1. Sector Landscape and Outlook

According to the Reserve Bank of New Zealand (RBNZ), global financial market volatility is elevated due to investors' anticipation of central bank measures to control inflationary pressure in the near term and a fading outlook for economic activity in the medium term. Further, the annual CPI inflation rate in NZ is at 7.3% in the June 2022 quarter, much higher than Reserve Bank and most private forecasters projected. However, the demand for NZ products has remained resilient to international and domestic headwinds.

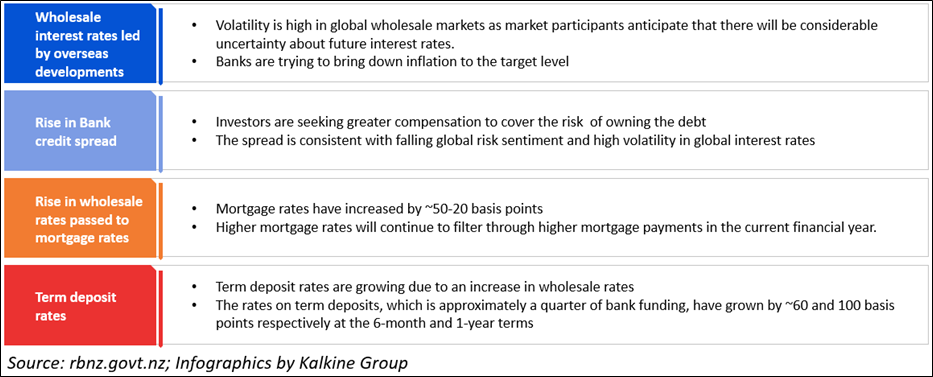

Exhibit 1: Performance of Mortgage and Term Deposit Rates

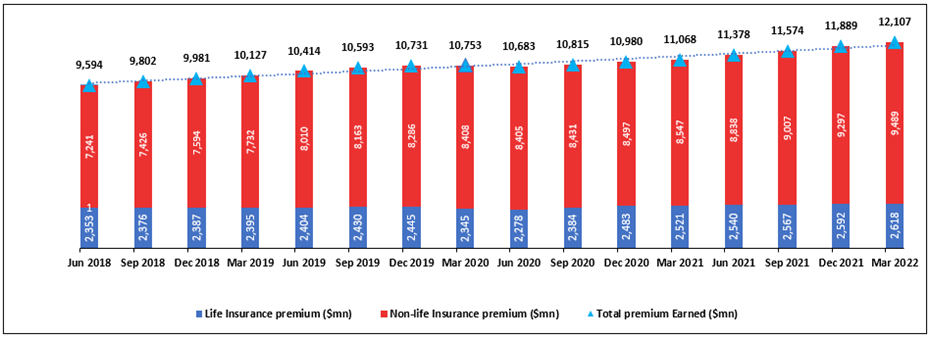

Insurance Sector Remained Resilient Despite Economic Uncertainty

As per RBNZ, the life insurance market in NZ is less concentrated than property and motor insurance or health insurance. It’s been observed that the life insurance sector is consolidating as most banks have divested or are divesting their life insurance wings. However, the insurance sector remained resilient during economic uncertainties. The solvency capital ratio of the general insurance sector fell in 2021 but is still at a decent level. The solvency ratio for the life insurance sector grew, and it remained volatile around previous levels for the health insurance sector. Further, the general insurers account for the most significant part of NZ’s insurance sector, with ~59% of total gross premium revenues, life insurers ~29%, and health insurers ~12%.

Exhibit 2: Trend in Insurance Companies in NZ ($million)

Data Source: This work is based on/includes rbnz data which are licensed by rbnz.govt.nz for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

