Hospitality industry has emerged as a key driver of growth in the service sector of New Zealand. According to Service IQ, strengthening economic activity together with buoyant outlook for business and household expenditure bode well for the broader food services sector in New Zealand. Higher disposable income acts as a primary growth driver for food and hospitality sector in New Zealand, and this is expected to be boosted by robust income from exports, stable industry dynamics, strong confidence of the consumers and overall growth of the economy.

Broader hospitality industry includes the tourism sector as well as food and services sector and increased growth of tourism might lead to elevated levels of growth rates for the hospitality sector moving forward. In one way, the industry is well-supported by domestic travel, immediately followed by international travel.

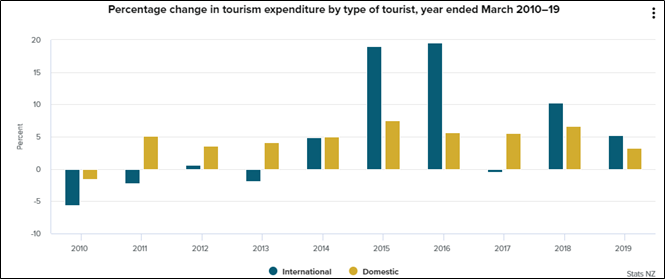

Key Data (Source: Ministry of Business, Innovation & Employment)

Global Footprint Might Support Hospitality Sector

According to the report by United States Department of Agriculture (October 2019), New Zealand offers a range of opportunities for the U.S. companies, and the country’s economic and investment environment is open as well as transparent, with strong trade and economic ties to the US.

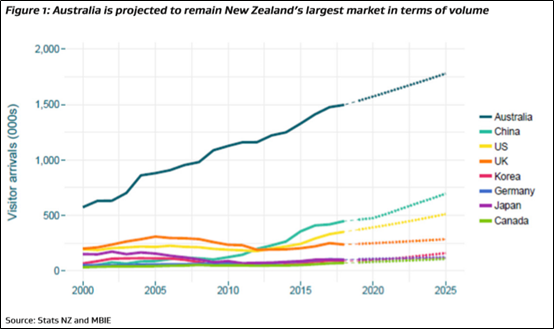

New Zealand Government has forecasted visitor arrivals to NZ to grow 4%-5% annually through to 2024. Australians make up the largest group of international visitors, and NZ has an estimated 1.5 million tourists visiting from Australia on the YoY basis to July 2019. Visitor numbers to June 2019 witnessed visitors from the U.S. up by 8.5%, visitors from Australia up by 4.1% and visitors from China down by 8.0%.

Expanding tourist base has been fuelling demand for a multitude of food as well as beverage products, and this is adding to the growth in food imports from the US.

International Visitor Spend to Reach $15 Billion by 2025- Opportunities for Hospitality Space

Total international spend is expected to reach $15.0 billion in 2025, up 34% from 2018, or 4.3% per year. Spending growth is forecast to grow at slightly higher than the growth of visitor numbers, suggesting that spend per visitor will increase. Australia is currently the largest market by spend, and will remain so, though Chinese spend will reduce the gap by 2025. Tourism contribution to GDP of $16.2 billion stood at 5.8% in 2019.

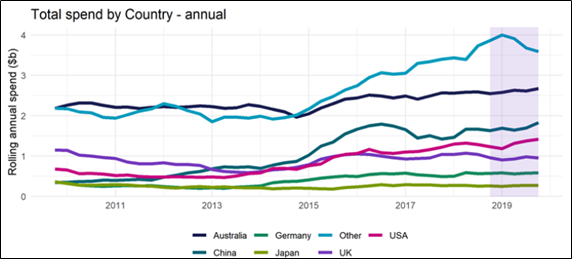

Total Spend (Source: International Visitor Survey, MBIE)

New Zealand possesses an established base of foodservice and hospitality sector, and the resilient nature of the industry might provide significant growth opportunities. Increased Government spending, infrastructure development, higher confidence of local people and stable income generation together with favourable Government policies are expected to boost the hospitality sector. According to the report by the United States Department of Agriculture, NZ possesses a comparative advantage when it comes to food production and manufacturing.

