.png)

I. Sector Landscape and Outlook

The Monetary Policy Committee concluded to increase the Official Cash Rate (OCR) to 0.50% and reduced the level of monetary stimulus to maintain low inflation and strengthen employment. The global economy is recovering at its pace, primarily supported by accommodative monetary and fiscal stance and increasing vaccination rates facilitating relaxation of mobility restrictions. The CPI inflation is expected to rise above 4% in the near term before returning to a 2% midpoint over the medium term.

Further, the government announced a $3.8 billion fund to speed up the pace and scale of homebuilding. The prime component of the Housing Acceleration Fund (HAF) is to boost the mix of private-sector and government-led developments in areas with the highest housing supply and affordability challenges. Further, the government plans to support Kāinga Ora to borrow $2 billion extra to accelerate land acquisition.

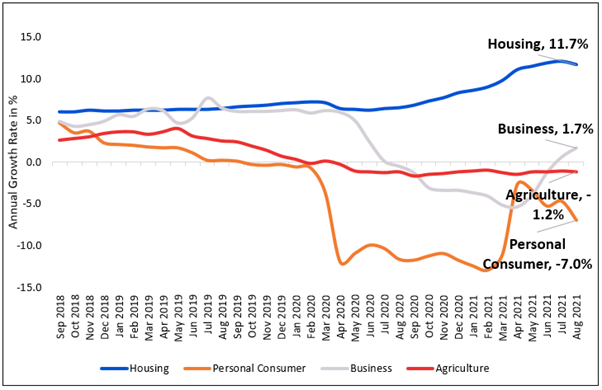

Housing Lending Increased in August 2021

As per the Reserve Bank of New Zealand (RBNZ), total housing lending stock expanded by $1.2 billion (0.4%), the lowest rise since the negative growth recorded in April 2020. Meanwhile, the annual increase in lending moved down slightly from 12.1% to 11.7% in August 2021. Also, the total personal consumer lending stock was down by $511 million (-3.6%). Further, the entire business lending stock increased for the fourth consecutive month, up by $796 million (0.7%), and the annual growth rose to 1.7% from 0.6%.

Exhibit 1: Trend in Lending Since 2017 – Banks and NBLIs

Data Source: This work is based on/includes rbnz data which are licensed by rbnz.govt for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

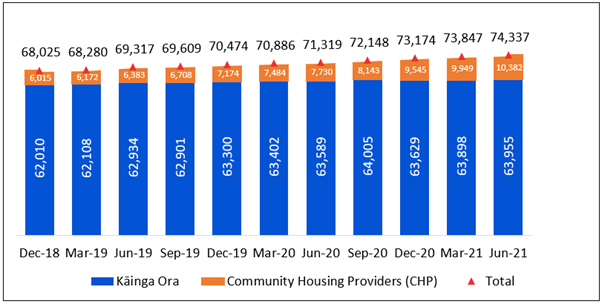

Increased Demand for Public Housing in June 2021 Quarter

As per the public housing quarterly report June 2021, published by the Ministry of Housing and Urban Development, the country had 74,337 public houses, an increase of 490 from the previous quarter (73,847 in March 2021). Within this, 63,955 state houses were provided by Kāinga Ora (who provide accommodation to over 180,000 people), and 10,382 community houses were supplied by 60 registered Community Housing Providers across NZ. Community houses are owned, leased, or managed by non-governmental organisations (NGOs) or independent government subsidiaries. Over the June quarter of 2021, registered CHPs have grown their total tenancies by 433.

Exhibit 2: Trend in Public Houses, Tenanted by People Who are Eligible

Data Source: This work is based on/includes hud.govt.nz which are licensed by Te Tūāpapa Kura Kāinga - Ministry of Housing and Urban Development on behalf of the Crown for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

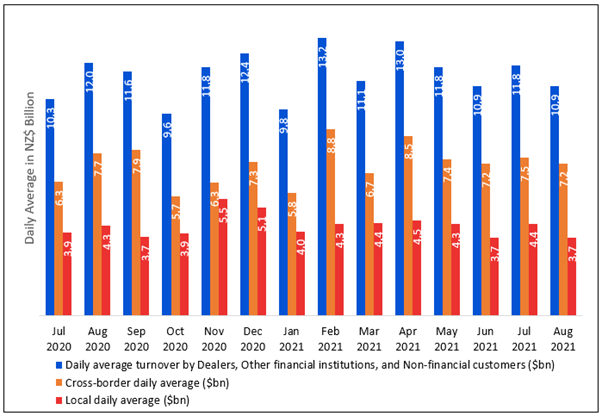

Foreign Exchange Turnover Expected to Rebound

As per the RBNZ, the average daily foreign exchange transactions from Dealers, Other financial institutions, and Non-Financial Customers in August 2021 stood at $10,899 million, against $11,966 million in the same month last year. This reflects decline in offshore capital investment into NZ and the associated lower global profile of the NZ dollar. As a result, foreign exchange trading in NZ has also reduced, mainly in line with global trends. However, expected recovery in the financial market, improved consumer sentiments, better economic data, controlled COVID-19 circumstances, may increase the inflow of foreign exchange in the NZ market.

Exhibit 3: Daily Average Foreign Exchange Turnover Trend since Jul 2020 - Aug 2021

Data Source: This work is based on/includes rbnz data which are licensed by rbnz.govt for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

Index Performance:

The S&P/NZX All Financials Index generated a 1-year return of ~43.06% versus ~4.03% by the S&P/NZX 50 Index. Therefore, S&P/NZX All Financials Index overperformed S&P/NZX 50 Index by ~39.03% in 1-year.

