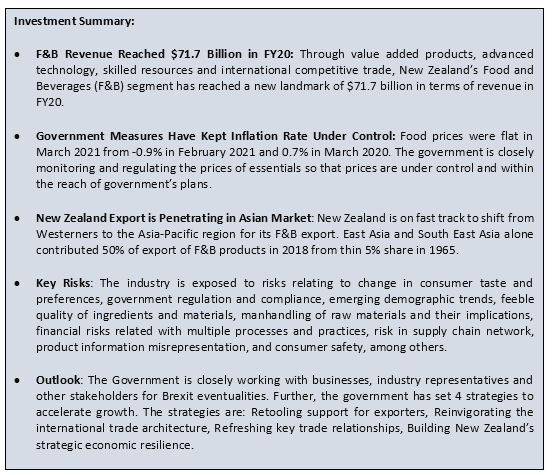

I. Sector Landscape and Outlook

Dairy, meat & wool, forestry, horticulture, seafood, arable, and processed foods & other products that includes live animals, honey, beverages, chocolate and soups are the part of primary Industry. As per the Economic Development Minister, the food and beverage industry has reached the total revenue landmark of $71.7 billion in FY20, mainly due to the increased focus of New Zealand companies on value-added products that is expected to continue and expand further in coming years.

As per Stats NZ, the food price index was flat in March 2021. Post seasonal modification, the index was down by 0.4% as against February 2021 index.

For the month of March 2021, fruit and vegetable prices grew by 0.3% (down 2.7% after seasonal modification), followed by meat, poultry, and fish prices that slipped by 0.6%, grocery food prices which fell by 0.4% (down 0.4% after seasonal modification). However, non-alcoholic beverage prices grew by 0.6%, followed by rise in restaurant meals and ready-to-eat food prices by 0.3%.

Exhibit 1: Food Price Index reported flat growth in March 2021

.png)

Data Source: stats.govt.nz, Chart Created by Kalkine Group

The government is focused towards wider economic plan, predicting an advanced product, sustainable and inclusive economy, and robust investment in the food and beverage value chain that will drive the outlook for the industry. The food and beverages industry has reported a drastic shift in export in East Asian countries in 2018, contributing ~38% of total export, from high concentration of export in European countries in 1965.

Exhibit 2: Shift in export destination to East Asia from high share in Europe in 1965

.png)

Data Source: mbie.govt.nz, Chart Created by Kalkine Group

Strengthening Export, Led by Dairy, Arable, and Processed Food

Amid COVID-19 circumstances, the production and exports of primary industry has reported better than expected numbers as per the Ministry of Primary Industries.

The export increased by 3.6% in FY20 to reach $48 billion driven by growth in dairy by 11.2% YoY to $20 billion, followed by rise in horticulture by 6.0% YoY to $6.5 billion, rise in Processed foods & other products by 5.2% YoY to $3 billion, among others.

Further, primary industries export revenue is estimated to fall by 1.0% YoY to $47.5 billion by June FY21E, led by fall in dairy by 4.6% YoY to $19.2 billion, followed by fall in meat & wool by 8.2% YoY to $9.8 billion.

However, processed foods & other products are expected to report a rise of 9.2% YoY to $3.2 billion, followed by rise in horticulture by 9.1% YoY to $7.1 billion, among others.

Exhibit 3: Trend in Primary Industries Export Revenue 2015-22:

.png)

Data Source: Ministry for Primary Industry, Chart Created by Kalkine Group

Strong Earning Visibility by all New Zealand Companies in Dairy

Amid turmoil led by COVID-19, the fundamental drivers of export growth for New Zealand’s dairy products continued to be strong, resulting better dairy prices over other agricultural commodity products. This resilience has been augmented by the swift recovery in demand from China. Further, the healthy underlying measures for demand of New Zealand’s dairy products still drives the government’s expectation of ongoing positive growth in dairy pay-outs (and, hence, profitability) over the coming years. However, the downside risks to future pay-outs is largely dependent on balanced nature of global markets, with the risk that increasing global output could surpass any retrieval in global demand.

