Company Overview: Green Cross Health Limited is a provider of primary healthcare services. The Company supports a range of ancillary services, such as radiology, physiotherapy, midwives and social workers. The Company operates in three segments: Pharmacy services, Medical services and Community Health. The Company's operations are in the pharmacy industry providing pharmacy services through consolidated stores, equity accounted investments and franchise stores. The Medical services segment includes equity accounted medical centers, and support services provided to the medical centers, as well as medical centers outside the Company. The Community Health segment provides services direct to the community to support independent living. The Company's medical network provides general practice services across New Zealand with over 900 doctors, nurses and healthcare practitioners. The Company operates under various brands, such as Unichem, Life Pharmacy, Access and The Doctors.

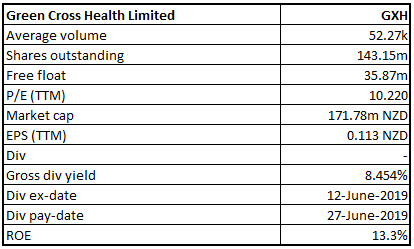

GXH Details

Impressive Growth in the Medical Division: Green Cross Health Limited (NZX: GXH) is a provider of primary health care services, with operations spread across three key business divisions, including Pharmacy, Medical, and Community Health. During the year ended 31 March 2019, the company reported a rise of 5.6% in revenue as compared to the prior corresponding period. Among three business divisions, the company’s medical division reported strong results on the back of organic growth and selective acquisitions. Revenue for the medical division went up by 34% on prior corresponding period. In addition, operating profit for the year witnessed a rise of 20% on prior corresponding period. The Pharmacy division and Community Health division lagged due to certain challenges during the year. Revenue for the Pharmacy division remained in line with the previous year and that for the community health division went up by 9.3%. However, the company maintained a strong financial position with decent cash flows, that helped to deliver dividends to its shareholders. EBITDA and net profit after tax went up by 2.3% and 3.2%, respectively.

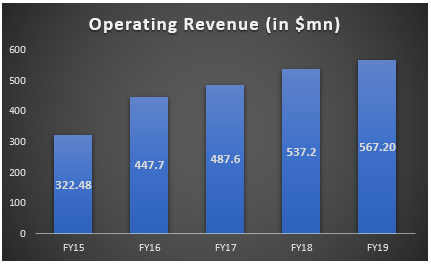

Over a period of 5 years covering FY15-FY19, the company has reported a decent CAGR growth of 15.2% in operating revenue. Operating revenue for FY15 and FY19 came in at $322.48 million and $567.20 million, respectively. The highest uplift in revenue was reported in FY16, with a growth rate of 38.8% on the previous year. The significant rise in revenue was primarily due to acquisitions completed in 2015 that boosted revenue in the Community Health and Medical divisions. In the subsequent years, growth remained moderate, ranging from 5% - 10%.

Net profit over the above-mentioned period has seen mixed trends. In FY16, group PAT increased by ~18% and was impacted by a $1.7 million fair value gain and interest costs approximately $2 million above last year. FY17 also saw double-digit growth in profit and was impacted by a fair value gain amounting to $2.8 million. However, in FY18, profit went down in comparison to FY17, due to a one-off increase in unfunded Leave Liability. FY19 reported a rise of 3.2%, supported by decent growth in the Medical division.

Moving forward, the company believes that its business is well-positioned to provide quality primary health care through its network of health care experts and is confident about earnings growth in the future. It has issued various measures to bring all the businesses back on track all together and is betting upon organic growth and selective acquisitions to push the earnings upwards.

Operating Revenue (Source: Company Reports)

