I. Sector Landscape and Outlook

As per the Ministry for Primary Industries (MPI), food and fibre sector export revenue is anticipated to reach the $52.2 billion by the end of 30 June 2022, as farmers, growers, fishers, foresters and others are delivering quality products for Kiwis and international consumers despite challenges of COVID-19. Following the current performance, the agency anticipated food and fibre export revenue to hit $56.8 billion by 30 June 2026. Further, the government is pushing free trade agreement (FTA) with major exporting countries to grow its export market.

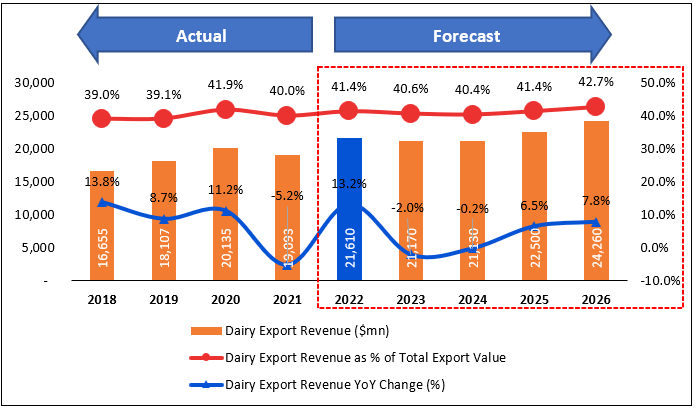

Higher Demand for Dairy Products in Global Market

As per MPI, the dairy export revenue is projected to grow by 13% in FY22 over FY21 and reach a record high of $21.6 billion, primarily driven by higher global demand and decreased supply from other key dairy exporting regions. The YoY increase in the average export price of Whole milk powder in FY22 to $5,760 per tonne from $4,613 per tonne (up 25% YoY) supported the overall export revenue growth. A YoY rise followed this growth momentum in the average export price of Butter, AMF, and cream in FY22 to $8,590 per tonne from $6,374 per tonne (up 35% YoY). All dairy product categories, excluding infant formula, are projected to surpass their 5-year average in export revenue.

Exhibit 1: Trend in Dairy Export Revenue 2018–26 (Year to 30 June, NZ$ million)

Data Source: This work is based on/includes the Ministry for Primary Industries data which are licensed under Crown for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

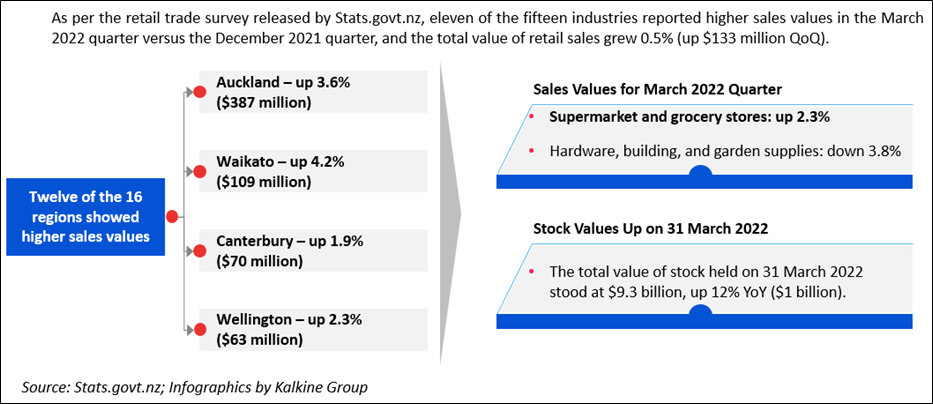

Rise in Food and Beverage Services Industry in the Retail Trade Survey for March 2022 Quarter

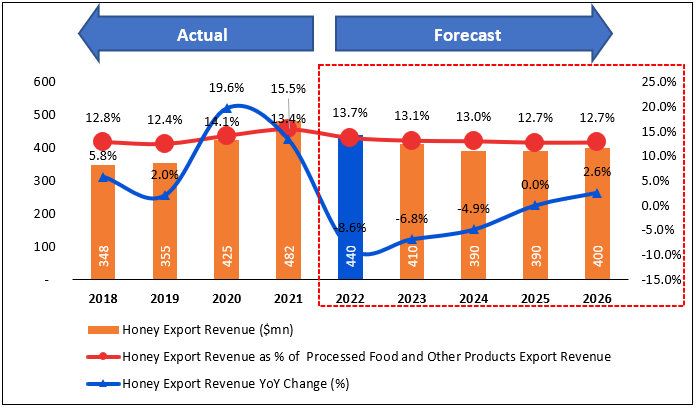

Honey to Enter the New Zealand-United Kingdom Free Trade Agreement

As per MPI, the export of wine, honey, and onions is projected to enter the UK duty-free under the New Zealand-United Kingdom Free Trade Agreement (NZ-UK FTA) that is expected to be in force by the end of 2022. The export revenue of honey of all types is projected to reach $440 million in FY22, down $42 million YoY as FY21 honey export revenue was one-off supported by higher demand from the international market during the COVID-19 period. The total export volume is forecast to fall by 15% to ~11,000 tonnes for FY22.

