I. Sector Landscape and Outlook

As per the Ministry for Primary Industries (MPI), food and fibre sector export revenue will cross $50 billion for the first time, reaching a record $50.8 billion in FY22, up 6% YoY. The sector indicates promising growth in the future driven by strong demand for food and fibre products as consumers worldwide look to healthier food and natural fibres with sound environmental credentials. An increase in total export revenue is anticipated for most sectors like dairy, meat and wool, horticulture, seafood, forestry and arable.

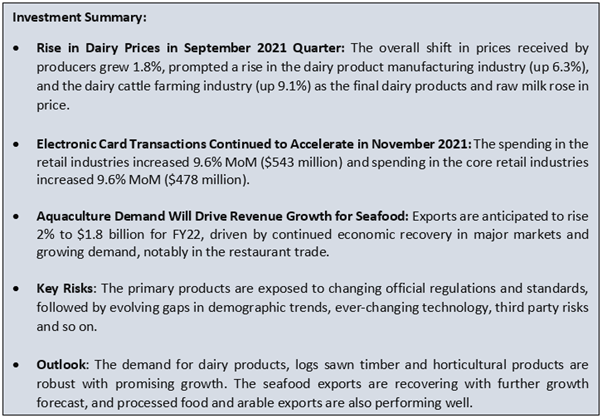

Dairy Prices Up in September 2021 Quarter

As per Stats.NZ, in the September 2021 quarter, prices received by producers grew 1.8%, and prices paid by producers grew 1.6%. The overall shift in prices received by producers was prompted by a rise in the dairy product manufacturing industry (up 6.3%) and the dairy cattle farming industry (up 9.1%) as final dairy products, and raw milk rose in price. The dairy product manufacturing industry influenced the producers' overall change in prices (up 7.4%) as raw-milk prices increased.

Exhibit 1: Dairy Product Manufacturing Price Indexes, September 2007–2021 Quarter

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

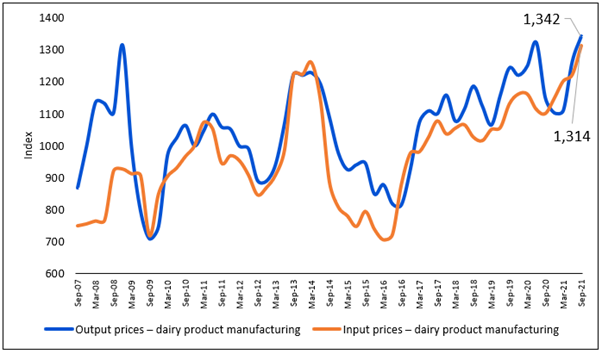

Electronic Card Transactions Continued to Accelerate in November 2021

As per Stats.NZ, the changes in the value of electronic card transactions for the November 2021 month versus October 2021 indicate that retail industries' spending increased 9.6% ($543 million) and spending in the core retail industries increased 9.6% ($478 million). In the consumables sub-industry space, supermarkets and grocery stores grew $144 million (7.7%), liquor increased by $7 million (3.6%). However, specialised food decreased by $4 million (1.7%).

Exhibit 2: Trend in Retail card spending ($Billion), monthly, November 2019 – November 2021

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

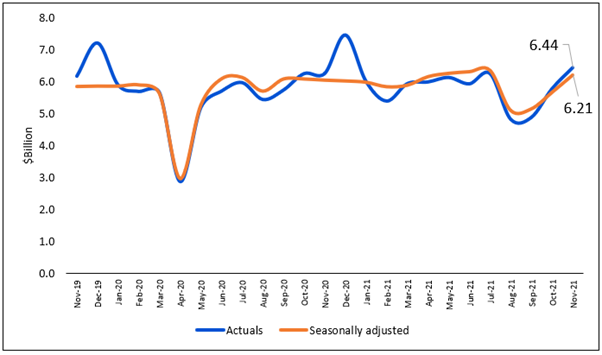

Aquaculture Demand Will Drive Revenue Growth for Seafood

As per MPI, there have been positive demand signals as food service reopen. However, prices and volumes have been volatile throughout 2020 and 2021 and are expected to persist in 2022, indicating a low growth forecast over 30 June 2022. Exports are anticipated to rise 2% to $1.8 billion for FY22, driven by continued economic recovery in major markets and growing demand, notably in the restaurant trade. MPI anticipates moderate export growth in FY23, with a further 2% rise in seafood export revenues.

