment objective.

The asset manager creates a portfolio after doing proper analysis and research. It is the call of the asset manager in deciding which security to sell, buy or hold. The entire formation of a portfolio is only based on the market knowledge of professionals, research, and study.

The asset manager allocates the funds to different asset classes by conducting market research. For example, an equity-oriented fund would invest more than 70% in equity and rest in debt. On the other hand, a debt-oriented would invest just 20% in equity-oriented funds to keep the risk levels low. A balanced fund would end up with just 60% in equity and 40% in debt to balance out return and risk.

The performance of the fund depends upon the allocation done by the fund manager. Generally, asset management companies choose to diversify their portfolio so that a downturn in one sector could not impact the performance of the overall portfolio. If portfolio has performed well than the benchmark index, it is considered to be well performed.

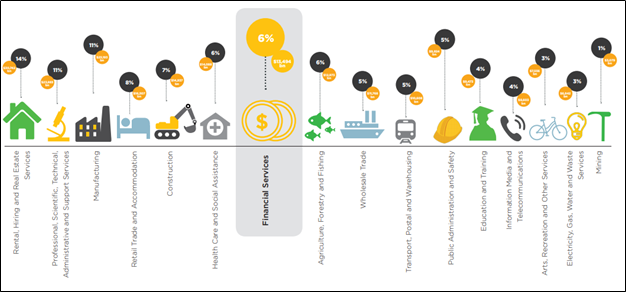

Contribution to GDP

Over the past 40 years, the rise in sector’s GDP makes the financial services industry the second fastest as well as the third largest contributor to the economic growth of NZ. In 2017, the Financial Services sector made the contribution of $13.5 billion into NZ’s economy, which represents 6% of the total GDP.

GDP Contribution in 2017 (Source: FSC)

Advantages in New Zealand

Over the last decade, New Zealand listed equity market has outperformed key global equity markets. This is mainly due to low interest rate environment and the yield offered by many of the larger stocks.

New Zealand debt markets have grown in depth, with corporate debt offerings well-subscribed. The total value of debt listed on the NZX Debt Market (NZDX) increased from $12.4 billion in January 2009 to $13.5 billion in October 2015.

Exposure Towards Defensive Industries

The outbreak of COVID-19 has impacted several sectors, and most of the companies have witnessed a halt in their core business activities. However, the impact has been tackled by some of the defensive industries. Investment management companies having exposure to defensive industries are expected to stay afloat amidst these uncertain circumstances. While the impact of COVID-19 was felt across sectors and industries, it can be said that the healthcare industry has managed to dodge the impact to some extent. Generally, defensive industries are strong enough to withstand macro-economic shocks.

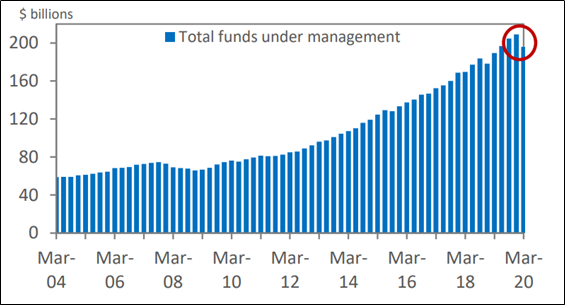

Current Statistics of Funds Under Management (FUM)

Total FUM witnessed a fall of 6.1 per cent in the quarter to 31st March 2020; however, there was a rise of 3.5 per cent over the year. This happens to be the biggest quarterly decline with respect to managed funds on record and followed financial markets decline amidst coronavirus. Quarterly fall was mainly because of coronavirus impacts on the financial markets globally. Notably, holdings of listed shares witnessed a fall of 17.1%. This was because international and local share markets encountered a sharp fall during March.

For the quarter ended 31 March 2020, KiwiSaver net assets fell $2.0 billion or 3.1 per cent to $63 billion, biggest quarterly drop on record. Other Superannuation witnessed a record decrease, declining $2.9 billion to $28 billion, a fall of 12.9% for the quarter.

Funds Under Management (Source: RBNZ)

Recovery of Broader Investment Management Industry Amidst COVID-19 Pandemic

Investment decisions are usually based on the intrinsic value of the share, which largely depends on the earning potential of the companies which in turn, depends on the quality of management and on economic activities that affect corporates profit and investors sentiment. The success of the economy leads to the success of overall markets. Without a positive and healthy economic environment, it would be difficult for the companies to expand their presence.