Exhibit 2: Trend in Honey Export Revenue 2018–26 (Year to 30 June, NZ$ million)

Data Source: This work is based on/includes the Ministry for Primary Industries data which are licensed under Crown for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

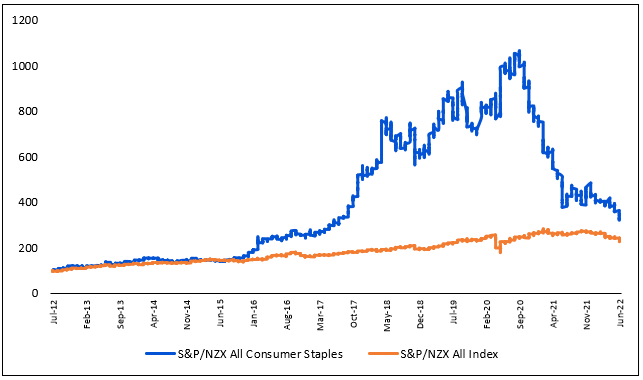

Index Performance:

The S&P/NZX All Consumer Staples Index generated a 10-year return of ~228.4% versus ~125.2% by the S&P/NZX All Index. Therefore, S&P/NZX All Consumer Staples Index overperformed S&P/NZX All Index by ~103.2% in 10-year.

Exhibit 3: S&P/NZX All Consumer Staples Index vs S&P/NZX All Index

Source: REFINITIV, Chart Created by Kalkine

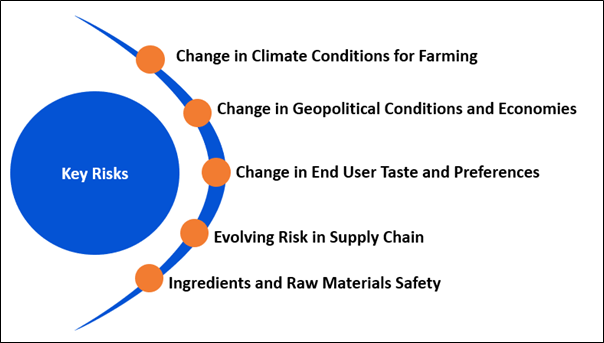

Key Risks and Challenges:

Honey exporters are exposed to near-term headwinds relating to the demand picture, which has to be evaluated in the post-COVID-19 scenario. Further, the vital parts of food ecosystems are becoming more capital-intensive, vertically integrated and concentrated in fewer hands. Also, crises and natural disasters are growing in number and intensity.

Exhibit 4. Key Risks in Consumer Staples Sector:

Source: Analysis by Kalkine Group

Outlook:

The food and fibre sector continues to drive the economic recovery from COVID-19 for New Zealanders, led by the initiative taken by the government and sector roadmap Fit for a Better World. The government is investing in 195 projects through the Sustainable Food and Fibre Futures fund in the food and fibre sector to deliver outcomes.

The momentum is building on trade partnerships as the government opens new market opportunities like the historic FTA with the United Kingdom in March 2022. This deal is expected to eliminate all tariffs on New Zealand exports (duties removed on 99.5% of current trade from entry into force). This action is expected to boost New Zealand’s GDP by $1 billion. With the ongoing implementation of FTA with China, most NZ dairy products to China are now duty-free, which is expected to drive savings of $180 million per annum.

Apart from the sector-specific factors, we have also analysed three NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

1) The a2 Milk Company Limited (Recommendation: Buy, Potential Upside: Low Double-Digit (M-Cap: NZ$3.67 billion)

Business Description:

The a2 Milk Company Limited (NZX: ATM) is engaged in the branded milk business, and it produces from cows that produce only the A2 protein type. It has products and trading activities across New Zealand, Australia, Greater China, North America, and selected emerging markets.

Outlook:

The company projects improved H2FY22 revenue more than H2FY21, mainly led by growth in China label and English label IMF. However, this revenue growth is not anticipated to translate into better earnings as the company is significantly investing in brand building and other reinvestment strategies for change. Meanwhile, the input costs are higher in FY22 than in FY21, partially nullified by better pricing from November 2021.

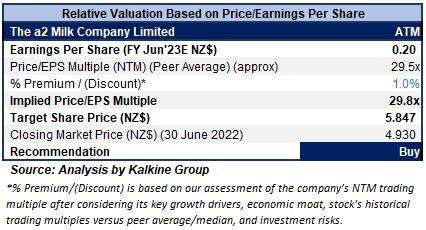

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

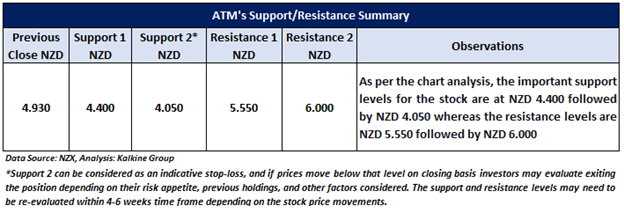

Stock Recommendation

The stock has been valued using P/E multiple-based illustrative relative valuation and the target price so arrived reflects a rise of low double-digit (in % terms). A slight premium has been applied to P/E Multiple (NTM) (Peer Average), considering price improvement in Milk products and higher demand from China.