Exhibit 4: Trend in Average Milk Solids Pay-Out, Including Dividend, By All Companies 2015-22

.png)

Data Source: Ministry for Primary Industry, Chart Created by Kalkine Group

Consolidation and Expansion in Small Businesses

The dairy cattle farming companies with 1-19 employees in New Zealand have grown from 51 in 2016 to 69 in 2020, that represents a CAGR of 7.8% over 2016-2020. However, there was a de-growth in Grocery, liquor and tobacco product wholesaling by CAGR of 2.4% over 2016-2020.

Exhibit 5: Number of businesses with 1-19 employees – 2016-20

.png)

Data Source: stats.govt.nz, Chart Created by Kalkine Group

Key Risks and Challenges:

As per the release by MPI on 18th March 2021, the regulatory agency has recalled Central Hawke's Bay producers Lindsay Farm raw unpasteurised drinking milk due to the identification of Campylobacter. This bacteria can result in severe gastrointestinal illness and could be serious in young people, the elderly, pregnant women and people with weakened immune systems. This indicates that the products of the companies in food and beverages industry are exposed to regulatory and compliance risk. In line with this, the industry faces the risk of food safety that leads to illness and foodborne diseases that are harmful to both the public and a company’s reputation. Food safety is dependent on product design, the procurement of products from the supply chain network, dangers in production processes, quality regulator, packaging and boxing, and other factors.

The Government has requested food industry to take preventive action that is resulting in obesity. The companies have been asked to look for sugar, fat and salt content in their products, that are resulting high growth in obesity in the consumers. Also, the companies should provide better information to consumers, and high restrictions on advertising to children. This indicates that the industry is closely regulated by the government for consumer safety and protection.

Exhibit 6: Key Risks in the Food and Beverages Industry:

Sources: Analysis by Kalkine Group

Outlook:

The development and growth in China is crucial for New Zealand’s short-term export prospects, as China accounts for one of the larger market place for export. The New Zealand has reported exports & re-export of overall goods in China to the tune of $5,247 million in Q4FY20 while the export and re-export in Asia Pacific Economic Co-operation (APEC) region stood at $12,411 million in the same period. This indicates that China alone accounted for 42% of overall export and re-export of all goods in the APEC region.

Importantly, the government has set trade recovery strategy that is based on four pillars of work – the four ‘R’s’ - to support New Zealand to overcome from the economic impacts of the pandemic. The four R’s are Retooling Support for exporters: Over 9,000 companies, with ~800 Māori businesses, have received COVID-19 support worth ~$30 million, by the regional business partner network. Reinvigorating the international trade architecture: The country has signed the Digital Economy Partnership Agreement with Singapore and Chile. Further, NZ plans to launch FTA negotiations with the UK, and EU with China soon. Refreshing key trade relationships: This circles around further trade diversification to support exporters with additional options, building brand and reputation, and giving new and strengthened FTAs. Resilience - Building New Zealand’s Strategic Economic Resilience: The government is striving to maintain a global trading system with fair opportunities for businesses to thrive.

Apart from the sector-specific factors, we have also analysed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

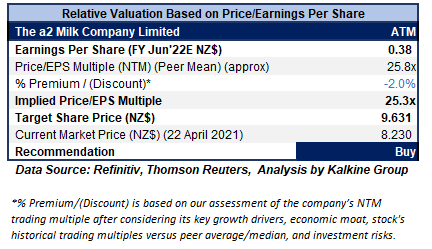

1) The a2 Milk Company Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$6.11 billion)

Business Description:

The a2 Milk Company Limited (NZX: ATM) is engaged in the sale of branded products from cows milk and the milk contains only the A2 protein type.

