New Zealand's GDP was under pressure during 2020 due economic slowdown on the back of outbreak of the COVID-19. However, based on Reserve Bank’s monitory policy, annual GDP growth for trading partners is assumed to reach 4.8% in late 2022 and to gradually decline thereafter. This projected growth will be heavily backed by foreign trade, foreign tourists, and economic policies among other factors.

The consumer staples sector encompasses of food and beverage manufacturing, household and personal care products, and food and staples retailing. As per Observatory of Economic Complexity (OEC), in 2019 NZ ranked 51 economy in the world in terms of GDP and exported a total of US$40.5 billion, placing it at number 55 in total exports. The main export items in 2019 includes: concentrated milk (14.2% of total export), sheep and goat meat (6.49%), rough wood (5.70%), butter (5.66%), frozen bovine meat (5.16%), cheese (3.33%), malt extract 3.31%, wine (3.11%) and other fruits (3.79%) among other items. To keep the export momentum going, the Government has emphasised to penetrate Asian market to cover larger market destination, which will add more value to organized companies over unorganized companies. Besides, the annual food price inflation reached at 4.4% in April 2020, which was the largest annual rise in more than eight years.

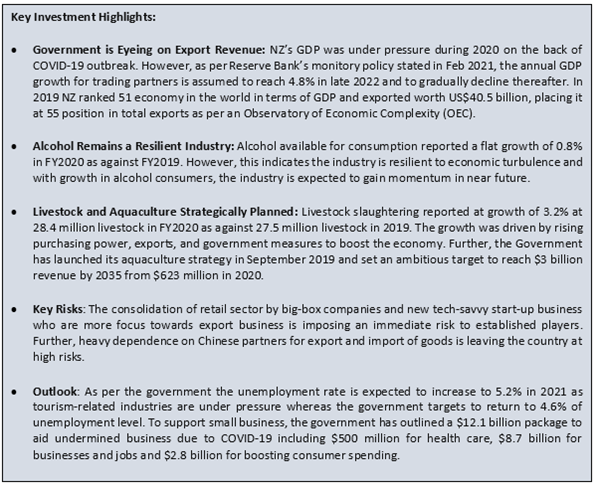

Exhibit 1: S&P/NZX All Consumer Staples (Sector) v/s S&P/NZX All Index (Five-Year Chart)

Source: S&P Global; Chart Created by Kalkine Group

The S&P/NZX All consumer staples sector has outperformed the S&P/NZX All Index with a 5-year return (18 March 2016 - 18 March 2021) of 16.13% as against the index’s 5-year return of 9.79%.

New Zealand exports its food and primary products to more than 200 markets around the world with the country’s primary sector exports accounting for more than 80% of the overall export of goods. The primary industries have logged a growth of 4.6% in September 2020 quarter supported by mining and forestry and logging sub sectors which registered growth of 16.1% and 23.2% respectively as per Stats NZ. While, in the in the December 2020 quarter, Primary industries witnessed a marginal decline of 0.6%.

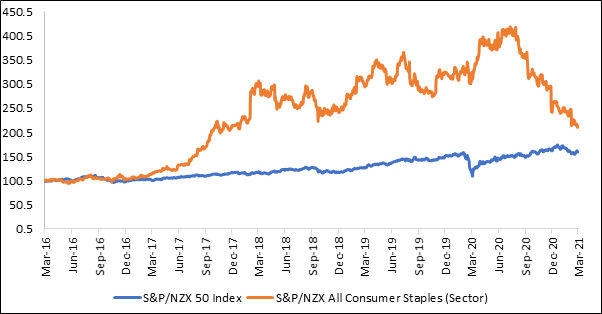

Albeit Traction Was Witnessed in Disposable Income in FY20

Rise in domestic disposable income also fuel demand of the consumer staples sector. Notably, the country’s average annual household income (gross) registered a growth of 3.6% for the year ended June 2020 to $107,731 compared with $103,991 for the year ended June 2019. Resultantly, the New Zealand’s average annual household disposable income (after tax and transfer payments) witnessed a growth of 3.9% for the year ended June 2020 to $86,626 from $83,406 for the year ended June 2019 as per Stats NZ. The benefits of easing in Covid-19 related restrictions and an improvement in economic activities is likely to provide further fillip to consumer spending going ahead.

