Company Overview: HUB24 Limited (ASX: HUB) provides investment and superannuation portfolio administration services, the provision of licensee services to financial advisers and software license and IT consulting services. The company reports its performance via Platform, Licensee, IT Services and corporate segments. The platform segment provides investment and superannuation services and Licensee provides financial advice to clients through advisers authorised by Paragem Pty Limited. IT Services include application and technology products and the Corporate segment supports these segments and allocates overhead headcount costs.

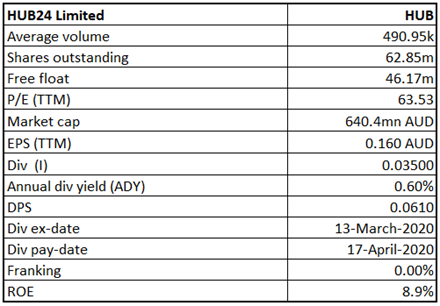

HUB Details

(16).png)

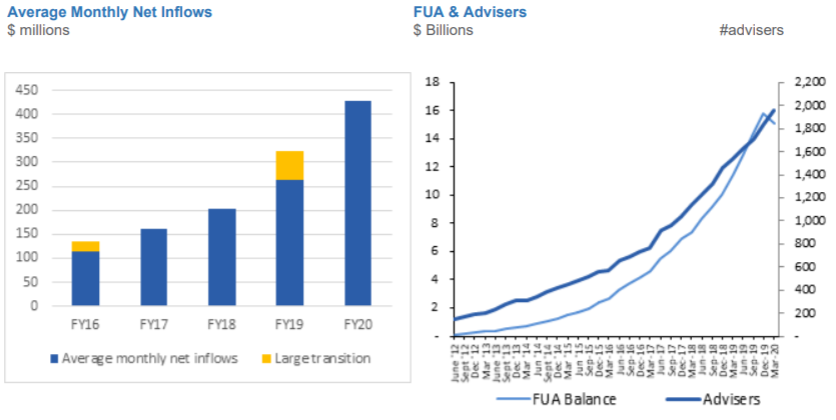

Strong Performance across Key Metrics and Growth in Market Share: HUB24 Limited (ASX: HUB) provides investment and superannuation portfolio administration services, the provision of licensee services to financial advisers and software license and IT consulting services. As on 16 June 2020, the market capitalization of the company stood at $640.4 million. The company marked another successful year with strong performance across key metrics, clear strategy, and industry-wide structure reform. The wealth management industry went through a significant change in the wake of the Financial Services Royal Commission because of which the company is seeing increased demand from customers. During FY19, revenue of the company went up by 13.4% to $98.7 million while group direct costs increased by only 2%. The company maintained its position as a market leader in the managed accounts segment with a growth of 54% in Funds Under Administration (FUA) to $12.9 billion, up from $8.3 billion at the end of the previous year, with record net inflows of $3.9 billion. In the same time span, EBITDA of the group increased by 30% to $14.8 million, with Underlying Net Profit After Tax up by 27% to $6.8 million.

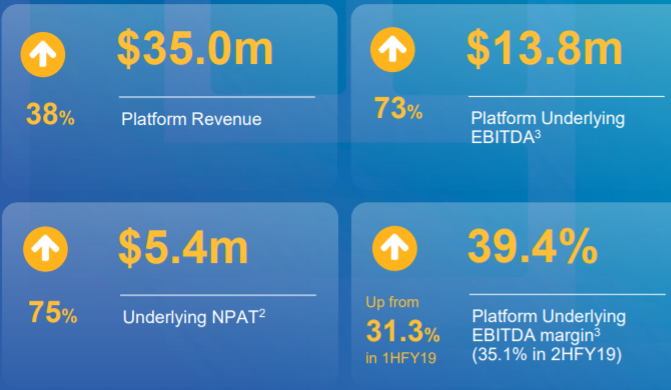

During 1H20, the company delivered on its strategy whilst maintaining momentum for growth. It delivered strong growth in Funds Under Administration with a continued increase in market share. During the half-year, group’s Underlying Net Profit After Tax stood at $5.4 million, up by 75% on 1HFY19 and underlying EBITDA of the company was $11.7 million, reflecting an increase of 71% on 1HFY19. In the same time span, it reported record net inflows from new and existing clients and increased market share to 1.6%. Strong growth and new business opportunities have been driven by HUB24’s market-leading technology, product leadership and customer focus.