Outlook:

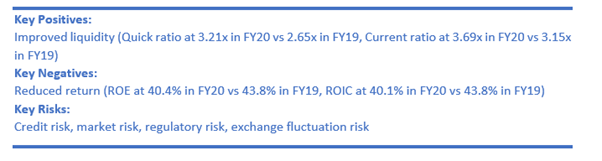

The Company remains assured in the strong fundamentals of the business, investments in brands and in its plans to drive long term growth. Further, the company expects a slide in EBITDA margin on the back of fall in revenue, higher brand investment, longer daigou/reseller support, fluctuation in foreign exchange and adverse channel mix. Revenue for FY21 is expected ~$1.4 billion, and EBITDA margin in the range of 24%-26% (excluding MVM acquisition costs).

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Stock Recommendation

We have applied P/E based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied a slight discount to P/E Multiple (NTM) (Peer Average) considering reduced revised guidance for FY21, risk pertaining to COVID-19 circumstances, and exposure of the company towards forex fluctuation.

For the purposes, we have taken peers such as Woolworths Group Ltd (WOW.AX), Bega Cheese Ltd (BGA.AX), to name a few.

Considering the aforesaid facts, we give a “Buy” recommendation on the stock at the current market price of $8.230 per share, down 0.96% on 22nd April 2021.

2) Foley Wines Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$115.696 million, Gross Dividend Yield: 2.367%)

Business Description:

Foley Wines Limited (NZX: FWL) produces and sells wine globally. It has collection of iconic wineries and brands from New Zealand’s most acclaimed wine regions.

Outlook

The company expects lower harvest in 2021 on the back of poor weather conditions during flowering in the two major regions as well as some frosts in spring. However, the Company has deep rooted its strong foundation for growth to take advantage of opportunities as they come and will extend its focus on brand building and developing new routes to market the products at the premium price points.

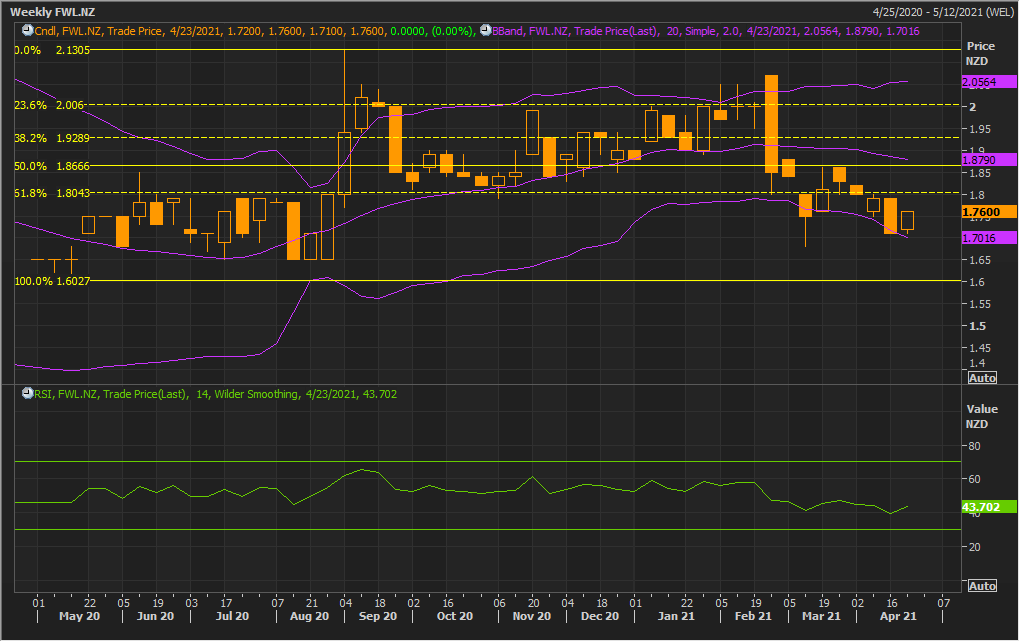

Technical Overview:

Weekly Chart

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack. https://www.bollingerbands.com/

After a sharp fall, the stock witnessed in the previous week, it has given a stronger close for the ongoing week with a ‘Bullish Harami’ chart pattern formed on the weekly chart which is towards confirmation of bullish reversal of the trend. The technical indicator RSI with a reading around 44 and a curve at the end pointing up, suggests gaining of bullish momentum.