Exhibit 3: Trend in Seafood Export Revenue 2017-2023 ($ million)

Data Source: This work is based on/includes the Ministry for Primary Industries data which are licensed under Crown for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

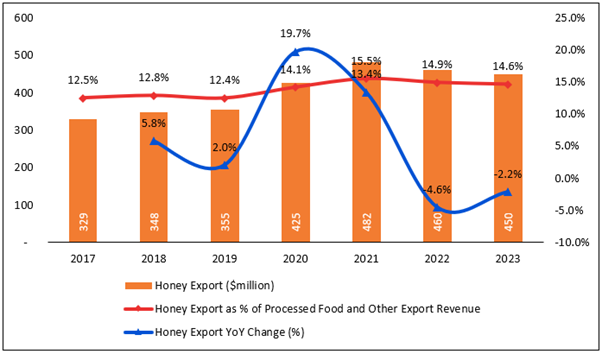

Export Demand to Drive Future Growth for Honey

As per MPI, honey exports reached a record 12,790 tonnes in FY21. However, the average price fell by 9% YoY to $37.66 per kg. While major exported honey was still packed ready for retail, many monofloral mānuka and non-mānuka honey were shipped in bulk and at lower prices than last year. Export prices for honey in retail packs held steady. Honey exports are anticipated to fall to $460 million for FY22. The demand for monofloral manuka is expected to remain firm.

Exhibit 4: Trend in Honey Export Revenue 2017-2023 ($ million)

Data Source: This work is based on/includes the Ministry for Primary Industries data which are licensed under Crown for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

Index Performance:

The S&P/NZX All Consumer Staples Index generated a 10-year return of ~310.2% versus ~175.0% by the S&P/NZX All Index. Therefore, S&P/NZX All Consumer Staples Index overperformed S&P/NZX All Index by ~135.2% in 10-year.

Exhibit 5: S&P/NZX All Consumer Staples Index vs S&P/NZX All Index

.png)

Source: REFINITIV, Chart Created by Kalkine

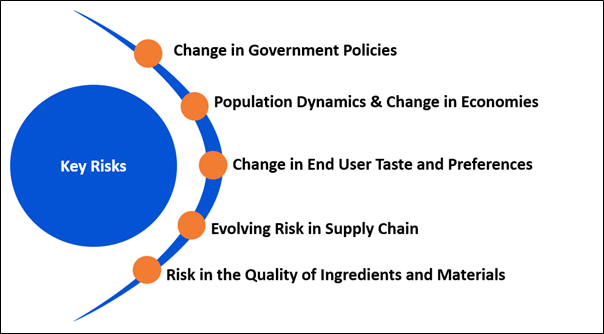

Key Risks and Challenges:

The changing international trends influence food security, poverty and complete sustainability of food and agricultural ecosystems. Further, climate change impacts disproportionately food-insecure regions, exposing crop and livestock production as well as fish stocks and fisheries. Also, the vital parts of food ecosystems are turning into more capital-intensive, vertically integrated and concentrated in fewer hands. Moreover, crises and natural disasters are growing in number and intensity.

The alcohol industry is competing to make its presence in online sales to reach a more extensive consumer base, like other booming online industries. While few alcohol brands have made their presence felt online, others have learned to create strategic partnerships.

Exhibit 6. Key Risks in Consumer Staples Sector:

Sources: Analysis by Kalkine Group

Outlook:

As per MPI, total export revenue for food and fibre will reach $50.8 billion in FY22, indicating a net rise of 6% YoY. Since mid-2018, the Government has committed ~$160 million towards Sustainable Food and Fibre Futures (SFF Futures) with Futures programmes of a total investment of nearly $355 million. MPI reached a significant milestone in October 2021, agreeing in principle for the New Zealand-United Kingdom Free Trade Agreement (NZ-UK FTA) that will eliminate customs tariffs on food and fibre exports to the UK. This will facilitate exporters to compete on a level playing field in the UK market.

The country realizes solid demand for NZ products, such as dairy products, logs sawn timber and horticultural produce. The seafood exports are recovering with further growth forecast, and processed food and arable exports are also performing well.

Apart from the sector-specific factors, we have also analysed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

1) The a2 Milk Company Limited (Recommendation: Buy, Potential Upside: Low Double-Digit (M-Cap: NZ$4.25 billion)

Business Description:

The a2 Milk Company Limited (NZX: ATM) is engaged in the sale of branded products in targeted markets made with milk from cows that produce milk naturally containing only the A2 protein type.

