I. Sector Landscape and Outlook

Vote Health is the prime source of funding for New Zealand’s health and disability system, followed by ACC for public financing in New Zealand. The budget allocated by Vote Health has been directly used for the day-to-day operation of solid and equitable public health and disability services provided by the skilled workforce in the communities, hospitals, and other care settings. The Ministry of Health has an important responsibility to oversee positive change in the health and disability system.

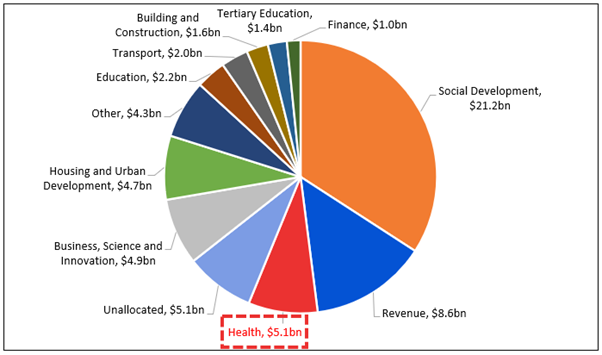

As per the ‘Wellbeing Budget 2021, released by Treasury.govt.nz, the government has allotted $4.7 billion in the healthcare sector, which includes more funding for PHARMAC and the transition to a new health system and development of a Māori Health Authority. In addition, the ‘Health and Disability System Reform’ has been allocated $485 million to support its operations and $1 million for capital expenditure.

Exhibit 1: COVID-19 Response and Recovery Fund – Wellbeing Budget 2021

Data Source: This work is based on/includes treasury.govt.nz data which are licensed by Treasury on behalf of the Crown for reuse under the Creative Commons Attribution 4.0 International Licence. Chart Created by Kalkine Group

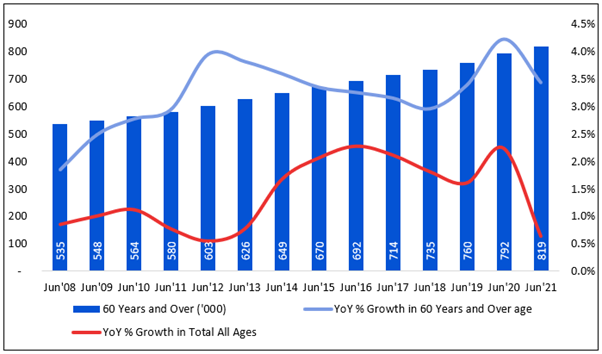

Higher Pace of Growth in Aged Population

As per Stats.govt.nz, NZ’s estimated resident population was provisionally reported at 5.12 million, comprising 2.54 million males and 2.58 million females. The median age of males and females stood at 36.7 and 38.7 years, respectively, as of 30 June 2021. Further, New Zealand’s population increased by 32.4k or 0.6% YoY by the end of 30 June 2021, while the estimated natural increase (births minus deaths) stood at 27.7k and counted net migration stood at 4.7k.

Further, the aged population, 65 years and over, increased by 3.4% YoY in June 2021, while the total all-ages population increased 0.6% YoY in June 2021. This significant rise in the aged population raises the requirement for healthcare facilities and support from government and private sources. Also, it is increasing the need for a retirement village with modern amenities at affordable prices.

Exhibit 2: Higher rate of Increase in Aging Population

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence. Chart Analysis by Kalkine Group

Government Plans to Re-Open Borders

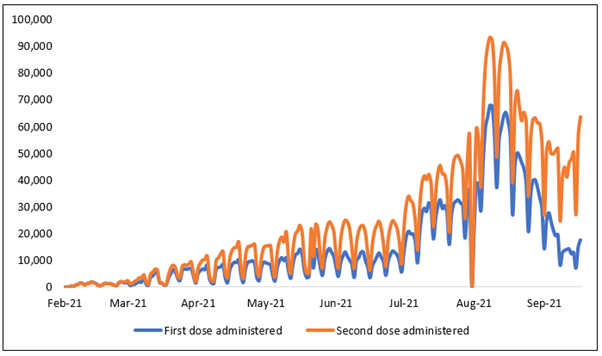

As per the Ministry of Health, as of 5 October 2021, 50% of the population (those aged +12) are fully vaccinated, comprising 2,105,686 people, ~80% of the people have had their first dose, comprising 3,361,425 people, and ~ 82% are booked in, or vaccinated with at least one dose, containing 3,438,288 people.

