I. Sector Landscape and Outlook

As per MBIE.NZ, private, and government focus is trending to electrify the vehicle fleet as ~20% of emissions in NZ come from road transport. The development of new transport technologies, including EV and hydrogen fuel cell cars and biofuels, will improve CO2 emissions and future electricity demand. The government's reference scenario states that EVs will comprise 44% of the light vehicle fleet and 13% of the heavy vehicle fleet by 2050. In the Disruptive scenario, EVs will comprise 74% of the light vehicle fleet, and 45% of the heavy vehicle fleet by 2050, reflecting the falling costs of batteries and EVs. These developments will impact the demand for oil & gas and subsequent pricing.

The share of electricity generation from renewable sources will increase from 84% in 2018 to over 90% and 95% by 2035 and 2050, respectively. In the Reference scenario, 6,250 MW of electricity generation capacity will be needed by 2050, with 55% of the new build being wind generation. For other scenarios, the new build generation capacity is expected in the range of 3,800-10,600 MW across other scenarios in 2050, with capital expenditure in the ambit of $7.0-$24 billion.

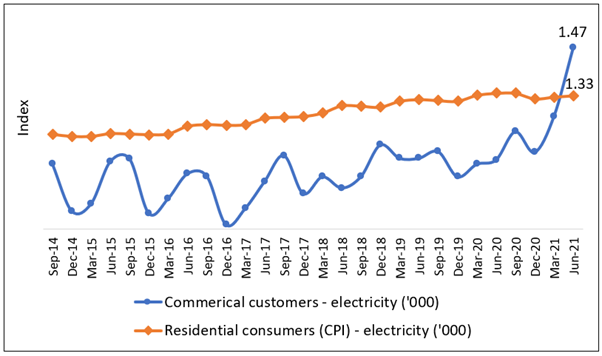

Rising Price is Supporting Electrical Utilities’ Sales to Record High

As per Stats.NZ, the electricity, gas, water, and waste services industry sales increased 32% ($1.7 billion) in the June 2021 quarter, primarily led by electricity generation sales and the high electricity index prices. The output price index for electricity and gas supply touched a record high in the June 2021 quarter, following a significant increase in the March 2021 quarter.

As per Stats.NZ, the continued increase in electricity prices drove a 3.0% rise in prices paid by producers and a 2.6% rise in prices received for production in the June 2021 quarter (from the March 2021 quarter). As a result, prices paid by electricity and gas supply producers increased 17.0% in the June 2021 quarter, while prices received for production rose 14.3%.

Exhibit 1: Trend in Commercial and Residential Electricity Commodities Price Indexes

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

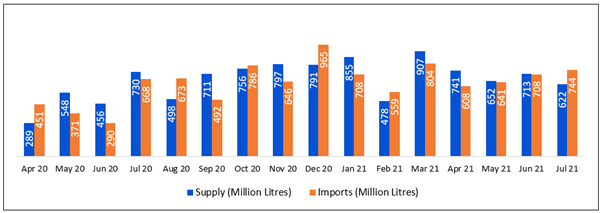

Oil Import Reporting Growth Since May 2021

The oil import reported a month-on-month growth of +5.4%, +10.5%, and +5.1% in May 2021, June 2021, and July 2021, respectively. Moreover, oil is NZ’s largest energy source and therefore has a significant impact on the economy. While there are multiple producing oil fields in NZ, the country is a net importer of oil. NZ’s locally-produced oil is mainly exported due to its high quality and, therefore, high value on the global market. Australia buys most of this oil. The Middle East is the primary source of crude oil, contributing over 50%, followed by Russia and Asia.

Exhibit 2: Monthly Trend in Oil Supply and Import (In Million Litres)

Data Source: This work is owned by the Ministry of Business, Innovation and Employment on behalf of the Crown which are licensed for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

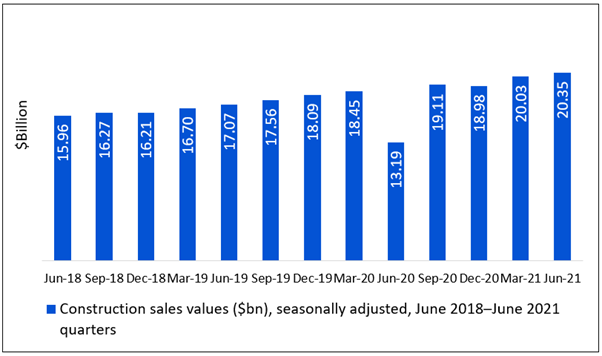

Construction Led the Highest Increase in all 26 Industries, Resulting in Higher Demand for Utilities

As per Stats.NZ, All 26 industries increased in quarterly sales in the June 2021 quarter, rose from the June 2020 quarter levels. Construction marched ahead with a sound percentage rise, up over 50% in June 2021 quarter versus June 2020 quarter. Construction sales increased to $7.2 billion (54%) in the June 2021 quarter versus June 2020 quarter. The construction sector realized strong momentum in the construction activity since the lockdown in April 2020. Other key industries that realized strong momentum include glass, timber, concrete, steel producers, and engineering and architectural services.