As the fall out of the COVID-19 outbreak, business conditions have become extremely challenging for many businesses.

The quality companies with strong industry positions, forming part of the core of the portfolio of investment companies would have been able to lessen the impact of the negative market. An astute investment manager may have continued to adjust the portfolio and would have taken advantage of the decline in share prices to increase holdings in companies he/she wanted to own more of.

The global share markets were on the track of strong year despite trade-war like situations and Brexit issue until the world was unexpectedly caught under COVID-19 virus in early 2020. Despite the significant decline in economic conditions, share markets across the globe have surged up, recovering almost all the losses it incurred during the decline. It has more to do with expansionary monetary and fiscal policies being pursued by the governments which created huge liquidity at the market place, finding their destination in equity markets.

The Road Ahead

The investment outlook remains unclear as companies face an extremely challenging operating environment. While expansionary policies have provided some breathing space for the economy, the investment environment is going to be largely dictated by the progress made on eliminating virus across the globe. As of now, valuations appear to be high, driven by low-interest rates and fiscal stimulus. Small number of stocks, particularly from information technology and healthcare, are driving these valuations. However, the full effect of COVID-19 on earnings and dividends are still to play out. Fund managers seem to be exercising caution at this stage while selecting securities and markets, and on being convinced of a sustainable recovery in the global economies, they will go all out for investing.

We expect a return to earnings growth in 2021 as central banks across the globe are expected to remain accommodative.

Challenges in Investment Management Industry

The COVID-19 pandemic has created significant volatility in the global stock markets. The impact was felt across asset classes and most of the corporate actions were either deferred or delayed. Halt on the economic activities have impacted the core business operations and some companies are uncertain about their outlook. Some investors have redeemed or reshuffled their holdings. Investment management companies having exposure to promising sectors and companies are expected to stay afloat.

However, the expectations of slowdown in the global economy and macro-economic challenges can affect the broader ecosystem.

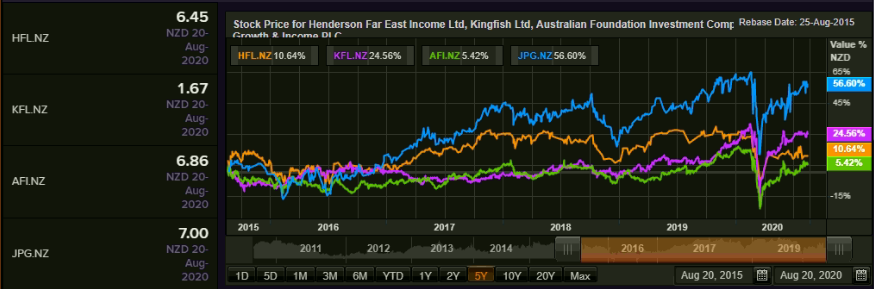

Since we now have a broad idea of the investment management sector, it is important to look at the performance of some companies operating in the same sector (HFL, KFL, AFI, JPG).

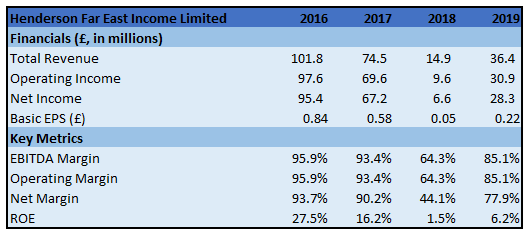

1. Henderson Far East Income Limited (NZX: HFL) (Recommendation: Buy, Potential Upside: Lower Double-Digit), (M-Cap: ~NZ$912.63 Mn, Gross Dividend Yield: 7.142%)

Business Description: Henderson Far East Income Limited aims to provide shareholders with a growing total annual dividend per share, as well as appreciation of capital with the help of a diversified portfolio of investments from the Asia Pacific region excluding Japan.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The company stated that monetary easing as well as rapid fiscal expansion is taking place as central banks are improving liquidity and they are limiting the damage. In the world of ultra-low interest rates, the case is robust for equity income investment and opportunity is being provided by Asia Pacific region.

Key Risks: The company is exposed to market risk, which arises from fluctuations in the market value of positions in a fund attributable to changes in market variables.