Moreover, the Government plans to use H2FY21 to vaccinate most New Zealanders and strategically conduct a self-isolation trial for vaccinated New Zealanders to augment phased wise quarantine-free travel. Moving ahead, the Government plans to re-opening the borders and move to an individualised risk-based model for a quarantine-free trip to strengthen the economy with a cautious approach. Broadly, the Government is planning to introduce Low-Risk, Medium-Risk, and High-Risk travel pathways. The pathway selected by the travel will depend on the risk associated with where they are coming from and their vaccination status.

Exhibit 3: Trend in First and Second Dose of Vaccinations Administered – (From 19 Feb 2021 to 5 Oct 2021)

Data Source: health.govt.nz, Copyright in content on this website is owned by either the Ministry of Health on behalf of the Crown or its licensors. It is licensed for re-use under a Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

Government Focus on Ambulance Services for All

As per the Ministry of Health, the government of New Zealand has allocated $17.264 million from Vote Health Budget in the coming four years to focus on the price and volume disparity in emergency air ambulance (rotary) services. The fund is aimed to ensure services remain equitable across regions in New Zealand and contracted performance levels are covered. This fund will likely support the existing air ambulance (rotary) services by meeting rising operational costs and volume growth.

It was understood from past experiences that emergency Road Ambulance Services respond to over half a million incidents every year and are a crucial momentum of the New Zealand health system. Therefore, in Budget 2021, $83.032 million spread over four years (including $31.428 million from Vote Labour Market) has been allocated to support and maintain emergency road ambulance facilities.

Aged Care Grabbed $8.11 Million, Used Over the Next Four Year

The Ministry of Health has assigned $8.11 million over the next four years to build an Aged Care Commissioner role and strengthen its ongoing operation. The Aged Care Commissioner role, which will be operational under the Health and Disability Commissioner, focuses on older people and their whānau higher confidence in the quality and safety of aged care and the scrutiny of their complaints.

Index Performance:

The S&P/NZX All Health Care Index generated a 2-year return of ~65.18% versus ~19.40% by the S&P/NZX 50 Index. Therefore, S&P/NZX All Health Care Index overperformed S&P/NZX 50 Index by ~45.78% in 2-year.

Exhibit 4: S&P/NZX All Health Care Index vs S&P/NZX 50 Index

Source: REFINITIV

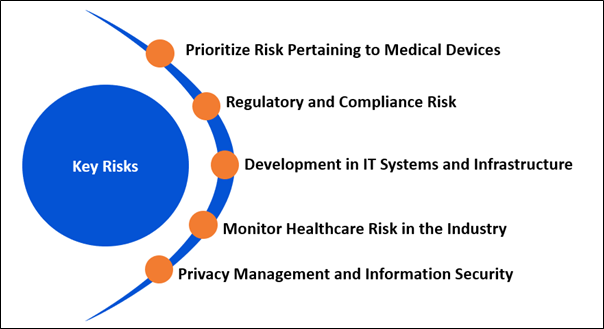

Key Risks and Challenges:

As per the Ministry of Health, older people are more exposed to a disability and suffer from more than one health condition. Therefore, the government wants a health system in New Zealand that supports people to live longer and healthier. Managing the long-term conditions of the aged population is a particular challenge, for example, dementia. The government forecasts the number of New Zealanders with dementia to increase from about 48,000 in 2011 to about 78,000 in 2026.

Further, obesity impacts the health of New Zealanders and has long-term health and social impacts. Children alone account for 10% of total obesity, while 30% in Pacific children. The cost of providing health services to New Zealanders via the existing model is unsustainable in the long term. The Treasury forecasts that, if nothing were to change in the current service, government health spending would increase from about 7% of GDP to about 11% of GDP in 2060.

Exhibit 5. Key Risks in Healthcare Sector:

Sources: Analysis by Kalkine Group

Outlook:

As per the Ministry of Health, the healthcare industry has strong support from public funding and a universal health system with an advanced and highly trained workforce.

As per the Budget 2021: Vote Health, the government has allocated $2.7 billion for District Health Boards (DHBs) to be spent over the next 4-year, up 4.37% from the existing baseline. This funding will facilitate DHBs to continue providing health services for New Zealand’s increasing and aging population in the face of inflation. In addition, Budget 2021 offers $700 million in capital funding to support the delivery of new DHB infrastructure projects and other projects.

Apart from the sector-specific factors, we have also analysed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

1) Fisher & Paykel Healthcare Corporation Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$17.53 billion, Gross Dividend Yield: 1.745%)

Business Description:

Fisher & Paykel Healthcare Corporation Limited (NZX: FPH) is a leading designer, manufacturer, and marketer of products and systems for acute and chronic respiratory care, surgery, and the treatment of obstructive sleep apnea.