Considering the facts above, a “Buy” recommendation on the stock has been provided at the closing market price of $4.93 per share, down 0.20% as of 30 June 2022.

2) Scales Corporation Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$619.41 million, Annual Dividend Yield (TTM)1: 5.930%)

Business Description:

Scales Corporation Limited (NZX: SCL) is engaged in the agri-business. It operates in three divisions that include horticulture, logistics, and food ingredients, in adjacent primary sectors.

Outlook

The company anticipates FY22 Food Ingredients earnings to remain in line with 2021. The board has reconfirmed guidance for Underlying Net Profit Attributable to Shareholders to be in the ambit of $23.5 million to $28.5 million in FY22, indicating an Underlying Net Profit in the range of $30.5 million to $35.5 million and an Underlying EBITDA in the field of $62 million to $67 million.

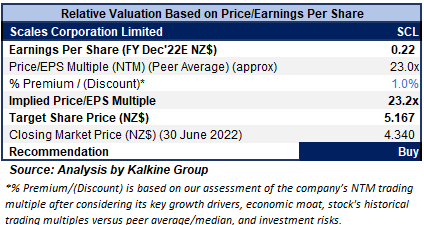

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

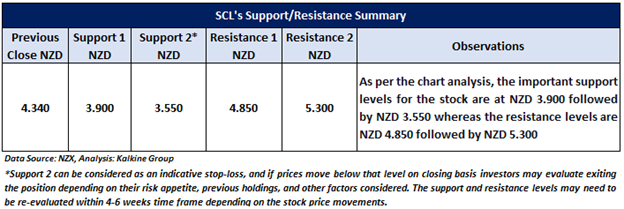

Stock Recommendation

The stock has been valued using P/E multiple-based illustrative relative valuation, and the target price reflects a rise of low double-digit (in % terms). A slight premium has been applied to P/E Multiple (NTM) (Peer Average), considering business diversification and a decent outlook.

Considering the facts above, a “Buy” recommendation on the stock has been provided at the closing market price of $4.34 per share, down 2.47% as of 30 June 2022.

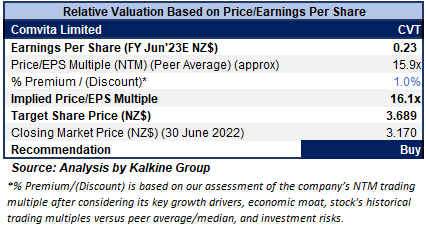

3) Comvita Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$221.16 million, Annual Dividend Yield (TTM)1: 1.96%)

Business Description:

Comvita Limited (NZX: CVT) is one of the leading global players in producing Manuka honey. The company has a decent geographical presence across Australia, New Zealand, China, and North America.

Outlook

The company anticipates an improved FY22 result, driven by a focused business model, cost-controlling measures, and investment in the brand and execution chain. Meanwhile, the company's long-term guidance for 2025 is on track, driven by long-term brand and business building activity to drive revenue, margin and earnings growth. The EBITDA is projected to be in the range of $27-$30 million for FY22. The company announced a fully imputed interim dividend of 2.5 cps, reflecting the strengths of its guidance despite ongoing Covid disruptions.

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using P/E multiple-based illustrative relative valuation, and the target price reflects a rise of low double-digit (in % terms). A slight premium has been assigned to P/E Multiple (NTM) (Peer Average), considering strategic investments in digitisation with its new web platform's enhanced functionality. Also, the company plans to increase digital sales to 50% (currently 33%) of total revenue by FY25 at accretive gross margins.

Considering the facts above, a “Buy” recommendation on the stock has been provided at the closing market price of $3.17 per share, down 0.63% as of 30 June 2022.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and geopolitical tensions prevailing. Therefore, it is prudent to follow a cautious approach while investing.

Note 1: The reference data in this report has been partly sourced from REFINITIV.

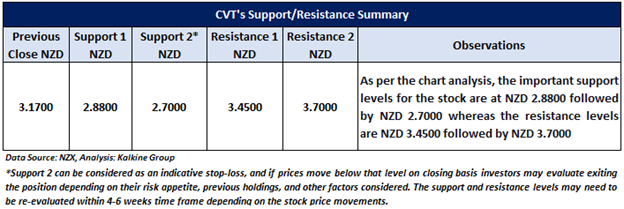

Note 2: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the analysis has been achieved and subject to the factors discussed above alongside support levels provided.

Note 3: Annual Dividend Yield is on a Trailing Twelve Month (TTM1) basis and are subject to change based on factors such as company performance, stock price changes, etc.

Technical Indicators Defined: -

Support: A level at which the stock prices tend to find support if they are falling, and downtrend may take a pause backed by demand or buying interest.

Resistance: A level at which the stock prices tend to find resistance when they are rising, and uptrend may take a pause due to profit booking or selling interest.

Stop-loss: In general, it is a level to protect further losses in case of any unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is authorised to provide general advice only. The information on this website does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...