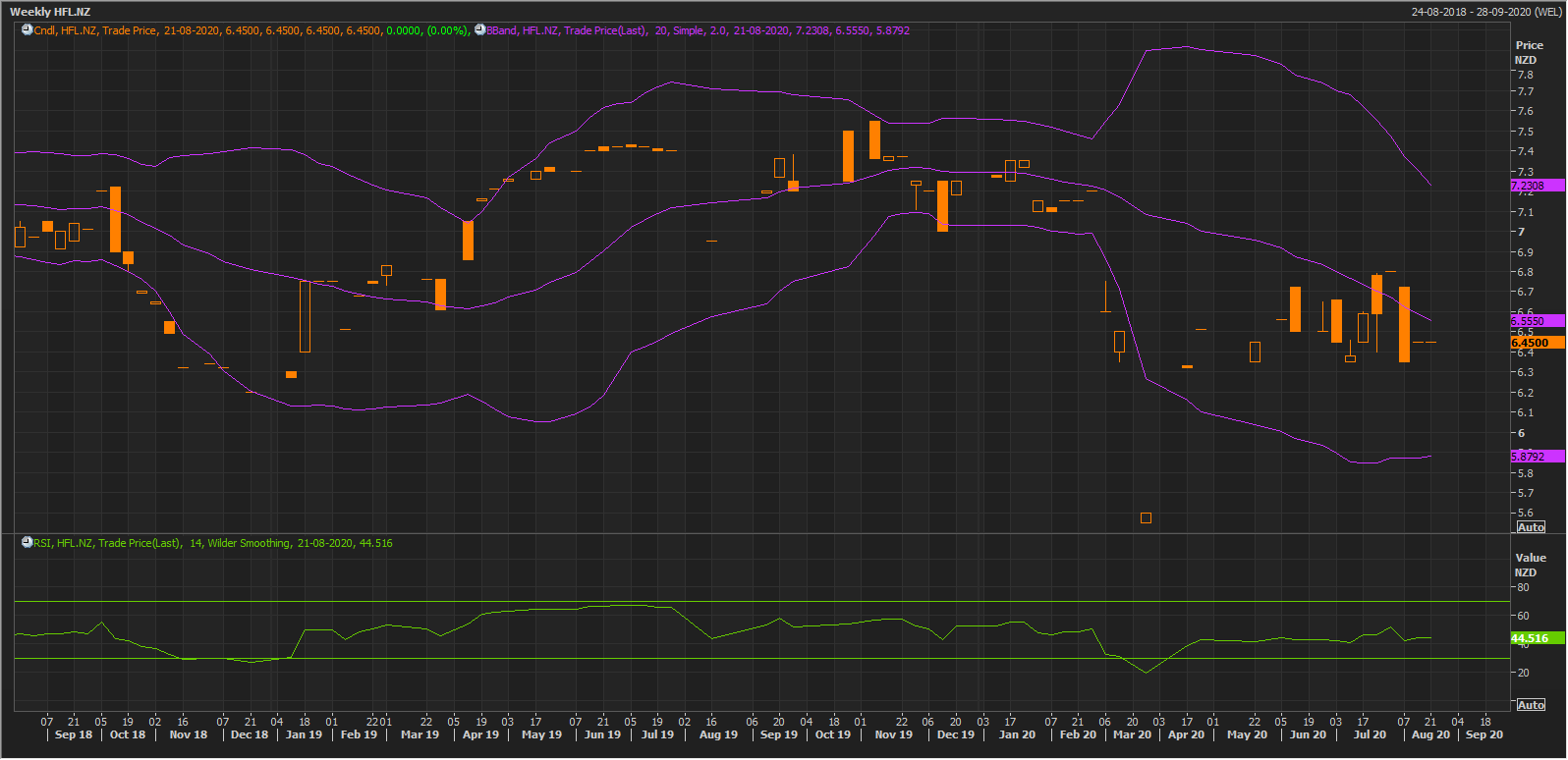

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands with upper band suggesting overbought status while lower band oversold status.

Having experienced sharp fall a week before the previous week, the stock has been giving ‘Four Price Doji’ close in the past two weeks including the on-going week. Since these charts formation are in the body of the bearish candle, it could be interpreted as ‘Bullish Harami’ chart pattern suggesting near-term bullish reversal for the stock. Technical indicator RSI with around 45 reading and curve at the end pointing up indicates at gaining of bullish momentum for the stock.

Going forward, the stock may have resistance around the previous high of $6.80 while support could be around $6.20.

Thus, we give a “Buy” recommendation at the current price of NZ$6.450 per share on August 20, 2020.