Exhibit 2: Household Disposable Income, By Household Income Sources

Source: Stats NZ; Chart Created by Kalkine Group

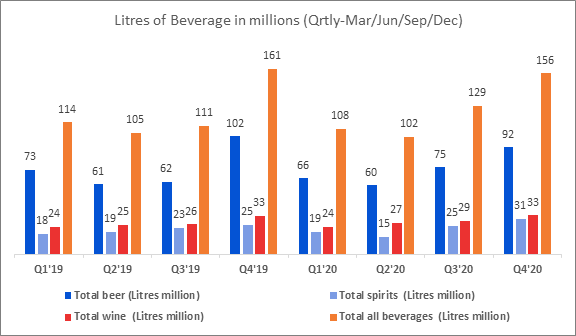

As per New Zealand Stats, alcohol available for consumption reported a flat growth of 0.8% in FY2020 as against FY2019 as shown in Exhibit 3. The growth in the alcoholic beverages’ consumption was powered by increase in the volume of wine as well as spirits (including spirit-based drinks) which reported a growth of 4.3% and 5.2% to 113 million liters and 89 million liters, respectively. However, decline in the volume of beer during the period under consideration by 1.7% to 293 million liters has capped the rise in the overall volume of alcoholic beverages consumption.

Exhibit 3. Alcohol Available for Consumption Replicated Trend of 2019 in 2020 – Consistent levels

Data Source: infoshare.stats.govt.nz; Chart Created by Kalkine Group

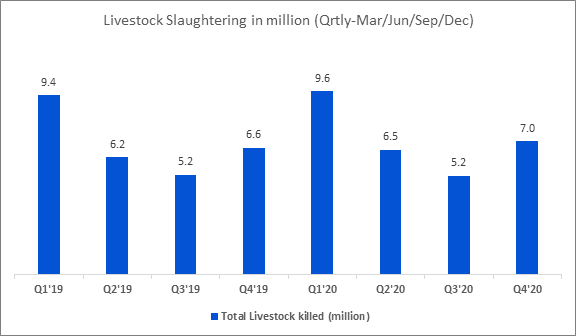

As per NZ stats, livestock slaughtering reported at growth of 3.2% at 28.4 million livestock in FY2020 as against 27.5 million livestock in 2019 as shown in Exhibit 4. The growth was driven by rising purchasing power, export, and government measures to boost the economy back to growth trajectory.

Exhibit 4. Livestock Slaughtering in 2019 and 2020 – building momentum for future growth

Data Source: infoshare.stats.govt.nz; Chart Created by Kalkine Group

Further, the New Zealand Government has launched its aquaculture strategy in September 2019 and set an ambitious target to reach $3 billion revenue by 2035 from $623 million in 2020. This is expected to streamline the channel and accelerate the dollar business at multiple fronts for domestic as well as international customers.

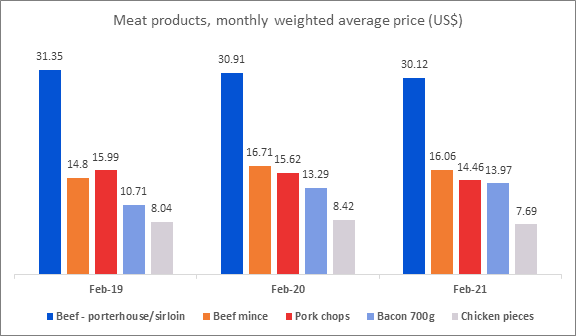

Exhibit 5. Meat Prices at low levels indicating bottom-out in February 2021

Data Source: stats.govt.nz; Analysis by Kalkine Group

Due to lower demand, the prices of chicken seems to be cheaper meat choice, approximately 50% of beef mince and less than one-third of the cost of steak, as shown in Exhibit 5. However, it is the most popular meat choice with shoppers. Further, the apple, chocolate biscuits, grilling or frying beef, and yoghurt prices have veered down sharply by 26%, 11%, 5.6%, and 6.5% respectively.