Key Risks Posed by COVID-19 & Strategies to Tackle Them

Tourism before COVID-19 was the largest export industry in New Zealand in terms of FX-earnings. But, with the outbreak of COVID-19, the industry received a severe setback. It has been subjected to several restrictions as the borders were sealed. Lockdown was imposed refraining non-essential business activities from operating. Under social distancing, all hotels, bars, and restaurants were closed. It resulted in about 30% reduction in employment across the hospitality sector. Due to drops in international visitors, coupled with the fact that for seven weeks, the hospitality industry experienced a loss of $40 million a day in revenue, many businesses are struggling to stay afloat.

However, the country has moved to Alert Level 1, which has widely been commended by hospitality industry. The industry for long been demanding removal of strict restrictions placed on it. Country transitioning to Alert Level-1 means that many hospitality operators can now begin operating. The industry has supported the Government’s ‘Smart Border’ concept as it will enable some international tourists to return and open-up opportunity for the hospitality and tourism industry. Moving forward, higher regulatory support and increased foreign exchange earnings might lead to an increase in spending towards infrastructure, resulting in higher income generation and increased contribution of the hospitality sector to the nation’s GDP.

Growth Drivers of Hospitality Sector in New Zealand

Market experts are of the view that increased demand, Government support, higher migration, wage, and employment growth are expected to keep the broader food and hospitality sector afloat moving forward. According to the international tourism forecasts, the visitor arrivals to New Zealand are expected to grow at an average of 4.0 percent each year, reaching 5.1 million visitors in 2025 from 3.9 million in 2018.

Contribution from Different Countries (Source: Ministry of Business, Innovation & Employment)

With the easing of restrictions and NZ moving to Alert Level-1, its now time to look at the companies in the food and hospitality space that could benefit (GSH, CGF, MOA, BFG)

1. Good Spirits Hospitality Limited (NZX: GSH) (Recommendation: Speculative Buy, Potential Upside: Lower Double-Digit) (M-cap: ~NZ$5.78 million)

Business Description: Good Spirits Hospitality Limited is a listed investment company that focusses on the hospitality sector.

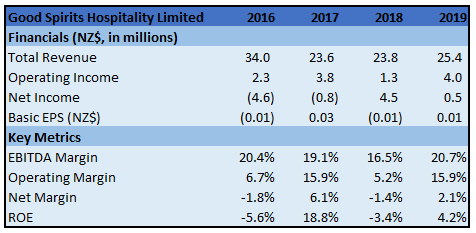

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The company has withdrawn its full year guidance due to the increased uncertainties around the duration and scale of the Covid-19 outbreak. GSH is taking various measures to mitigate the impact of Covid-19, such as managing employee expense ratios to revenues and reducing forward orders for particularly perishable food and beverages.

Valuation: GSH has advised that all venues (except DB Newmarket which would reopen on July 1, 2020) are opened and trading without the restrictions related to COVID19. This follows the announcement which was made by New Zealand Government to move to COVID-19 Alert Level 1. Since reopening under Alert Level 2, the company has witnessed a level of trade which has increased weekly since reopening, though has been limited by significant operating restrictions of Alert Level 2. On a positive note, the company expects further improved trading conditions under Alert Level 1.

On the TTM basis, EV/Sales multiple of GSH’s stock stood at 1.6x, which is lower than the industry median (investment banking and investment markets) of 5.0x. Its EV/EBITDA multiple stood at 6.7x as compared to the industry median of 8.6x. Therefore, it can be said that the company’s stock is slightly undervalued, and the current juncture provides a decent opportunity to make an entry.