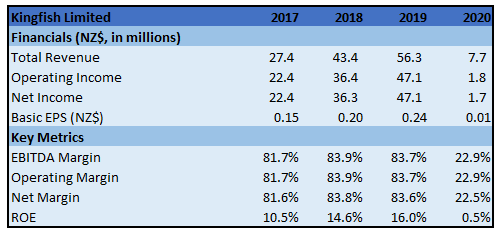

2. Kingfish Limited (NZX: KFL) (Recommendation: Hold, Potential Upside: Mid Single-Digit), (M-Cap: ~NZ$418.21 Mn, Gross Dividend Yield: 7.898%)

Business Description: Kingfish Limited happens to be a listed investment company based in NZ which invests in growing companies of NZ.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The company continues to favour quality stocks in its portfolio with long runways for growth irrespective of the short-term economic backdrop. Its largest positions are having long runways for growth through continuing to take market share as well as benefiting from long-term structural growth tailwinds. This could help it to bear the inevitable economic slowdown brought by coronavirus.

Key Risks: The company is exposed to various financial risks. These risks arise because of its investment activities, including market risk, liquidity risk as well as credit risk. All equity investments offer a risk of loss of capital, often because of the reasons beyond the company's control like competition, regulatory changes, commodity price changes as well as changes in general economic climates internationally and domestically.

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands with upper band suggesting overbought status while lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack.

The stock has given a very strong closing for the on-going week having closed around peak price and covering virtually all the losses of the previous week. Technical indicator RSI with 60 reading and curve at the end pointing up suggests strong bullish momentum for the stock.

Going forward, the stock may have resistance around $1.75 as has been provided by the upper Bollinger band while support could be around 20 periods SMA of $1.59.

Thus, we give a “Hold” recommendation at the current price of NZ$1.670 per share on August 20, 2020.

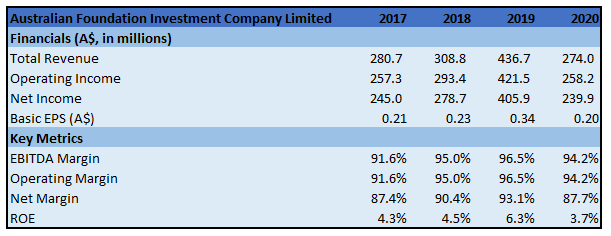

3. Australian Foundation Investment Company Limited (NZX: AFI) (Recommendation: Buy, Potential Upside: Lower Double-Digit), (M-Cap: ~NZ$8.30 Bn, Gross Dividend Yield: 3.741%)

Business Description: Australian Foundation Investment Company Limited is a listed investment company which invests in Australian and New Zealand equities. It seeks to deliver attractive investment returns to shareholders through access to a growing stream of fully franked dividends and growth in invested capital.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The outlook is still unclear as companies in the portfolio are still in an extremely difficult operating environment. While recent fiscal and monetary support has provided some breathing space for the economy, the environment would be largely influenced by the progress made on suppressing coronavirus in Australia as well as throughout the globe. However, the company believes that the portfolio is well-positioned to dodge further volatility, given the high-quality of companies.

Key Risks: The company can never be free of market risk as it invests its capital in securities which are not risk free.