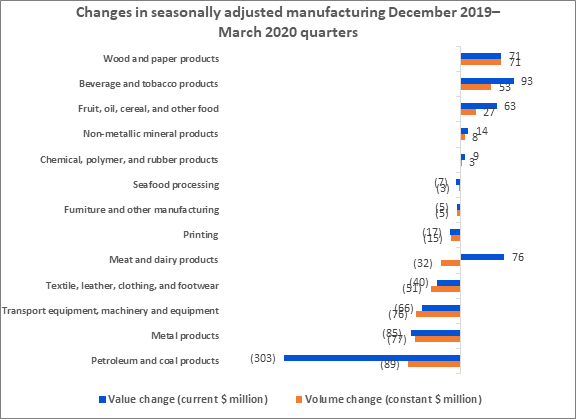

Exhibit 6. Changes in seasonally adjusted manufacturing sales, values and volumes indicating a revival

Data Source: stats.govt.nz; Analysis by Kalkine Group

The adjusted data from December 2019 to March 2020 represents the change in money value and volume for the said period, as shown in Exhibit 6. Beverage & tobacco products and fruit, oil, cereal, and other food have shown a positive shift whereas Meat & dairy products and Textile, leather, clothing, and footwear has reported a negative volume for the said period.

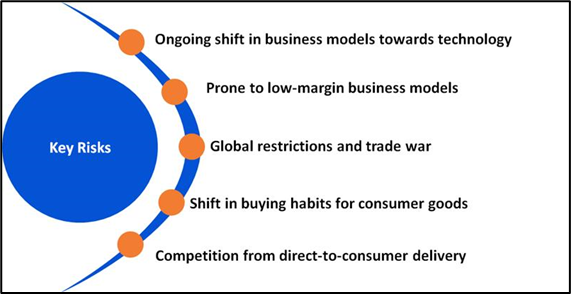

Key Risks and Challenges:

The consolidation of retail sector by big-box companies and new tech-savvy start-up business who are more focus towards export business is imposing an immediate risk to established players. To retain and grow the business, the established players must pace up with technology and market scenario. Further, heavy dependence on Chinese partners for export and import of goods is leaving the country at high risk. China alone comprise of 24.23% of trade followed by Australia 15.92%, USA 9.60%, Japan 6.08%, and Republic of Korea 3.04% among top five export and import partners.

Further, the pricing pressure by heavyweights are trying to cut small players and dominate the market, placing at high risk to companies who have lower margins compared to established players. In line with this, private label competition is attempting to capture higher margin. Additionally, competition from direct-to-consumer delivery with strategic marketing backed by venture capital, is diluting the market share by selling staples directly to the consumer. Moreover, as per Reserve bank of New Zealand the strong Chinese economy is expected to continue to underpin demand for New Zealand’s exports, particularly dairy products.

Exhibit 7. Key Risks in Consumer Staples Sector:

Sources: Analysis by Kalkine Group

Outlook:

New Zealand expressed optimism about the economic prospects. The household living-costs price indexes reported strength in Q4FY2020, where Fruit and vegetables reported at 1081 units (vs 1005 unites in Q4FY2019), Grocery food at 1017 unites (vs 1008 unites in Q4FY2019), Alcoholic beverages at 1063 unites (vs 1038 unites in Q4FY2019) and Cigarettes and tobacco at 1817 units (vs 1632 unites in Q4FY2019) among others. As per Reserve Bank of New Zealand, the unemployment rate is expected to increase to 5.2% in 2021 as tourism-related industries continues to be under pressure whereas the government targets to return to 4.6% of unemployment level for the future period.