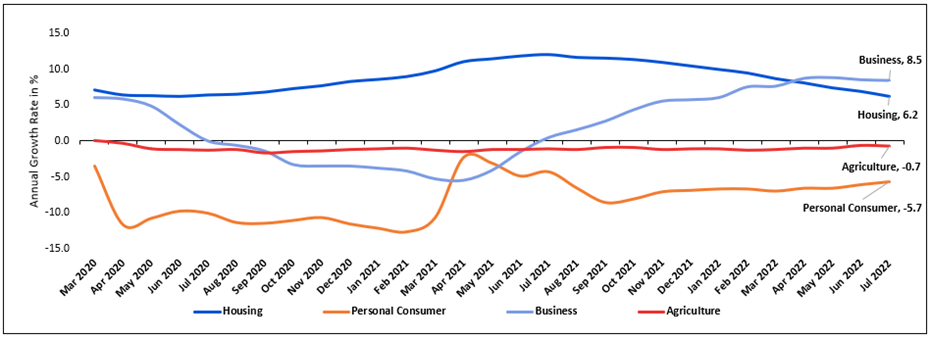

Marginal Uptick in House Lending

RBNZ's total housing lending stock grew by $848 million (0.2%) in July 2022, down on the $1.1 billion (0.3%) rise reported in June 2022. However, the annual growth decreased to 6.2%, sliding further from 6.9% in June 2022. Additionally, the total personal consumer lending stock fell by $38 million (-0.3%) in July 2022, while the annual growth increased to -5.7% from -6.1% in June 2022. Meanwhile, the total business lending stock grew by $221 million (0.2%) in July 2022, while its annual growth fell from 8.6% to 8.5%. Annual growth has decreased from its high in May 2022, the highest annual growth rate seen since February 2009. The total agriculture lending stock grew by $192 million (0.3%) in July 2022, while yearly growth decreased from -0.6% to -0.7%.

Exhibit 3: Lending Pattern Since March 2020 – Banks and NBLIs

Data Source: This work is based on/includes rbnz data which are licensed by rbnz.govt.nz for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

Aggregate Retail Spending is Driving the Demand

As per RBNZ, businesses are facing many headwinds. Despite this, the business remained resilient, primarily driven by aggregate retail spending. Although demand remains resilient, the output is under pressure due to an acute labour shortage across all sectors, global supply-chain disruptions, higher interest rates and elevated global uncertainty. Some larger businesses have continued with their planned investments, while some smaller companies are holding back on investment (beyond repairs and maintenance) due to global uncertainty, causing the slowdown in growth perspective.

Index Performance:

The S&P/NZX All Financials Index generated a 2-year return of ~32.44% versus ~-1.83% by the S&P/NZX 50 Index. Therefore, S&P/NZX All Financials Index overperformed S&P/NZX 50 Index by ~34.27% in 2-year.

Exhibit 4: S&P/NZX All Financials Index vs S&P/NZX 50 Index

Source: REFINITIV

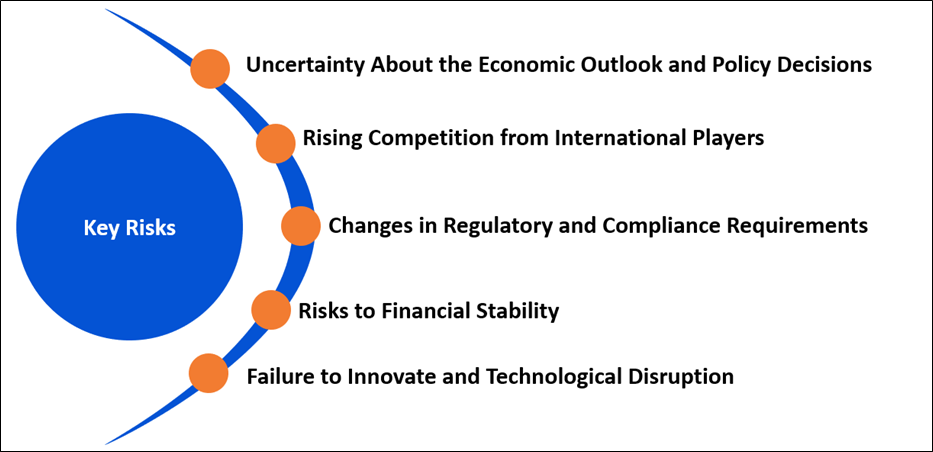

Key Risks and Challenges:

Financial market participants are adjusting to uncertainty about the economic outlook and the transmission of its policy decisions, causing high volatility in the financial system and a sense of nervousness in taking financial decisions. The Monetary Policy Committee of NZ increased the Official Cash Rate (OCR) to 3% from 2.5% to fight against elevated inflation. It plans to make similar decisions to maintain price stability and sustainable employment. It’s been observed that few households throughout NZ are finding current economic conditions challenging as the growing cost of living has beaten income growth.

Exhibit 5. Key Risks in Financial Sector:

Source: Analysis by Kalkine Group

Outlook:

The NZ financial system remains better placed to support the economy. Banks’ capital positions have grown in past ahead of upcoming higher capital requirements. This strengthens the banking sector’s ability to realize losses and continue lending in the event of a downturn. According to 'Fortnightly Economic Update', released by 'The Treasury', on 2 September 2022, the retail sales volumes decreased 2.3% in June 2022 quarter in NZ as 12 of the 17 industry groups fell in the previous quarter. Further, the US Federal Reserve Chairman Jay Powell's address at Jackson Hole indicated a further rise in interest rates to bring inflation down to 2%. The Bank of Korea increased its policy rate by 25 basis points, and Bank Indonesia increased by 25 basis points to tighten the cycle. Signs of undermining global demand are reflected in Asia's trade and production data. Japan's flash manufacturing new export orders PMI decreased 1.8 points to 47.0 in August 2022, followed by declines in export orders for Taiwan and Korea.