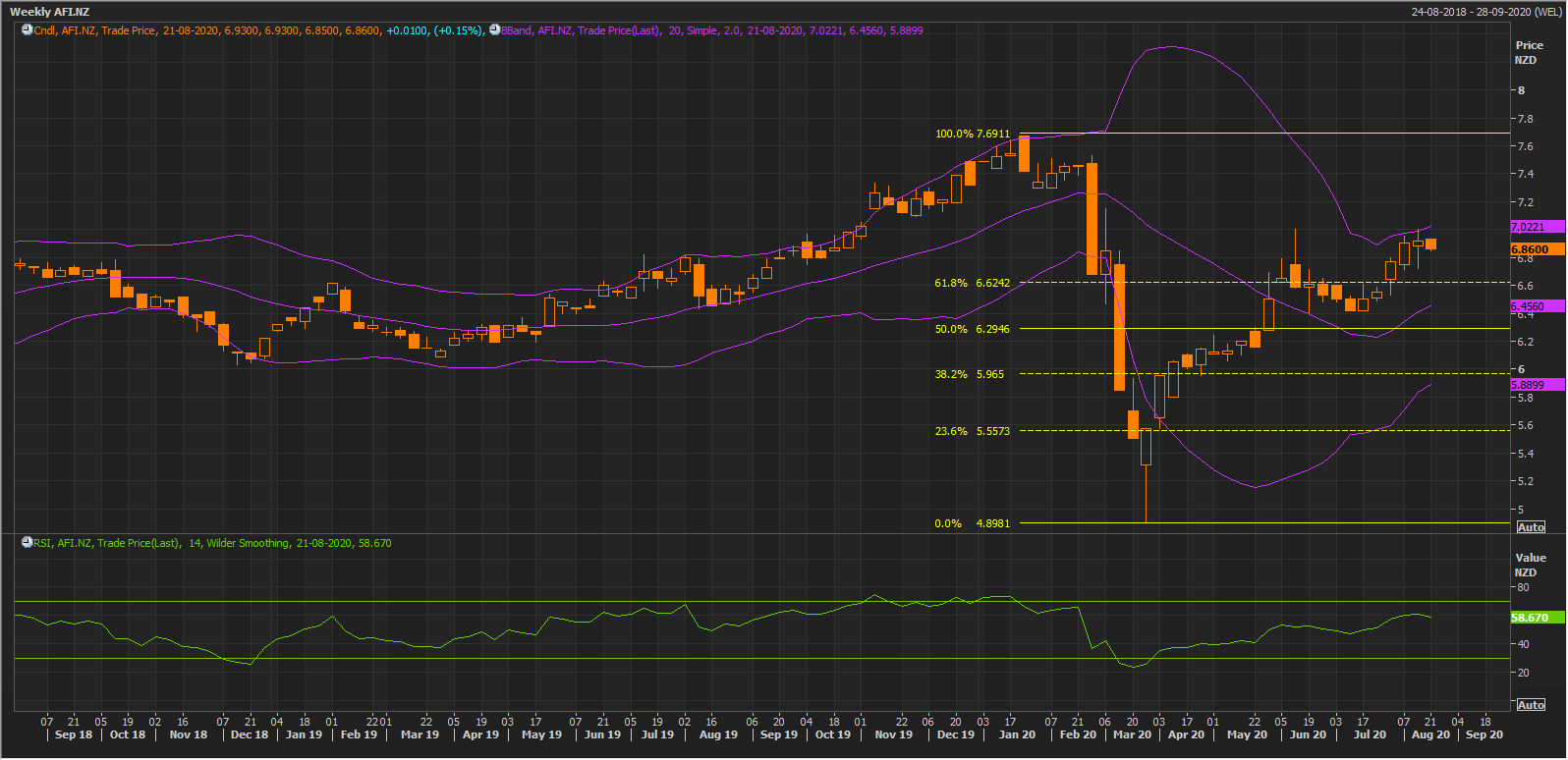

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands with upper band suggesting overbought status while lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack.

While remaining in an uptrend, the stock has given softer close for the on-going week at $6.85. Technical indicator RSI with 58 reading and curve at the end pointing down indicates at softening of bullish momentum for the stock.

Going forward, the stock may have $7.50 while support could be around 61.8% retracement level of $6.61.

Thus, we give a “Buy” recommendation at the current price of NZ$6.860 per share on August 20, 2020.

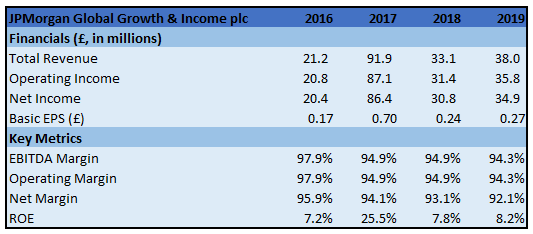

4. JPMorgan Global Growth & Income plc (NZX: JPG) (Recommendation: Hold, Potential Upside: Mid Single-Digit), (M-Cap: ~NZ$994.21 Mn, Gross Dividend Yield: 3.699%)

Business Description: JPMorgan Global Growth & Income plc focuses on making investments in the best ideas throughout the world’s stock market.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The company continues to focus its time on identifying great companies, which are expected to become great investments. The company sees opportunities in high-quality industrial companies, like Airbus and Norfolk Southern, as well as in semiconductor companies that could drive innovation.

Key Risks: Exchange rate changes can result in fluctuations in the value of underlying overseas investments. Investments in emerging markets involve a higher element of risk as a result of political as well as economic instability along with underdeveloped markets and systems.