Further, to support small business a cash-flow loan scheme is administered by the government where up to $100,000 loan amount is fixed for the firms employing 50 or fewer full-time equivalent employees. The loan will be for a maximum of 5 years, with repayments not due in the first 2 years. The government has outlined a $12.1 billion package to aid undermined business due to COVID-19. This comprised of $500 million for health care industry, $8.7 billion in support for businesses and jobs and $2.8 billion for income support and boosting consumer spending. These measures taken by government and big businesses is expected to positively impact the consumer staples business.

Apart from the sector-specific factors, we have also analyzed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

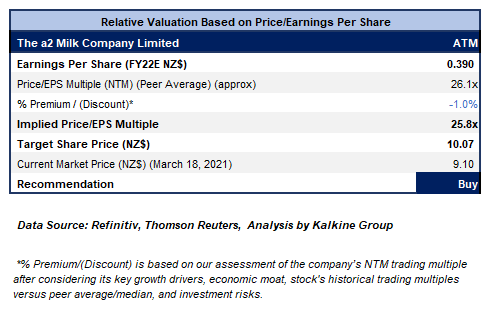

1. The a2 Milk Company Ltd (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$6.7 billion)

Business Description:

The a2 Milk Company Ltd (NZX: ATM) single-mindedly pioneers scientific understanding, operational know-how as well as commercialisation of the premium a2 Milk brand products throughout the world.

Outlook

ATM remains assured in the underlying fundamentals of the business and it continues to focus on strengthening its supply chain capability.

In order to attain long term growth, ATM continues to invest towards brand building and in the capability. Meanwhile, the company has guided its FY21 revenue of $1.4 billion with the group’s FY21 EBITDA margin in the range of 24% to 26% (excluding MVM acquisition costs).

The Company’s balance sheet position stood robust with zero debt and a healthy cash position of $774.6 million. This will provide leeway for the company in tapping growth opportunities. However, the investors should keep an eye on related risks like unprecedented levels of uncertainty and volatility due to COVID-19.

Valuation Methodology: P/E Based Relative Valuation (Illustrative)

We have applied P/E based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied a slight discount Price/EPS Multiple (NTM) (Peer Average) considering that the pace of recovery in the daigou/reseller channel as well as in the CBEC channel has been slower than was expected.

Considering the expected upside and robust balance sheet, we give a “Buy” recommendation on the stock at the current market price of $9.10 per share, down by 2.78% on 18th March 2021.

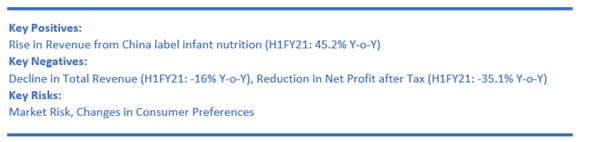

2. New Zealand King Salmon Investments Ltd (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$214.03 million)

Business Description:

New Zealand King Salmon Investments Ltd (NZX: NZK) is the pioneer in marine salmon farming in New Zealand.

Outlook

The company remains hopeful of recovery in sales demand later in the year which will surpass the company’s ability to supply. Further, it anticipates to clear excess inventories of salmon by the middle of calendar year 2021. Meanwhile, NZK has cultivated new sales channels in North America which includes online delivery, fishmongers and specialty retail.

In order to support recovery and growth, in both foodservice and new retail opportunities, the company is investing in additional sales resource in key export markets.

However, the investors should keep an eye on related risks like uncertain macroeconomic climate and higher inventories level.

Valuation Methodology: P/E Based Relative Valuation (Illustrative)

.png)

We have applied P/E based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied a slight discount Price/EPS Multiple (NTM) (Peer Average) considering Covid-19 impact on both domestic and export markets especially due to the nature of its marine farming business.

Considering the expected upside and better liquidity position, we recommend a ‘Buy’ rating on the stock at the current market price of $1.540 per share, up by 2.67% on 18th March 2021.