HUB24 Limited seems well-positioned to leverage industry trends. Flexibility, connectivity and provider collaboration allow HUB to lead the development of new solutions & grow market share. The company is focused on converting new opportunities from the current strong pipeline and is aiming for continued strong financial results and unlock value for customers through technology and product innovation.

1H20 Financial Highlights (Source: Company Reports)

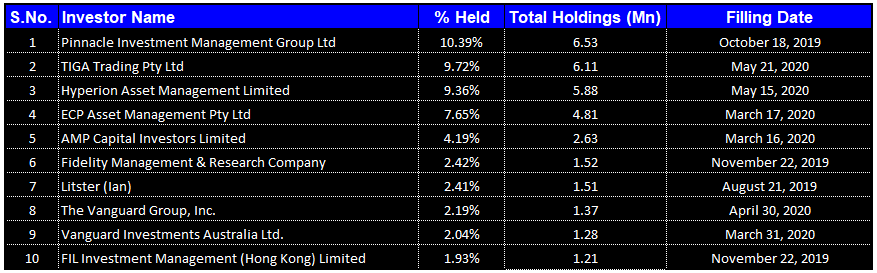

Details of Top 10 Shareholders: The following table provides an overview of the top 10 shareholders of HUB24 Limited. Pinnacle Investment Management Group Ltd is the largest shareholder in the company, with a percentage holding of 10.39%.

Top 10 Shareholders (Source: Refinitiv, Thomson Reuters)

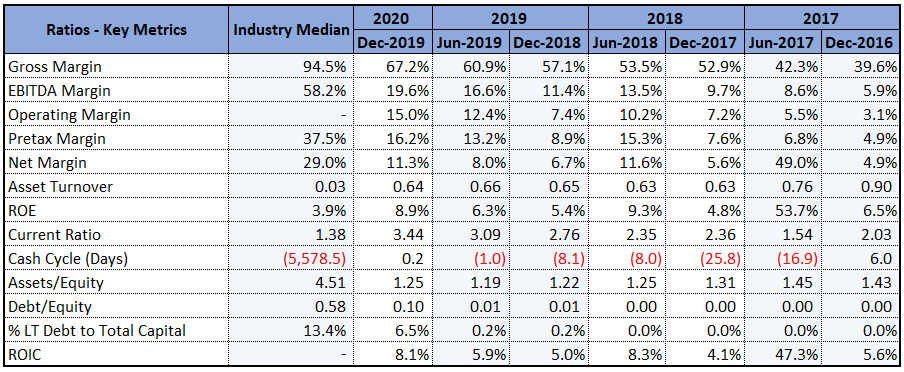

Well Management of Costs and Increasing Returns to Shareholders: During 1H20, gross margin of the company witnessed an improvement over the previous half and stood at 67.2%, up from 60.9% in 2H19. In the same time span, net margin of the company went up to 11.3% from 8% in 2H19. The improvement in the gross and net margin of the company indicates that the company is well managing the costs and is capable of converting its revenue into profits. During the half-year, the company reported higher profitability with an improvement in EBITDA margin to 19.6% from 16.6% in the previous half. In the same time span, Return on Equity of the company stood at 8.9%, higher than the industry median of 3.9%. This indicates that the company is well managing the capital of its shareholders and is capable of generating profits internally. During 1H20, current ratio of the company stood at 3.44x as compared to the industry median of 1.38x. This shows that the company retains ample liquidity to pay off its current liabilities using its current assets. In the same time span, Assets/Equity Ratio of the company was 1.25x, lower than the industry median of 4.51x and Debt/Equity Ratio of the company was 0.1x as compared to the industry median of 0.58x. This indicates that the business is financed with a significant proportion of investor funding and a small amount of debt, resulting in a financially stable balance sheet.

Key Margins (Source: Refinitiv, Thomson Reuters)

Quarterly Performance (For the Period Ended March 2020): During the quarter ended 31 March 2020, HUB continued to experience strong net inflows of $1.4 billion and a growth of 32% in Funds Under Administration to $15.1 billion. Net inflows for the March quarter have been driven by strong support from large national licensee and broker channels, as well as new business from boutiques and self-licensed advisers. The company continued to retain a strong pipeline of opportunities with a focus on adapting business models for the current environment. Despite the uncertainty prevailing in the financial markets, HUB24 has continued to maintain 2nd place ranking for both quarterly and annual net inflows and has increased its market share to 1.75% from 1.3% in the last quarter.

