Summary:

New Zealand has a vibrant tech-based healthcare sector with 140 medical device companies and health IT companies, an active research community and entrepreneurial clinicians and health providers. There is an ecosystem of incubators, accelerators, and investors with growing expertise in partnering health technology companies making this an exciting space for economic opportunities. New Zealand companies have been developing health technologies for the local market for many decades.

The high technology export sector has been highlighted as the great economic hope for the New Zealand economy in various ways for many years.

As per the release dated 13th May 2020 by Medical Technology Association of New Zealand, The New Zealand HealthTech sector has shown steady growth over the past five years, with exports driving success. HealthTech companies generated $1.9 billion in revenue, with a five-year CAGR of 9.1% and global exports of healthcare technology accounted for $1.6 billion, or 87.5% of revenue.

Despite the high barrier to entry for medical devices, there is a strong perceived economic opportunity for the companies that can successfully achieve market entry. New Zealand has few companies, however, that have reached the scale required to operate as true multinational corporations, with the majority of companies having a turnover of between $1,000,000 and $30,000,000.

New Zealand’s Performance in Health Technology Innovation

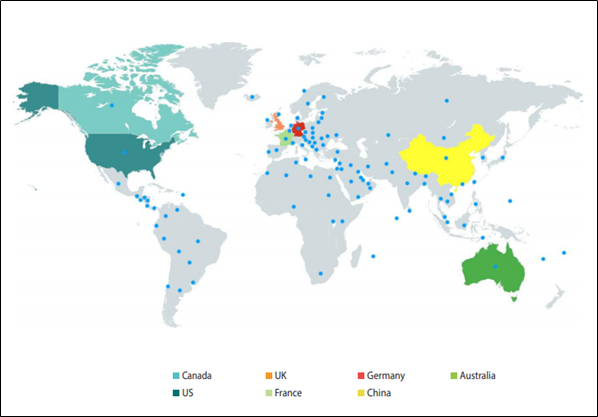

According to a report by Medical Technology Association of New Zealand (New Zealand Health Technology Review: 2016), New Zealand companies sell medical technologies to 116 countries, with Fisher & Paykel Healthcare exporting to 114 countries. The top markets for exporting NZ companies are:

Top Markets (Source: Medical Technology Association of New Zealand)

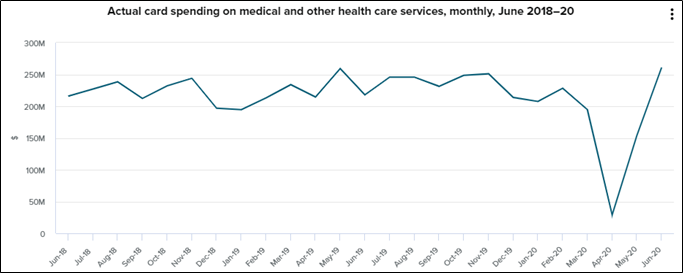

Health Care Spending Revived in June

As per Stats NZ, monthly card spending on medical and other health care services reached a record high in June 2020.

Key Data (Source: Stats NZ)

Significant Investment in Healthcare Budget

To ensure the sector is able to respond to the pandemic while maintaining the sustainable delivery of existing services, Budget 2020 invests significantly in areas that will make a difference to the well-being of New Zealanders. Key initiatives in this area include:

A Surge in Demand for Smart Care: A Look at Demand Drivers

With the outbreak of COVID-19, there has been a surge in demand for smart care, centered around patients and technologies.

However, already financially stressed sector, spending is expected to be driven by ageing and growing population, market expansion, clinical and technology advancements, etc. The health care providers should deploy innovative care delivery models based on data and analytics. They should ensure quality care and patient safety, digital health care technology solutions addressing better diagnostics, and more personalized tools. They should consider strategic investment in people, processes, and premises enabled by digital technologies.

Going ahead, healthcare companies with innovative approaches, having technologies to address health concerns cost-effectively, will benefit in an environment of smart healthcare facilities. There are companies listed on NZX which have been focused on providing cost-effective and technology-driven healthcare facilities and are expected to benefit from their innovative and cost-effective medical devices.

With the increase in competition, businesses are looking to explore the latest dynamics and trends, which will have a positive impact. They are embracing strategies where talent can collaborate with technology to improve operating efficiency to deliver smart healthcare centered around patients and technology. New Zealand also offers vast opportunities in R&D as well as medical tourism.