Apart from the sector-specific factors, an analysis on three NZX-listed companies is provided. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

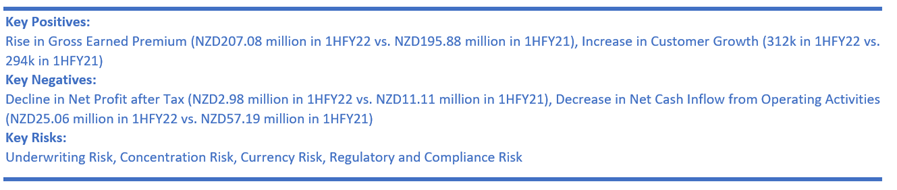

1) Tower Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZD231.48 million, Annual Dividend Yield (TTM)1: 8.80%)

Business Description:

Tower Limited (NZX: TWR) is a New Zealand-based insurance company that operates across New Zealand and the Pacific Islands.

Outlook:

The company remain focused on delivering healthy underlying operating performance, driving efficiencies through scalable platform and cost management and offering positive shareholder returns through dividends and boosting growth. Further, TWR has maintained its full year underlying NPAT guidance of between NZD21 million and NZD25 million.

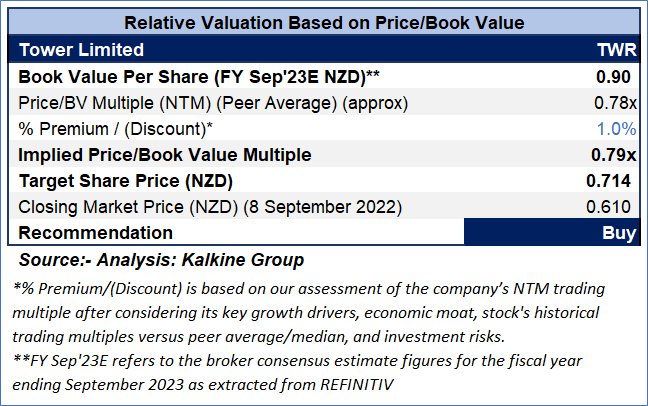

Valuation Methodology: Price/Book Value Based Relative Valuation (Illustrative)

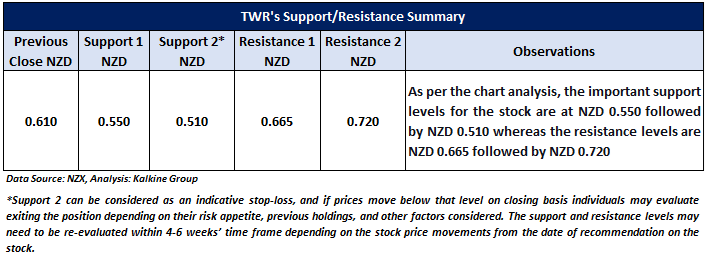

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using P/B multiple-based illustrative relative valuation and the target price so arrived reflects a rise of low double-digit (in % terms). A slight premium has been applied to P/B Multiple (NTM) (Peer Average), considering its healthy capital and solvency position in 1HFY22, along with its digitisation drive and expanding partnerships to gain scale and decent outlook for FY22.

Considering the facts above, a ‘Buy’ recommendation on the stock has been provided at the closing market price of NZD0.61 per share, up 1.67% as of 8 September 2022.

2) Harmoney Corp Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZD75.764 million)

Business Description:

Harmoney Corp Limited (NZX: HMY) provides online direct personal lending services throughout New Zealand and Australia. It provides unsecured personal loans that are easy to access, competitively prices and accessed 100% online.

Outlook:

The key focus of the company in FY23 would be on origination growth as well as loan book growth, cash NPAT growth and to attain net interest margin of more than 10%. It has a high-quality book with low arrears, and a loyal group of increasing customers. Driven by the relevant products as well as the focus towards service, HMY would further take market share from the larger banks and traditional lenders.

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

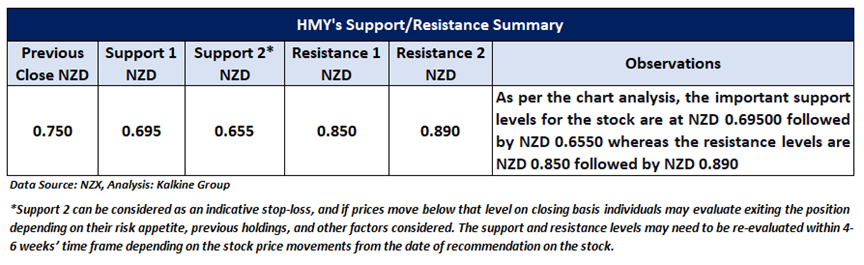

Stock Recommendation

Driven by its extremely automated Stellare® technology platform processing and approving loan applications, HMY is witnessing 85% growth in total loan originations and decline in arrears. Further, the company is targeting to boost conversion prospects by expanding its product offering with innovative features.