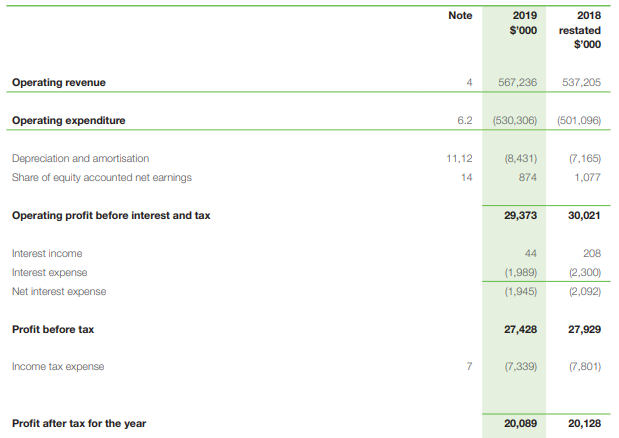

Financial Highlights: During the year ended 31 March 2019, operating revenue amounted to $567.24 million, up 5.6% on prior corresponding period revenue of $537.21 million. EBITDA for the year amounted to $36.9 million, up 2.3% on prior corresponding period. Operating profit came in at $29.4 million, representing a decline of 2.2% on prior corresponding year. Reported Net Profit after Tax Attributable to Shareholders stood at $16.1 million, representing growth of 3.2% on pcp. Growth in net profit was calculated after restating the prior year’s profit on account of two changes made to the Community Health result. These included a $0.7m increase in the provision for alternate leave liability due to a correction in the calculation of this provision and the introduction of IFRS 15 during the year, which required a write off amounting to $0.5m, pertaining to capitalised contract bidding costs. During the year, the company generated an operating cash flow of $29.5 million and reported a reduction of $6.0 million in net debt. At the end of the period, net debt of the company stood at $32.5 million.

FY19 Income Statement (Source: Company Reports)

Performance – Pharmacy Division: Revenue for the Pharmacy division stood at $340 million, almost flat in comparison to the prior corresponding period. Operating profit was reported at $27.3 million, down 5.5% on pcp, as a result of decline in gross margin due to a competitive environment. Same store sales for the period went up by 1.1%. However, the same store gross margin went down by 1.4% due to change in sales mix and increased promotional activity. Key developments in the Pharmacy division included, addition of three licensed stores to the branded group, which now totals 360 Unichem and Life pharmacies. The company continued to optimise its pharmacy investments and made a number of changes to its equity positions in the store network. For instance, during the year, the company sold its equity stake in Life Pharmacy Tauranga and Unichem Timaru Pharmacy. During the year, upgradation of the Life Pharmacy website was largely completed, and the company will now work on driving traffic and sales through the platform. The company’s presence in the China Cross Border e-commerce market was restructured, capitalising on New Zealand’s reputation for health, beauty and wellness products.

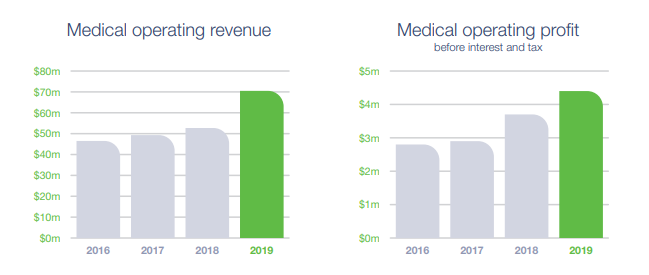

Performance – Medical Division: The Medical division was the highlight of the period, reporting strong growth on the back of benefits from organic growth and selective acquisitions. Revenue for the segment was reported at $70.5 million, up 34% on prior corresponding period. Operating profit stood at $4.4 million, up 20% on prior corresponding period. Patient enrolments in the division increased by approximately 7.6% or 18,000 in comparison to the previous year. The period was also marked by the acquisitions of two businesses located at Waimauku and St Heliers, along with increased investment in two associate medical centre businesses, at New Lynn and Whakatane, moving the ownership to majority interest.

Medical Division Results (Source: Company Reports)

Performance – Community Health Division: Revenue for the segment was reported at $156.5 million, up 9.3% on prior corresponding period. However, operating profit went down to $0.1 million due to continued funding challenges. On review of profitability by contract, the division exited the underperforming Midland DHB contract and won the Greater Wellington contract on new terms. Continued service expansion was seen by the nursing business, i.e., Total Care Health, across multiple regions including Wellington, Whangarei, New Plymouth, Rotorua, and Napier.

From the above section, it can be inferred that performance in FY19 was highly supported by the medical division. Going forward, the company is aiming at continued reviewing the profitability of the contracts under the Community Health division and will work with funders to rebalance the outcomes for loss-making contracts. To beat the competition in the Pharmacy space, it will focus on evolving the product range and will also capitalise on retail growth opportunities. Moreover, the business will also emphasize on margin management across all product categories.

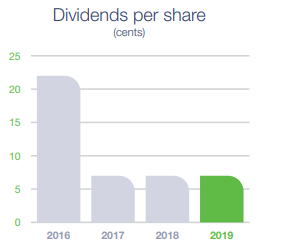

Dividend: During the year, the company declared a fully imputed final dividend of 3.5 cents per share, consistent in comparison to the previous year.