Key Challenges Faced by the Healthcare Industry

New Zealand’s health workforce faces several challenges. Notably, 40% of doctors and 45% of nurses are aged over 50 years. It also has a large unregulated workforce (numbering about 63,000), including care and support workers, who often have limited access to training. NZ needs to continually invest in training so that its health workforce has the skills needed to meet the health needs and expectations of caring for New Zealanders.

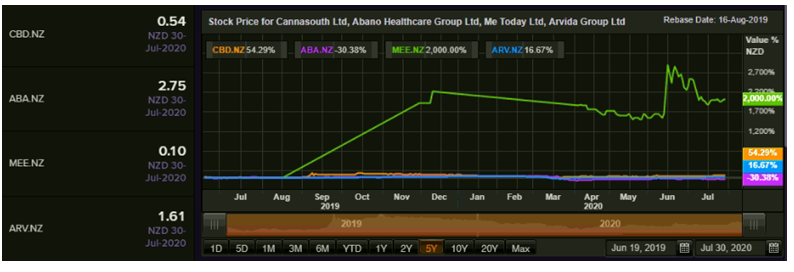

Since we now have a broad idea of the healthcare sector in New Zealand, it is important to look at the performance of some companies in the same sector (CBD, ABA, MEE, ARV).

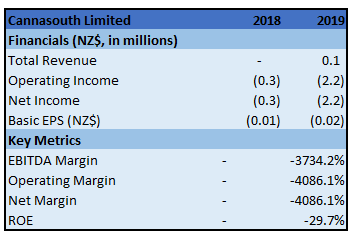

1. Cannasouth Limited (NZX: CBD) (Recommendation: Speculative Buy, Potential Upside: Lower Double-Digit), (M-Cap: ~NZ$65.51 million)

Business Description: Cannasouth Limited was formed to focus on the growth of the medicinally useful characteristics of cannabinoid compounds like THC, CBD, and other related chemical structures.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The company is focused on developing good clinical data to support medicinal cannabis products and establish education programmes for doctors and prescribers. Equipping these professionals with this knowledge will be key to ensuring they have readily available quality information to make informed decisions. The company’s mission is to create the foundations of a well-defined and vertically integrated medicinal cannabis business with a focus on sustainability and profitability.

Key Risks: The company is exposed to several risks, including market risk, credit risk and liquidity risk. Its activities expose it primarily to the risk of changes in interest rates. The company is exposed to interest rate risk because it invests funds in term deposits with banks.

Technical Overview:

Weekly Chart –

.png)

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands with upper band suggesting overbought status while lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack.

The stock has formed Parabolic Curve step-like formation which suggests that from the end point of Base 3 which might be around the current level, the stock could double in.

Technical indicator RSI with 59 reading suggests strong bullish momentum for the stock.

Going forward, the stock may have immediate resistance around 61.8% retracement level of $0.65 while support could be around intersecting value of 20 periods SMA and 23.6% retracement level of $0.46.

Thus, we give a “Speculative Buy” recommendation at the current price of NZ$0.540 per share on July 30, 2020.

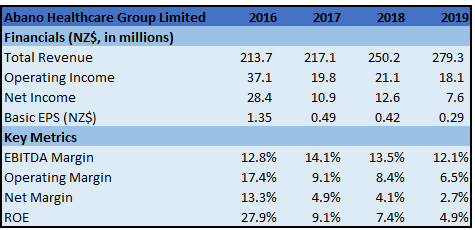

2. Abano Healthcare Group Limited (NZX: ABA) (Recommendation: Speculative Buy, Potential Upside: Lower Double-Digit), (M-Cap: ~NZ$72.27 million, Gross Dividend Yield: 3.934%)

Business Description: Abano Healthcare Group is an NZX listed company that operates and owns one of the largest dental networks in Australasia, which comprises of Maven Dental Group in Australia and Lumino The Dentists in New Zealand.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: After opening operations in the month of May, ABA’s dental networks have continued to recover strongly and have been performing ahead of expectations.

For June 2020, Lumino’s same store revenue was about 113 per cent of the same period last year, with Maven at about 98 per cent. Forward bookings for both Maven and Lumino, for the next 2 months, are ahead of where they were at the same point 12 months ago.

Valuation: The company’s focus remains on optimising the use of spare capacity within Abano’s dental practices, leveraging the trust and awareness of brands with targeted marketing and offers to attract patients into practices like the Lumino Dental Plan as well as leveraging investment made into technology in order to drive further efficiencies and better serve patients. We have applied P/E based relative valuation (on an illustrative basis) and the target price reflects a rise of lower double-digit (in % terms).

Key Risks: The performance of the business may be impacted by various factors, including the number of clinical days worked, revenue per clinical day, patient flow, and unplanned leave.