Going forward, the stock may have resistance around 20 periods SMA of $1.88 whereas support could be around the lower Bollinger band of $1.70.

Stock Recommendation

Considering a firm revival in the global market, strong product line and fundamentals as well as strong balance sheet and decent outlook, we give a “Buy” recommendation on the stock at the current market price of $1.760 per share on 22nd April 2021.

3) Cooks Global Foods Limited (Recommendation: Speculative Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$22.602 million)

Business Description:

Cooks Global Foods Limited (NZX: CGF) owns the international intellectual property and master franchising rights to the Esquires Coffee brand (excluding Australia and New Zealand).

Outlook

Amid the impact of COVID-19, the business has reflected resilience in the post lockdown period, especially in UK & Ireland. During July-October 2020, outlets were permitted to open in near to normal mode and the same momentum is expected in the future period. The company has also restructured its plan for future growth that will be reflected in the FY21 financial performance.

Technical Overview:

Weekly Chart

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack. https://www.bollingerbands.com/

The stock has given a flattish close for the ongoing week. The technical indicator RSI with a reading around 35 and a flattish curve at the end, suggests flattening of momentum.

Going forward, may have resistance around the 23.6% retracement level of $0.041 whereas support could be around the lower Bollinger band of $0.034.

Stock Recommendation:

Considering the current trading levels, restructuring of business strategy for future period, wide presence of business across geographies and current business momentum, we give a “Speculative Buy” rating on the stock at the current market price of $0.036 per share on 22nd April 2021.

4) Comvita Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$232.337 million)

Business Description:

Founded in 1974, Comvita Limited (NZX: CVT) is the global market leader of the Mānuka honey and committed to the development of Mānuka and Bee products led by unrivalled scientific knowhow.

Outlook

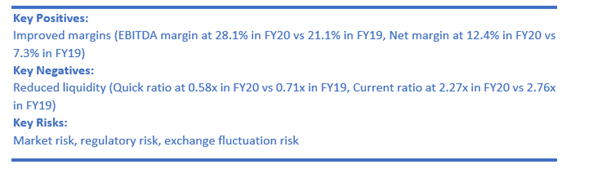

The management has upwardly revised the guidance for FY21. The operating EBITDA is expected to be in a range of $22.5-$25.5 million from earlier guidance of $20-$23 million. This optimism has been built on the back of robust growth in its focus growth markets of China and North America (nullifying Australia, New Zealand and Hong Kong limitation). The company is also realizing strong traction from digital channel that accounted for over 30% of group sales and extended efficiencies in production and cost control measures. Importantly, the new harvest model has been rolled out successfully in FY21 and strong cost control initiatives will deliver a small contribution to Group profits in FY21.

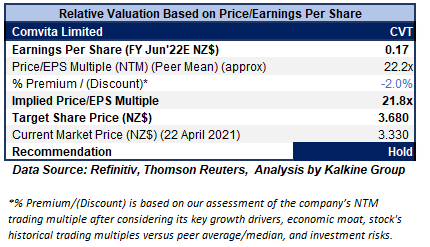

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Stock Recommendation

We have applied P/E based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied a slight discount to P/E Multiple (NTM) (Peer Mean) considering business risk in the wake of COVID-19 restrictions.

For this purpose, we have taken peers such as A2 Milk Company Ltd (ATM.NZ) and Scales Corporation Ltd (SCL.NZ), to name a few.

Considering resilient business model, strong product penetration across geographies, prudent capital management, and decent outlook, we give a “Hold” recommendation on the stock at the current market price of $3.330 per share, up by 0.91% on 22nd April 2021.

Comparative Price Chart (Source: Refinitiv (Thomson Reuters))

Note: Investment decision should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the Valuation has been achieved and subject to the factors discussed above.

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...