Exhibit 3: Trend in Construction Sales

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

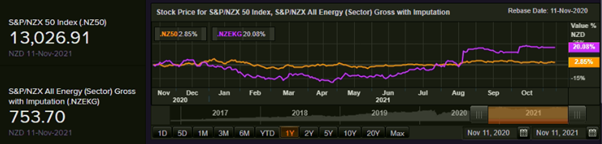

Index Performance:

The S&P/NZX All Energy (Sector) Index generated a 1-year return of ~20.08% versus ~2.85% by the S&P/NZX 50 Index. Therefore, NZX All Energy Index overperformed NZX50 Index by ~17.23% in 1-year.

Exhibit 4: S&P/NZX All Energy (Sector) vs S&P/NZX50 Index

Source: REFINITIV

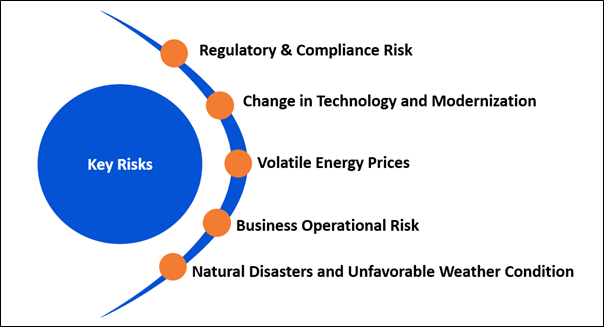

Key Risks and Challenges:

The Government is considering measures to control climate change. One of the measures was banning new low and medium-temperature coal-fired boilers and connecting with the private sector to help it transition away from fossil fuels. This measure will reduce NZ’s emissions profile and provide a phenomenal boost to the clean energy sector. The Government is also planning to phase out coal boilers by 2037. In line with this, attention is on how to phase out other fossil fuels in existing sites through re-consenting processes and best practice requirements in a National Environment Standard

Exhibit 5. Key Risks in Utilities & Energy Sector:

Sources: Analysis by Kalkine Group

Outlook:

The government set the policy direction and urgencies for the NZ energy sector and are focused on net-zero carbon emissions by 2050 by building a more productive, sustainable, and inclusive economy. Future electricity demand will depend heavily on decarbonization and the length of changes in electricity using supply technologies over the next 30 years.

Apart from the sector-specific factors, we have also analysed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

1) Mercury NZ Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$8.26 billion, Gross Dividend Yield: 3.942%)

Business Description:

Mercury NZ Limited (NZX: MCY) is engaged in generating electricity from renewable sources. The company sells electricity through its retail brands - Mercury and GLOBUG.

Outlook

The management has guided achieving EBITDAF of $590 million in FY22 driven by higher earnings from the Turitea wind farm and the benefit of recently acquired Tilt Renewables’ New Zealand assets, and the impact of the company’s Thrive programme. Further, the company expects to provide a fully imputed ordinary dividend of 20.0cps in FY22, a growth of 17.6% over FY21.

On 19 October 2021, the company released its quarterly operational update for the three months ended on 30 September 2021. Hydro generation in Q1FY22 stood at 953GWh, below average, as Waikato catchment inflows remained below average at the 34th percentile. However, the company lifted Lake Taupo hydro storage at 403GWh, 45GWh above average. Further, the customer numbers maintained at 328,000, primarily due to market share. It completed the acquisition of Tilt Renewables NZ wind farms while the commissioning of Turitea is underway. Also, the company released an update on Tararua Wind Farm, where it confirmed the return to service of the five adjacent turbines damaged by fire.