Dividend Trend (Source: Company Reports)

Update on Group CFO: The company recently updated that Ben Doshi, who was supposed to commence his services from 07 October 2019, took charge of the position on 02 October 2019.

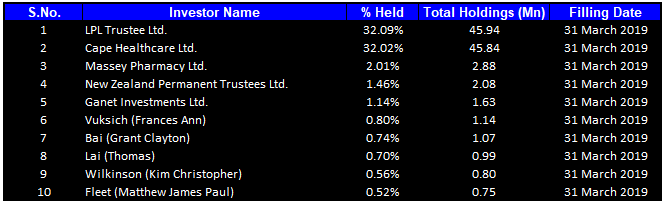

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 72.03% of the total shareholding. LPL Trustee Ltd. is the entity, holding maximum shares in the company at 32.09%. Cape Healthcare Ltd. is the second largest shareholder, with a percentage holding of 32.02%.

Top Ten Shareholders (Source: Thomson Reuters)

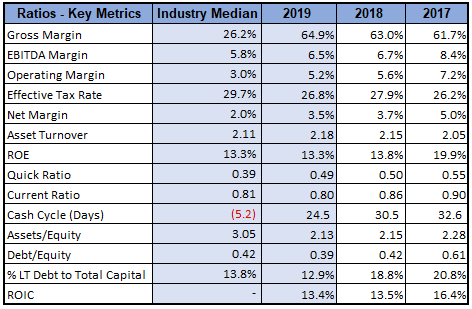

Key Metrics: During FY19, the company’s gross margin stood at 64.9%, higher in comparison to prior corresponding period gross margin of 61.7%. Moreover, the margin was substantially higher than the industry median of 26.2%. EBITDA margin for the year stood at 6.5%, higher in comparison to the industry median of 5.8% and slightly down in comparison to the prior corresponding year EBITDA margin of 6.7%. Net margin came in at 3.5%, as compared to the industry median of 2.0%. Debt to equity ratio was reported at 0.39x, lower in comparison to the prior corresponding period multiple and the industry median of 0.42x.

Key Metrics (Source: Thomson Reuters)

Outlook: Going forward, the company is looking to maximise its market opportunities in China through cross-border e-commerce, under the Pharmacy division. In addition, it will continue to strengthen its connection with New Zealand communities, by working in collaboration with the Ministry of Health, District Health Boards and other funders on new services. Growth in the Medical division is being targeted through network and patient expansion on the back of organic and selected acquisition. As performance under the Community Health division reported extended coverage by Total Care Health nursing business, the company is now aiming for further expansion of the same for complex client needs. Given the above targets, the company is confident about growth in the coming years.

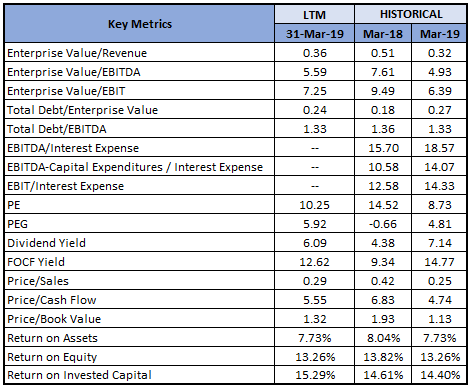

Key Valuation Metrics (Source: Thomson Reuters)

Stock Recommendation: The stock of the company is currently quoting at $1.200 and has a market capitalisation of ~$171.78 million (as at 18 November 2019). In FY19, the company’s performance was majorly supported by remarkable performance by the Medical division, that reported a decent increase in revenue and operating profit along with expansion of the clinic network through acquisition of new businesses. Going forward, the company aims to achieve further operational efficiencies to support growth in patient numbers and promote the delivery of high-quality patient care. As discussed in the outlook section, it has also come up with various corrective measures to increase the pace of growth in other business divisions. Considering the decent financial performance in FY19, a conservative balance sheet to support dividend payments, expected continued growth from the Medical division and corrective measures with respect to the Pharmacy and Community Health divisions along with improved earnings, we expect a high single digit growth in the stock in the next 12 months. Thus, we recommend a “Buy” rating on the stock at the current market price of $1.200, up 4.35% on 18 November 2019.

GXH Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...