Considering the facts above, a ‘Buy’ recommendation on the stock has been provided at the closing market price of NZD0.75 per share, down 1.32% as of 8 September 2022.

3) Australia and New Zealand Banking Group Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$76 billion, Gross Dividend Yield (TTM1): 9%)

Business Description:

Australia and New Zealand Banking Group Limited (NZX: ANZ) is Australia’s 3rd largest banking and financial services group, with operations extending across Australia and offshore in NZ, East Asia, and the Pacific Islands.

Outlook

The bank’s main priorities for FY 2022 include restoring the momentum in the Australian home loans, group simplification as well as productivity, etc. It would continue to adjust the risk appetite, business settings as well as investment priorities. ANZ has been witnessing increased demand from its business customers and it is well-positioned to continue to support them as they are managing in a world of higher inflation and interest rates.

It is conscious of the risks to the domestic as well as global economic outlook. It has maintained the Collective Provision balance at 30th June 2022 of $3.78 billion.

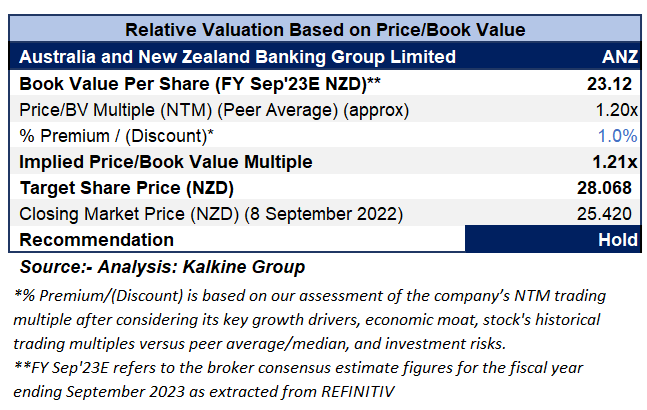

Valuation Methodology: Price/Book Value Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

The stock has been valued using P/B multiple-based illustrative relative valuation and the target price so arrived reflects a rise of low double-digit (in % terms). A slight premium has been applied to P/B Multiple (NTM) (Peer Average), considering the focus towards risk appetite, business settings as well as investment priorities.

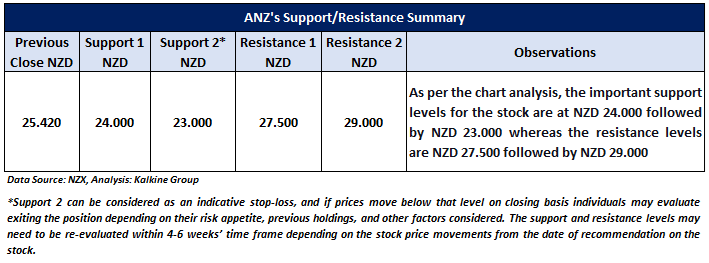

Considering the facts above, a ‘Hold’ recommendation on the stock has been provided at the closing market price of NZD25.420 per share, up 1.97% as of 8 September 2022.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and geopolitical tensions prevailing. Therefore, it is prudent to follow a cautious approach while investing.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance levels is September 8, 2022. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Annual Dividend Yield is on a Trailing Twelve Month (TTM1) basis and are subject to change based on factors such as company performance, stock price changes, etc.

Technical Indicators Defined: -

Support: A level at which the stock prices tend to find support if they are falling, and a downtrend may take a pause backed by demand or buying interest. Support 1 refers to the nearby support level for the stock and if the price breaches the level, then Support 2 may act as the crucial support level for the stock.

Resistance: A level at which the stock prices tend to find resistance when they are rising, and an uptrend may take a pause due to profit booking or selling interest. Resistance 1 refers to the nearby resistance level for the stock and if the price surpasses the level, then Resistance 2 may act as the crucial resistance level for the stock.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is a Financial Advice Provider (“FAP”) and is authorised by a Transitional FAP license issued by Financial Markets Authority (“FMA”) to provide financial advice. Kalkine provides only general financial advice through its research reports following a person becoming a member. The reports contain buy/sell/hold and other recommendations in relation to equity financial products. The recommendations and opinions [on this website] / [in this report] do not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions. If you act on the advice in the research reports, you may have to pay fees, expenses or other amounts (but not to Kalkine). Further information about the complaints and dispute resolution process, as well as information about Kalkine’s duties are available on Kalkine’s website. Please read our Financial Advice Provider (FAP) disclosure statement and Complaints Handling Guide, which are available on the website.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...