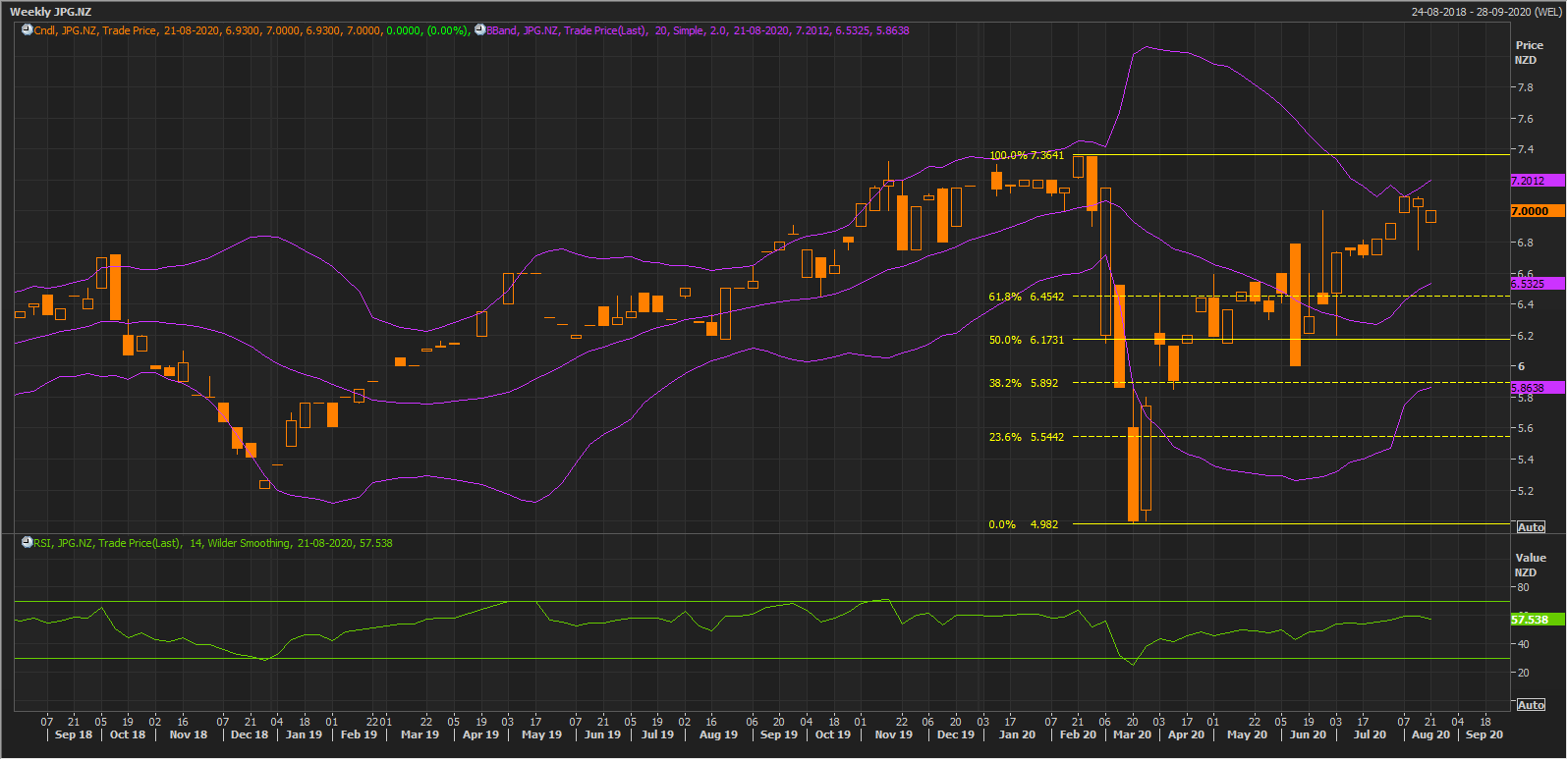

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands with upper band suggesting overbought status while lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack.

The previous week for the stock was very volatile but the closing was still higher meaning thereby that the bull is not ready to give up. In the on-going week also, the stock has given close at its peak price even though below the previous week closing, yet confirming bullish trend remains strong. Technical indicator RSI with around 58 reading suggests strong bullish momentum for the stock.

Going forward, the stock may have resistance around the previous high of $7.38 while support could be around $6.70.

Thus, we give a “Hold” recommendation at the current price of NZ$7.000 per share on August 20, 2020.

Comparative Price Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...