Quarterly Operational Highlights (Source: Company Reports)

Impact of COVID-19: Even though equity markets have been adversely impacted by the pandemic, HUB24 remains in a solid financial position. It continues to operate profitably with cash reserves significantly above regulatory capital requirements and generating strong operating cash flows. The group has no debt and has access to an undrawn working capital facility of $5 million. The company has activated the Business Continuity Plan. Revenue, on the other side, is likely to be impacted by the reduction in the official cash rate by the RBA. However, increasing transactional revenue, changes in portfolio asset composition, and the effect of tiered administration fees may soften the revenue and earnings impact.

Key Risks: Investment in HUB shares is subject to investment and other known and unknown risks. It might bear some credit risk if a counterparty fails to meet its contractual obligations given this uncertain environment. The group does not hold any credit derivatives to offset its credit exposure. The market volatility has significantly increased asset trading volumes and investors are advised to focus on the financial impacts arising from the pandemic.

Future Expectations and Growth Outlook: Despite challenging conditions for the market and advisers, HUB24 has mobilized and weathered out effectively. It is focused on delivering on strategic objectives and pursuing growth opportunities. The strategic initiatives of the company are progressing well, and the company is planning the FUA transition from ClearView Wealth Solutions wrap platform. HUB24 is in a strong position and has mobilized rapidly to deliver customers without interruption.

The company is likely to deliver higher shareholder value by accelerating growth in market share. It is converting new opportunities from the current strong pipeline and is expected to deliver benefits in the coming years. It is constantly innovating its capabilities and is creating solutions that enable licensee and adviser success. The company is targeting to achieve FUA in the range of $22 billion to $26 billion in FY21.

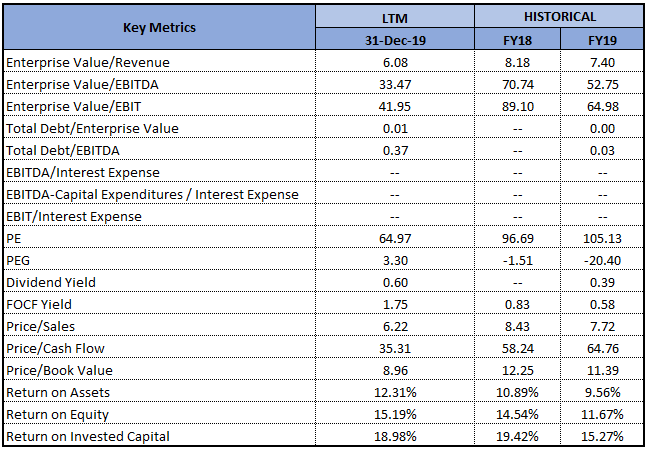

Key Valuation Metrics (Source: Refinitiv, Thomson Reuters)

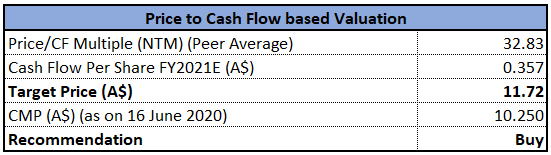

Valuation Methodology: Price to Cash Flow Multiple Based Relative Valuation (Illustrative)

Price to Cash Flow Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: HUB24 Limited maintained market-leading growth levels whilst other industry participants were impacted by structural change and softer market conditions due to the pandemic. The profitable trajectory of the company is likely to continue in the coming years and seems to be well-positioned to offer increasing returns. As per ASX, the stock of HUB gave a return of 59.22% in the past three months. We have valued the stock using the price to cash flow multiple based illustrative relative valuation approach and have arrived at a target price offering an upside of low double-digit (in percentage terms). For the said purposes, we have considered Netwealth Group Ltd (ASX: NWL), Pinnacle Investment Management Group Ltd (ASX: PNI), and Pendal Group Ltd (ASX: PDL) as peers. Considering the attractive returns in the past three months, resilience of the business amidst the global pandemic, decent financial performance, and positive long-term outlook, we recommend a ‘Buy’ rating on the stock at the current market price of $10.25, up by 0.589% on 16 June 2020..png)

HUB Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...