P/E Based Relative Valuation (Illustrative)

.png)

P/E Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Thus, we give a “Speculative Buy” recommendation at the current price of NZ$2.750 per share, up by 0.36% on July 30, 2020.

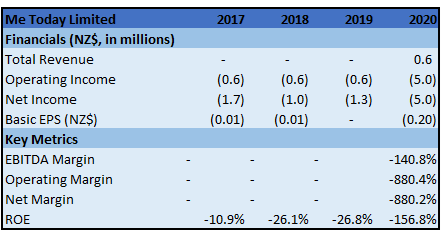

3. Me Today Limited (NZX: MEE) (Recommendation: Speculative Buy, Potential Upside: Lower Double-Digit), (M-Cap: ~NZ$42.73 million)

Business Description: Me Today Limited produces quality supplements that are made from premium quality formulas based on scientific and traditional evidence, as well as skincare that is cruelty free vegan/vegetarian and highly natural.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: Given the backdrop of coronavirus pandemic, NZ will remain the focus for Me Today for the financial year ahead. The brand has a great opportunity for growth in the New Zealand market, and the group wants to cement a position of strength in the local market before fully embarking on international expansion plans. Accessing the Chinese market remains the top priority as this can be accessed through the local NZ community of daigou traders. The company has recently released a new hand sanitiser which forms part of the Protect Skincare range and will launch 9 new supplement products during the July – September period taking the Me Today portfolio of products from 20 to 30 products in the first half of FY21.

Key Risk: The company’s interest rate risk arises from interest on cash and cash equivalents. Cash balances denominated in New Zealand dollars at variable rates expose the Group to cash flow interest rate risk. During the current and comparative year, the company’s interest rate risk was minimal.

Technical Overview:

Weekly Chart –

.png)

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands with upper band suggesting overbought status while lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack.

After the previous week of full-body bullish candle close, the stock has formed Hammer pattern with close on the peak price for the on-going week which exhibits strength in recently assumed uptrend. Technical indicator RSI with around 56 reading suggests strong bullish momentum for the stock.

Going forward, the stock may have resistance around 50% retracement level of $0.13 while support could be around $0.09.

Thus, we give a “Speculative Buy” recommendation at the current price of NZ$0.105 per share, up by 0.96% on July 30, 2020.

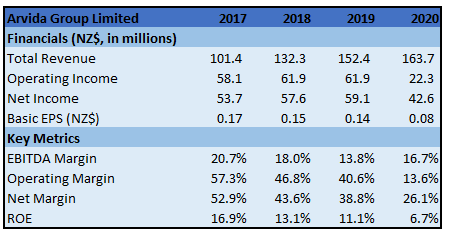

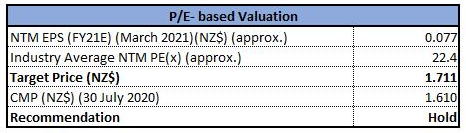

4. Arvida Group Limited (NZX: ARV) (Recommendation: Hold, Potential Upside: Higher Single-Digit), (M-Cap: ~NZ$873.40 million, Gross Dividend Yield: 3.813%)

Business Description: Arvida Group Limited is one of New Zealand’s largest aged care providers owning and operating 32 retirement villages located nationally.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: As an essential business, the company continued to operate throughout the Covid-19 pandemic. The effects of the containment measures required and the disruption to sales and construction activities can have a negative impact on the FY21 operational costs, sales volumes, sales margins, and earnings. However, the company is in a strong financial position and is positioned well for the opportunities and challenges that lie ahead.

Key Risks: The company’s activities expose it to a variety of financial risks: market risk (including interest rate risk), credit risk, liquidity risk and capital risk.

Valuation: The company reported that, while sales activity ceased during Alert Level 4 restrictions, sales results since resumption of activity in the month of May 2020 have been encouraging. Provisional sales metrics over the Q1 of the 2021 financial year resulted in an increase in gains on sales of occupation rights, as compared to prior corresponding period, on the lower level of settlements.

On an overall basis, $5.0 million of gains were witnessed on 44 settlements in 1Q FY 2021 as compared to $4.8 million on 61 settlements in 1Q FY 2020.

We have applied P/E based relative valuation (on an illustrative basis) and the target price reflects a rise of higher single-digit (in % terms).

P/E Based Relative Valuation (Illustrative)

P/E Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Thus, we give a “Hold” recommendation at the current price of NZ$1.610 per share, up by 0.63% on July 30, 2020.

Comparative Price Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...