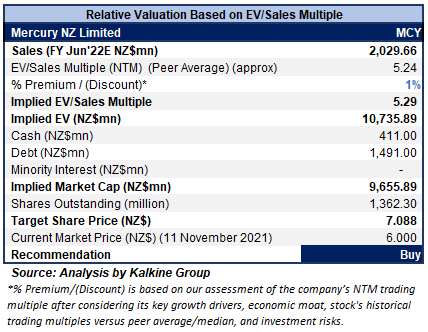

Valuation Methodology: EV/Sales Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

.png)

Stock Recommendation

The stock has been valued using EV/Sales multiple-based illustrative relative valuation, and the target price so arrived reflects a rise of low double-digit (in % terms). A slight premium has been applied to EV/Sales Multiple (NTM) (Peer Average), considering the improved guidance on EBITDAF for FY22, extensive renewable generation pipeline, and the acquisition of Tilt Renewables’ New Zealand that adds more than 1,100GWh to its total annual generation.

For relative valuation, peers like Vector Ltd (VCT.NZ), Infratil Ltd (IFT.NZ), and Genesis Energy Ltd (GNE.NZ), among others, have been considered.

Considering the factors above, the current trading levels, and the associated business risks, we give a “Buy” recommendation on the stock at the current market price of $6.00 per share as of 11th November 2021 (New Zealand Time: 12:57 PM (GMT +12).

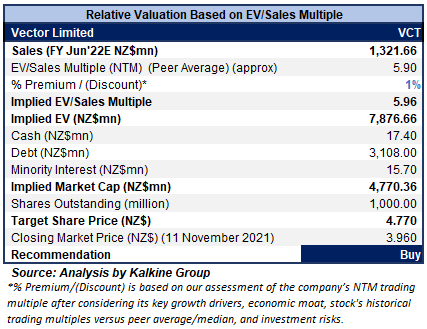

2) Vector Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$3.96 billion, Gross Dividend Yield: 4.738%)

Business Description:

Vector Limited (NZX: VCT) is a network infrastructure company that distributes energy and communication services across Australasia. Further, it has established itself as a top player in the electricity and gas network distribution in New Zealand.

Outlook

The company expects the growth in the electricity and gas connections to sustain. Further, it forecasts a high level of capex to prevail owing to high connection growth in Auckland and advanced meter deployments in Australia and New Zealand, roll out of 4G modems, and advanced gas meters in New Zealand.

As per the release dated 8 November 2021, the company is planning to make an offer of up to NZ$200 million (with the flexibility to accept an additional NZ$100 million) for 6-year, unsecured, unsubordinated, fixed-rate bonds (Bonds) to institutional investors and New Zealand retail investors.

On 21 October 2021, the company released operational performance for the three months ended on 30 September 2021. It reported 592,962 electricity network connections, up 1.7% YoY and 116,840 gas network connections, up 2.0% YoY. Also reported 8.5% YoY growth of advanced meter fleet (total of 1,895,550 now installed across AU/NZ) and over 420,000 advanced meters now installed in the Australian market.

Valuation Methodology: EV/Sales Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

.png)

Stock Recommendation

The stock has been valued using an EV/Sales multiple-based illustrative relative valuation method. A target price with the potential of low double-digit growth (in percentage terms) has arrived. A slight premium has been applied to EV/Sales Multiple (NTM) (Peer Average) considering its strong operational performance in Q1FY22 and decent outlook as growth in the electricity and gas connections is expected to sustain.

For relative valuation, peers like Contact Energy Ltd (CEN.NZ), Infratil Ltd (IFT.NZ), Mercury NZ Ltd (MCY.NZ), among others, have been considered.

Considering the factors above and the current trading levels, we give a “Buy” recommendation on the stock at the closing market price of NZ$3.96 per share, up 0.25% as of 11th November 2021.

3) Genesis Energy Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$3.32 billion, Gross Dividend Yield: 7.208%)

Business Description:

Genesis Energy Limited (NZX: GNE) is a state-owned energy company in New Zealand with a diverse electricity generation portfolio. It is also a significant retailer, which supplies LPG, electricity, and reticulated natural gas via its retail brands of Energy Online and Genesis Energy.

Outlook

The company has signed an agreement with Tilt Renewables for a 75 MW wind farm to be completed by early 2024. Further, signed a deal with CEN whereby GEN will purchase 63 MW of energy for 15 years from 2025.

FY22 Guidance: The company has provided EBITDAF guidance range of $420 million to $440 million, subject to market conditions and capital expenditure guidance of $95 million for FY22.

On 11 November 2021, the company moved forward with joint venture partner FRV Australia, who will bring its expertise in developing utility-scale solar projects with GNE in delivering up to 500MW of solar capacity over the next five years.