Outlook:

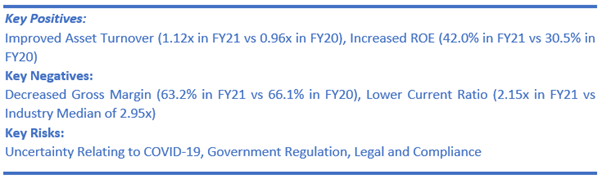

Amid ongoing uncertainties of vaccinations, lockdowns, COVID-19 variants, localized waves and return to stable hospitalization rates around the world, the company is not releasing guidance for FY22. Further, it expects Hospital and Homecare revenue for FY22 to be interrupted by the pandemic circumstances. Meanwhile, it will continue with its manufacturing plan and hold higher levels of inventory so that any surge demand can be met. Importantly, Hospital revenue continues to remain variable with higher volumes of Hospital hardware with an ongoing shift towards Optiflow of nasal high flow therapy. OSA shows signs of recovery after a slower Q4FY21.

As per the release dated 6 October 2021, the company launched F&P Evora Full, a compact full-face mask aimed at obstructive sleep apnea (OSA). The mask is developed with floating seal and stability wings to create the next generation of Dynamic Support Technology.

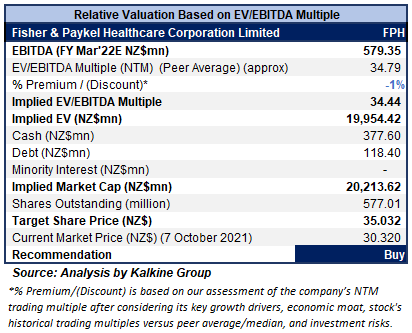

Valuation Methodology: EV/EBITDA Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock is valued using an EV/EBITDA multiple based relative valuation (on an illustrative basis) and the target price so arrived reflects a rise of low double-digit (in % terms). A slight discount has been applied to EV/EBITDA multiple (NTM) (Peer Average) considering a lower quick ratio at 1.52x in FY21 versus an industry median of 2.45x and the associated business risks.

For relative valuation, we have taken peers like Ryman Healthcare Ltd. (RYM.NZ), Arvida Group Ltd. (ARV.NZ), and Clinuvel Pharmaceuticals Ltd. (CUV.AX).

Considering the aforesaid facts, we give a “Buy” recommendation on the stock at the current market price of $30.32 per share (New Zealand Time: 12:32 PM (GMT +12) as of 7th October 2021.

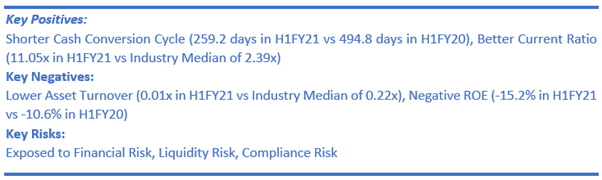

2) Cannasouth Limited (Recommendation: Speculative Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$53.66 million)

Business Description:

Cannasouth Limited (NZX: CBD) is a biopharmaceutical company and is engaged in medicinal cannabis product development and research.

Outlook

The company is vertically integrated to produce medicinal cannabis products in New Zealand from raw materials sourced locally. Also, it has a supply contract with an Australian partner to import three medicinal cannabis products. On 1 October 2021, the company stated that it has closed the capital raise of $4.7 million through the issue of 11,750,000 new fully paid ordinary shares and 3,917,149 options. Further, it plans to review the options for the proposed acquisition of the outstanding 50% of Cannasouth Cultivation Limited.

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

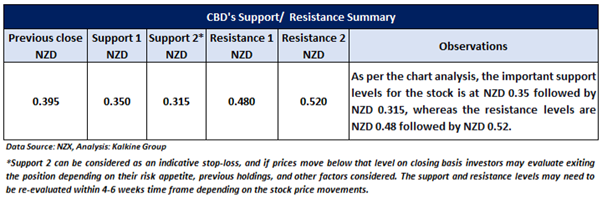

Considering the aforesaid facts, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.395 per share, down 1.25% as of 7th October 2021.