Outlook:

The company is confident in the fundamentals of its business and it has a strong outlook on the future. It also acknowledges the inevitable challenges related to COVID-19 and other rapidly changing market dynamics. The overall marketing investment in FY 2022 is expected to return to approximately FY 2020 levels which is anticipated to continue to drive improved brand health metrics as well as future demand.

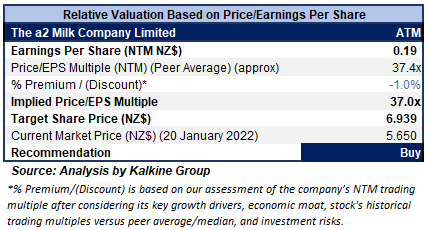

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using P/E multiple-based illustrative relative valuation, and the target price so arrived reflects a rise of low double-digit (in % terms). A slight discount has been assigned to P/E Multiple (NTM) (Peer Average), considering the risks related to the COVID-19 pandemic and supply chain disruption. However, the company is possessing decent outlook.

For relative valuation, peers like Seeka Ltd (SEK.NZ), Fonterra Shareholders' Fund (FSF.NZ), Scales Corporation Ltd (SCL.NZ), among others, have been considered.

Considering the facts above, we give a “Buy” recommendation on the stock at the current market price of $5.65 per share as of 20th January 2022 (New Zealand Time: 1:05 PM (GMT +12).

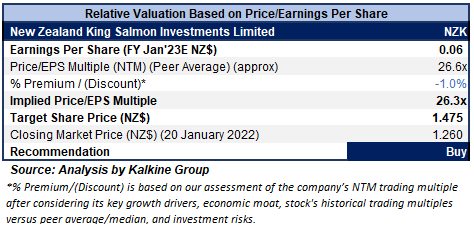

2) New Zealand King Salmon Investments Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$175.12 million)

Business Description:

New Zealand King Salmon Investments Limited (NZX: NZK) is one of the largest aquaculture producers of the premium King Salmon species. It operates under four key brands: Ōra King, Regal, Southern Ocean, and Omega Plus, as well as the New Zealand King Salmon label.

Outlook

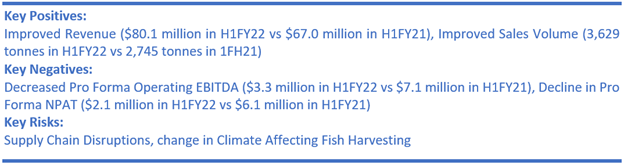

The company anticipates harvest volumes of over 4,000 tonnes in H2FY22, delivering at usual premium prices maintained despite COVID-19 circumstances. In addition, excess unbranded stock, primarily whole frozen fish, continues to be sold to global customers outside of traditional branded channels. Further, the company is extending its innovation program for Ōra King and launched a limited edition new Ōra King Keiji product, premium sashimi or plate-size salmon recognized for unique flavour and delicate texture.

On 8th December 2021, the company provided an update on FY22 earnings guidance where proforma EBITDA is expected to be in the range of $10.5-$12.5 million, up from the previous guidance of $8.0-$10.0 million.

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using a P/E multiple-based illustrative relative valuation, and the target price so arrived reflects a rise of low double-digit (in % terms). Accordingly, a slight discount has been applied to P/E Multiple (NTM) (Peer Average), as the small fish size and compensating restrictions on harvest have negatively disrupted the company's financial performance.

For relative valuation, we have taken peers like PGG Wrightson Ltd (PGW.NZ), The a2 Milk Company Ltd (ATM.NZ), and Scales Corporation Ltd (SCL.NZ).

Considering the facts above, we give a “Buy” recommendation on the stock at the closing market price of $1.26 per share as of 20th January 2022.

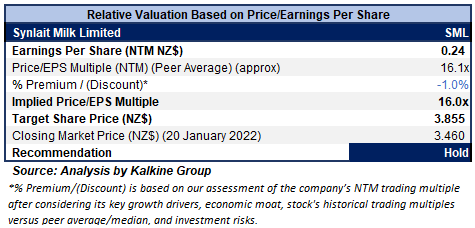

3) Synlait Milk Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$756.29 million)

Business Description:

Synlait Milk Limited (NZX: SML) is engaged in producing a range of nutritional milk products for its global customers by combining expert farming with state-of-the-art processing.

Outlook

The company estimates its forecast milk price at $8.00 per kgMS for the current 2021-2022 season driven by sustained robust demand for dairy. Further, it expects to achieve strong profitability in FY22 driven by the benefits of return to normal trading conditions and tighter management of its Ingredient business. Additionally, the advantage of enhanced infant base powder volumes, a rising contribution from its Liquids and Consumer Foods business units, and substantial cost savings from Synlait, Dairyworks and Talbot Forest Cheese would also drive profitability.