On 3 November 2021, the company launched a comprehensive Sustainable Finance Programme (Framework). The programme includes a new Framework, designating an existing NZX listed bond (GNE030) as a Green Bond from 3 November 2021 and a $100 million loan linked to Genesis achieving its sustainability targets.

Valuation Methodology: EV/Sales Based Relative Valuation (Illustrative)

.png)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

.png)

Stock Recommendation:

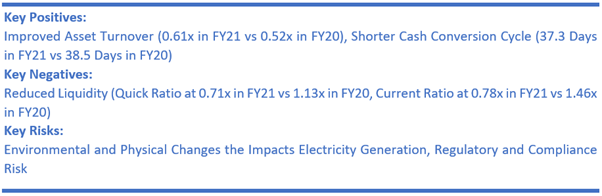

The stock has been valued using an EV/Sales multiple based illustrative relative valuation method and arrived at an upside target price of low double-digit (in percentage terms). The company might trade at a slight discount to its peers’ average, considering a fall in ROE to 1.6% in FY21 versus 2.2% in FY20 and higher debt to equity in FY21 versus FY20.

For relative valuation, peers like Contact Energy Ltd (CEN.NZ), Mercury NZ Ltd (MCY.NZ), and Origin Energy Ltd (ORG.AX), among others, have been considered

Considering the fact above, we give a “Buy” recommendation on the stock at the current market price of NZ$3.16 per share as of 11th November 2021 (New Zealand Time: 12:33 PM (GMT +12).

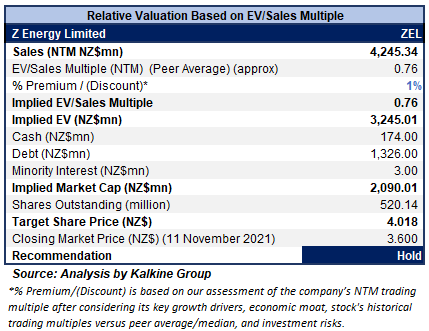

4) Z Energy Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$1.87 billion, Gross Dividend Yield: 5.401%)

Business Description:

Z Energy Ltd (NZX: ZEL) deals in supplying fuel to retail and commercial customers. In addition to this, it provides bitumen to roading contractors. The company’s rich commercial customer base includes airlines, trucking companies, mines, shipping companies, and vehicle fleet operators.

Outlook

The earnings guidance for FY22 is maintained with RC EBITDAF earnings forecasted between $270-$310 million despite ongoing COVID-19 lockdowns. On 11 October 2021, the company announced to enter into a binding Scheme Implementation Agreement (SIA) with Ampol Limited (ASX: ALD). Under this, the company's shareholders would get a cash offer price of NZ$3.78 per share. They would also get the first NZ$0.05 per share of the interim FY22 dividend without adjusting the cash offer price, resulting in an overall value of NZ$3.83 per share.

Valuation Methodology: EV/Sales Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

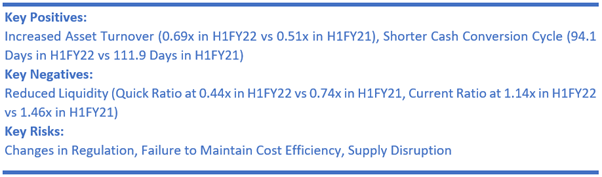

The stock has been valued using an EV/Sales multiple-based illustrative relative valuation, and the target price so arrived reflects a rise of low double-digit (in % terms). Accordingly, a slight premium has been applied to EV/Sales Multiple (NTM) (Peer Average), considering its positive net margin of 4.2% in H1FY22 versus -3.9% in H1FY21 and a jump in EBITDA margin at 9.8% in H1FY22 versus 1.4% in H1FY21.

For the valuation purpose, we have taken peers such as AGL Energy Ltd (AGL.AX), Ampol Ltd (ALD.AX), and New Hope Corporation Ltd (NHC.AX), to name a few.

Considering the factors above, along with its current trading levels and the associated business risks, we give a “Hold” recommendation on the stock at the closing market price of $3.60 per share as of 11th November 2021.

Note 1: The reference data in this report has been partly sourced from REFINITIV.

Note 2: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the analysis has been achieved and subject to the factors discussed above alongside support levels provided.

Technical Indicators Defined: -

Support: A level where-in the stock prices tend to find support if they are falling, and downtrend may take a pause backed by demand or buying interest.

Resistance: A level where-in the stock prices tend to find resistance when they are rising, and uptrend may take a pause due to profit booking or selling interest.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is authorised to provide general advice only. The information on this website does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...