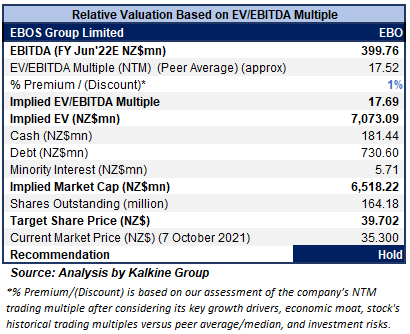

3) EBOS Group Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$5.80 billion, Gross Dividend Yield: 2.767%)

Business Description:

EBOS Group Limited (NZX: EBO) is the marketer, wholesaler, and distributor of healthcare, medical and pharmaceutical products. Further, the company is also a marketer and distributor of recognized consumer products and animal care brands.

Outlook:

The company reported decent earnings growth in FY21 and forecasts to be able to continue the growth momentum in FY22, primarily driven by the strong portfolio of businesses. It anticipates capital expenditure for FY22 to remain elevated due to the completion of the new pet care manufacturing facility, which attracts an additional expenditure of ~$30 million over and above business-as-usual CAPEX. Meanwhile, it has a strong balance sheet and cemented its position to pursue growth opportunities.

Valuation Methodology: EV/EBITDA Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock is valued using an EV/EBITDA multiple based relative valuation (on an illustrative basis) and the target price so arrived reflects a rise of low double-digit (in % terms). A slight premium has been applied to EV/EBITDA multiple (NTM) (Peer Average), considering a better asset turnover at 2.39x in FY21 versus an industry median of 0.44x and a higher ROE at 13.6% in FY21 versus an industry median of 11.5%.

For relative valuation, we have taken peers like Ryman Healthcare Ltd. (RYM.NZ), Summerset Group Holdings Ltd. (SUM.NZ), and Oceania Healthcare Ltd. (OCA.NZ).

Considering the aforesaid facts, we give a “Hold” recommendation on the stock at the current market price of $35.30 per share, up 0.57% as of 7th October 2021.

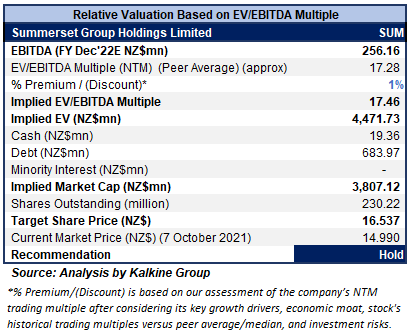

4) Summerset Group Holdings Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$3.45 billion, Gross Dividend Yield: 1.124%)

Business Description:

Summerset Group Holdings Limited (NZX: SUM) has grown to become one of the leading operators in the retirement village and aged care sector in New Zealand.

Outlook

As per the management, the company will see strong demand for retirement living in the coming days. The database for Whangārei village stands at 700-plus, where ~60% of villas are pre-sold. Further, the company expects FY21 New Zealand build rates in the range of 600-650 units (550-600 units sold under Occupation Right Agreement and 52 care beds). Also, it expects development margins to be in the range of 20%-25%.

Valuation Methodology: EV/EBITDA Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock is valued using an EV/EBITDA multiple based relative valuation (on an illustrative basis) and the target price so arrived reflects a rise of low double-digit (in % terms). A slight premium has been applied to EV/EBITDA multiple (NTM) (Peer Average), considering a higher ROE at 17.7% in HFY21 versus an industry median of 5.9% and a higher gross margin at 91.2% in H1FY21 versus an industry median of 48.7%.

For the purposes of relative valuation, we have taken peers such as AFT Pharmaceuticals Ltd. (AFT.NZ), Oceania Healthcare Ltd. (OCA.NZ), CogState Ltd. (CGS.AX), to name a few.

Considering the aforesaid facts, we give a “Hold” recommendation on the stock at the current market price of $14.99 per share, down 0.33% as of 7th October 2021.

Note 1: The reference data in this report has been partly sourced from REFINITIV.

Note 2: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the analysis has been achieved and subject to the factors discussed above alongside support levels provided.

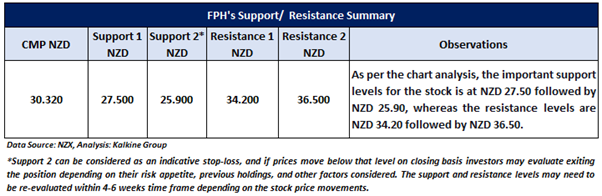

Technical Indicators Defined: -

Support: A level where-in the stock prices tend to find support if they are falling, and downtrend may take a pause backed by demand or buying interest.

Resistance: A level where-in the stock prices tend to find resistance when they are rising, and uptrend may take a pause due to profit booking or selling interest.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is authorised to provide general advice only. The information on this website does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...