The company also stated that its FY22 would comprise a one-off gain on selling around $17 million from the sale and leaseback of the land and building at Synlait Auckland. Moreover, the company highlighted that its new Total Debt/EBITDA covenant limit stood at 4.5x for FY22, and it expects it to remain lower than 4.0x in FY22.

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using a P/E multiple-based illustrative relative valuation, and the target price so arrived reflects a rise of low double-digit (in % terms). Accordingly, a slight discount has been applied to P/E Multiple (NTM) (Peer Average), considering lower EBITDA margin in FY21 on the YoY basis. However, the company has increased its current ratio in FY21 on the YoY basis.

For relative valuation, we have taken peers like Sanford Ltd (SAN.NZ), Seeka Ltd (SEK.NZ), and Fonterra Shareholders' Fund (FSF.NZ).

Considering the facts above, we give a “Hold” recommendation on the stock at the closing market price of $3.46 per share, down 0.86% as of 20th January 2022.

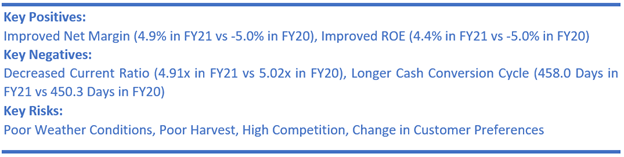

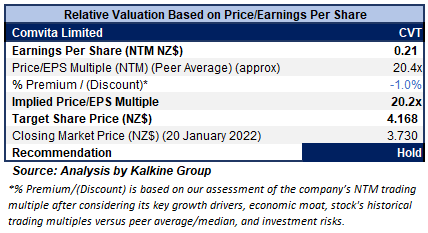

4) Comvita Limited (Recommendation: Hold, Potential Upside: Low Double-Digit (M-Cap: NZ$261.34 million, Gross Dividend Yield: 1.47%)

Business Description:

Comvita Ltd (NZX: CVT) is currently one of the leading players globally in producing Manuka honey. The company has a decent geographical presence across Australia, New Zealand, China, and North America.

Outlook:

The company’s mega plan of $25 million remains on track to deliver by 2025. The company has achieved over $12 million of improvements in the first 18 months, investing $1.2 million to deliver this in FY21. In addition to this, it will invest an additional $2.5 million in transformation projects in FY22. Meanwhile, it has announced a 60:15:20 plan to deliver a gross profit of over 60%, marketing to sales ratio of 15% and an EBITDA ratio of 20% by 2025.

On 15 December 2021, the company announced its intention to acquire upto 300,000 of its ordinary shares for proposed share scheme arrangements for employees.

On 16 November 2021, the company reported record China market sales during the 11:11 event that boosted confidence in the focused strategy and lifted the unique business model. The domestic market reported a high double-digit growth driven by the quality of market execution.

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using P/E multiple-based illustrative relative valuation, and the target price so arrived reflects a rise of low double-digit (in % terms). A slight discount has been assigned to P/E Multiple (NTM) (Peer Average), considering the decline in the current ratio to 4.91x in FY21 and a longer cash conversion cycle to 458.0 Days FY21.

For relative valuation, peers like Sanford Ltd (SAN.NZ), The a2 Milk Company Ltd (ATM.NZ), 'Synlait Milk Ltd (SML.NZ), among others, have been considered.

Considering the facts above, we give a “Hold” recommendation on the stock at the closing market price of $3.73 per share, down 1.32% as of 20th January 2022.

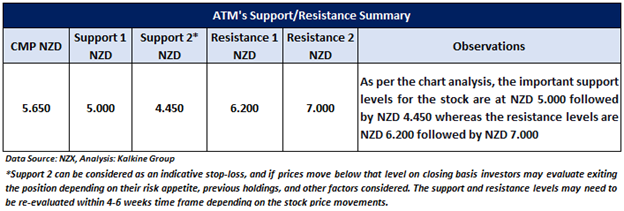

Note 2: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the analysis has been achieved and subject to the factors discussed above alongside support levels provided.

Technical Indicators Defined: -

Support: A level where-in the stock prices tend to find support if they are falling, and downtrend may take a pause backed by demand or buying interest.

Resistance: A level where-in the stock prices tend to find resistance when they are rising, and uptrend may take a pause due to profit booking or selling interest.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is authorised to provide general advice only. The information on this website does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...