Technical Analysis: The stock has shown resilience during the on-going week, having given bullish break-out and giving close at the peak price of $0.107 above 20 period SMA, reflecting strength in bullish trend. Momentum indicator RSI with 51 reading and curve at the end pointing up, support the strength in bullish trend for the stock. Going forward, the stock may maintain the existing resilience with likely resistance around $0.140 where gap on chart exists while support could be around the low price of the on-going week of $0.089.

Weekly Chart-

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands with upper band suggesting overbought status while lower band oversold status, and yellow lines are Fibonacci retracement lines which measures price rebound and backtrack.

2. Cooks Global Foods Limited (NZX: CGF) (Recommendation: Speculative Buy, Potential Upside: Lower Double-Digit) (M-cap: ~NZ$30.50 million)

Business Description: Cooks Global Foods Limited owns the intellectual property and master franchising rights to Esquires Coffee Houses worldwide (excluding New Zealand and Australia). CGF currently operates or franchises Esquires Coffee outlets in the United Kingdom, Ireland, Portugal, Bahrain, Kuwait, Syria, Saudi Arabia, Jordan, Pakistan, Indonesia, Canada, and China.

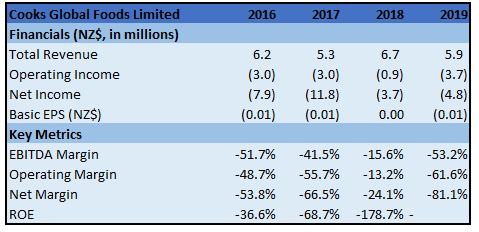

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The company has been closely monitoring the impact of the COVID-19 outbreak, particularly on its Esquires café operations in Ireland and the United Kingdom- the company’s two largest business units in revenue terms. CGF has applied for all government subsidies and relief it is eligible for. However, largely thanks to Government support packages, CGF is not aware of any of its franchisee’s needing to close their stores permanently. In China, CGF holds a minority interest in a joint venture operating 8 stores and 60 self-service machines. These have all re-opened or otherwise resumed operations.

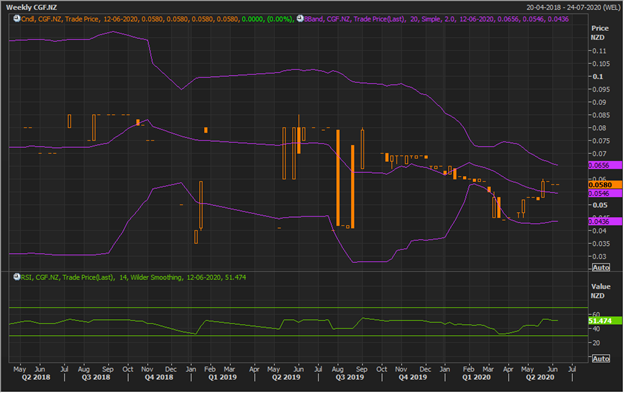

Technical Overview: Two weeks ago, the stock surged to $0.060 and gave close around the same. In the past three weeks including the on-going week, the stock has shown no movements giving flattish close. Momentum indicator RSI with 51 reading but with flattish curve at the end suggests flattish to bullish momentum for the stock.

Going forward, the stock might find resistance around upper Bollinger band level of $0.0656 while support could be around 20 period SMA of $0.0546.

Weekly Chart-

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands with upper band suggesting overbought status while lower line suggesting oversold status.

3. Moa Group Limited (NZX: MOA) (Recommendation: Speculative Buy, Potential Upside: Lower Double-Digit) (M-cap: ~NZ$26.16 million)

Business Description: Moa Group Limited is a brewing and hospitality company which is based in New Zealand. The Group is made of two segments: Moa Beverages, which brews and distributes Moa branded craft beers and ciders, and Moa Hospitality, which owns and operates restaurants and bars across New Zealand.