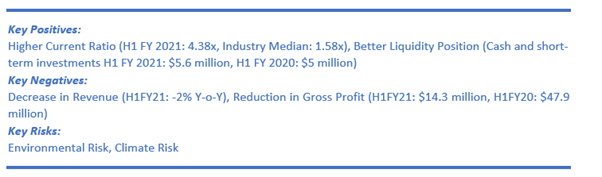

3. Fonterra Co-operative Group Ltd (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$8.1 billion, Gross Dividend Yield: 0.990%)

Business Description:

Fonterra Co-operative Group Ltd (NZX: FCG) is a multinational dairy company, which is owned by 13,000 NZ dairy farmers.

Outlook

In order to accelerate the demand for the foodservice products in the US, FCG has entered into a sales and marketing agreement with one of America’s leading dairy co-operatives, Land O’Lakes, Inc. The company has reaffirmed the forecast farmgate milk price range of $7.30 - $7.90 per kgMS and forecast normalised earnings guidance of 25-35 cps.

Technical Overview:

Monthly Chart:

.png)

Note: Yellow color line indicates trend-line while purple color line depicts RSI (14-period). Green color histograms at the bottom of the chart indicates weekly volumes and the pink color line shows 21-period SMA and the sky blue color line shows 50-period SMA.

FCG prices are slowly trying to recover from the low made in August 2019 and currently trading near 52-week high. Prices are currently trading above 21-period SMA and 50-period SMA that indicates prices are trading in a bullish territory. Prices broke the symmetrical triangle pattern in February 2021 and are sustaining above the breakout point from last two months. Volumes are showing increasing trend along with surging prices which support the existing price trend. RSI (14) is hovering at 65 on the monthly time frame chart showing strong momentum of the stock prices. Immediate resistance levels of the stock are NZ$ 5.59 and NZ$5.90. On the lower side, prices might take support at NZ$ 4.85 and NZ$ 4.30.

Considering the technical analysis and rise in net cash flow, we give a “Hold” recommendation on the stock at the current market price of $5.070 per share, up by 0.40% on 18th March 2021.

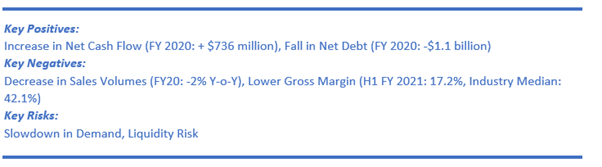

4. Delegat Group Ltd (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$1.5 billion, Gross Dividend Yield: 1.574%)

Business Description:

Based in New Zealand, Delegat Group Ltd (NZX: DGL) happens to be the New Zealand's 4th largest wine company (by the litres of wine sold).

Outlook

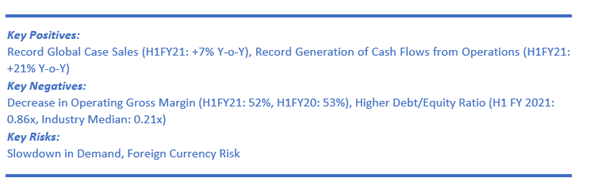

The company is on target to achieve global case sales for the full year of 3,391,000, reflecting a rise of 3% on last year. DGL has generated record cash flows from operations of $42.9 million in H1FY21, a growth of 21% YoY. Resultantly, the group’s net debt stood at $254.1 million at 31 December 2020, a reduction of 5% as compared to the figure at December 2019.

Valuation Methodology: P/E Based Relative Valuation (Illustrative)

.png)

We have applied P/E based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied a slight premium to Price/EPS Multiple (NTM) (Peer Average) considering that the company is on target to achieve the global case sales for the full year and reduction in net debt.

Considering the expected upside and record generation of cash flows from operations, we give a “Hold” recommendation on the stock at the current market price of $15 per share on 18th March 2021.

Comparative Price Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...