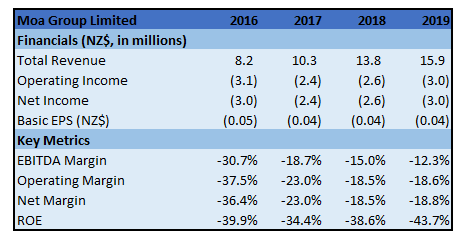

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: As per the release dated March 3, 2020, the company’s expected FY 2020 revenue is expected to be in excess of $40 million. The Venues have delivered a solid performance with their EBITDA for the year expected to be between $4.5 million to $5 million excluding head office and administration costs. The company’s recently acquired Non Solo Pizza (NSP) performed in line with expectations and successfully builds on the company’s strategy to expand its hospitality presence through a larger portfolio of venues across New Zealand and will continue to innovate and bring new concepts to market.

Valuation: The Moa Beverages segment has improved its position over last year and will deliver an EBITDA loss of approximately $1.2 million for FY20. On the TTM basis, EV/Sales multiple of MOA’s stock stood at 1.6x which is lower as compared to the industry average (Beverages) of 17.7x and its P/BV multiple is 2.0x while that of the industry is 15.5x. Thus, it can be said that the stock is currently undervalued and is offering decent opportunities for accumulation.

Technical Analysis: After several weeks of choppy price movements, the stock has moved up during the on-going week and has given close at its peak price of $0.18 around clustered resistance provided by 50% retracement level and 20 period SMA around $0.19. Momentum indicator RSI with 42 reading and curve at the end pointing up suggests gaining of bullish momentum. Going forward, the stock may have resistance around $0.22 as provided by 61.8% retracement level while support could be around $0.17 as provided by 38.2% retracement level.

Weekly Chart-

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands with upper band suggesting overbought status while lower band oversold status and yellow lines are Fibonacci retracement lines which measures price rebound and backtrack.

4. Burger Fuel Group Limited (NZX: BFG) (Recommendation: Speculative Buy, Potential Upside: Higher Single Digit) (M-cap: ~NZ$23.34 million)

Business Description: Burger Fuel Group Limited (NZX: BFG) has experience in the restaurant sector which stretches over 20 years, going back to the original BurgerFuel store which opened in 1995. It operates 3 brands: Shake Out, BurgerFuel and Winner Winner.

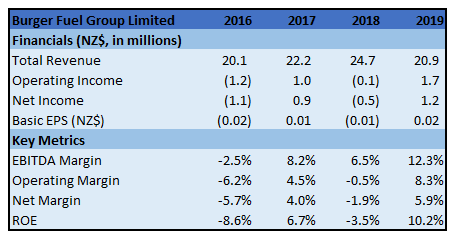

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: Due to the government’s announcement of both stage 3 and 4 COVID-19 measures being rapidly implemented, the company expects its earnings to be materially affected in the coming months. However, the company has no debt and, as at 30 September 2019, had cash reserves of $5.2 million which could help it in making deployments towards strategic growth initiatives.

Valuation: The company’s Master Licensee in Iraq has closed its last remaining BurgerFuel store in Baghdad. However, there will be no significant effect on its earnings due to the single store closure in Iraq. On the TTM basis, the stock’s EV/Sales multiple stood at 2.3x which is lower than the industry average (hotels and entertainment services) of 3.9x, and its P/BV multiple stood at 2.1x while that of the industry is 2.6x. Therefore, it can be said that the stock is slightly undervalued at the current juncture.

Technical Analysis: Creating a gap on chart around $0.38, the stock moved up to the high of $0.61 but it could not hold on positive momentum and slipped to 50% retracement level of $0.42 and for past three weeks including the on-going week, it has been trading around the same. Momentum indicator RSI with around 47 reading suggests neutral to bullish momentum for the stock.

Going forward, the stock might have good resistance around $0.4734 as provided by 38.2% retracement level while support could be around $0.38 where gap on chart exists.

Weekly Chart-

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands with upper band suggesting overbought status while lower band oversold status and yellow lines are Fibonacci retracement lines which measures price rebound and backtrack.

Comparative Price Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...