Exhibit 4: S&P/NZX All Financials Index vs S&P/NZX 50 Index

Source: REFINITIV

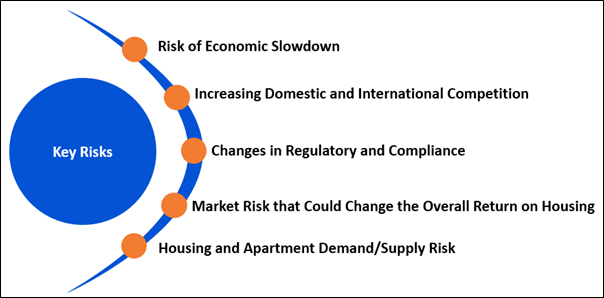

Key Risks and Challenges:

As per RBNZ, the recent house loan borrowers are vulnerable to decline in house price, while banks are less at risk. A significant reduction in households’ housing wealth would reduce consumption outlay, negatively impacting the commercial sector and banks’ business borrowing portfolios. A more substantial fall in house prices indicates a more comprehensive economic downturn.

Further, the RBNZ anticipates vulnerabilities in the financial system. The regulator is seeing the impact of lower global interest rates resulting in the higher risk-taking appetite of the consumers and higher asset prices, most visible in higher house prices.

Exhibit 5. Key Risks in Financial and Real-Estate Sector:

Sources: Analysis by Kalkine Group

Outlook:

As per the RBNZ, global monetary and fiscal levels gained strong momentum, strengthening international spending and investment. In addition, increasing vaccination rates across countries have facilitated economic impetus. The increase in global development has continued to boost demand and prices for NZ’s export commodities. Also, multiple small and big businesses are indicating better confidence to invest and hire additional workers. These factors are expected to strengthen further and provide sustainable growth to the companies in real estate and banking sectors.

As per the ‘Wellbeing Budget 2021’, the government has provided a $3.8 billion Housing Acceleration Fund to deliver on key initiatives that would boost NZ’s economic recovery, rebuild and long-term wellbeing.

Apart from the sector-specific factors, we have also analysed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

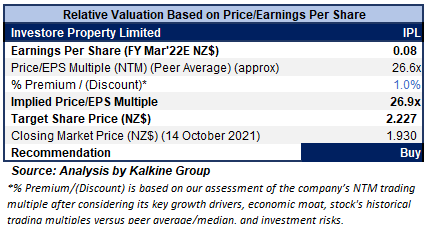

1) Investore Property Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$710.50 million, Gross Dividend Yield: 4.583%)

Business Description:

Investore Property Limited (NZX: IPL) invests in quality, large format retail properties throughout New Zealand and manage shareholders’ funds to maximise total returns over the medium to long-term.

Outlook:

The company extended its focus on targeted growth to better the portfolio and maximise returns; provide smooth delivery of development opportunities at Waimak and continue refurbishment projects with Countdown and other key tenants. As a result, the FY22 cash dividend would be ~7.60 cents per share. Meanwhile, on 2 September 2021, the company announced a cash dividend for Q1FY22 (1 April 2021 to 30 June 2021) of 1.975 cents per share.

Valuation Methodology: Price/Earnings Per Share Multiple Based Relative Valuation (illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using a P/E multiple-based illustrative relative valuation method. The target price so arrived reflects the potential rise of low double-digit (in percentage terms). As a result, the company might trade at a slight premium to its peers’ average, considering an increase in current ratio at 2.58x in FY21 versus 0.83x in FY20 and a decreased debt to equity at 0.38x in FY21 versus 0.47x in FY20.

For the valuation purpose, we have taken peers such as Property for Industry Ltd. (PFI.NZ), Goodman Property Trust. (GMT.NZ), and Vital Healthcare Property Trust. (VHP.NZ) to name a few.

Considering the facts above, we give a “Buy” recommendation on the stock at the closing market price of $1.93 per share as of 14th October 2021.

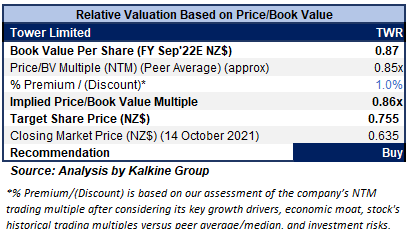

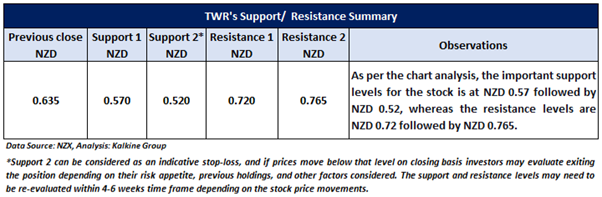

2) Tower Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$267.75 million, Gross Dividend Yield: 3.906%)

Business Description:

Tower Limited (NZX: TWR) is a New Zealand-based insurance company that operates across New Zealand and the Pacific Islands. It is engaged in providing insurance for houses, cars, content, businesses, and more.

Outlook

The company has revised FY21 underlying net profit after tax to be in the range of $19-$21 million from the previous guidance of $22-$24 million, underpinned by increasing house claims cost and falling investment income. Further, it remains in a substantial capital and solvency position and plans to pay a final dividend in line with its policy for the entire year. Large house claims are continuing in FY21, which are above long-term averages, especially during Q3FY21. Ninety-seven large house claims were summing ~$21.3 million in FY21 versus 56 in FY20 to $10.4 million.

Valuation Methodology: Price/Book Value Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using a P/BV multiple based illustrative relative valuation method. The target price so arrived reflects the potential rise of low double-digit (in percentage terms). As a result, the company might trade at a slight premium to its peers’ average, considering business growth and ongoing reduction in management expenses. Also, the technology and distribution strategy continues to deliver growth with the insurer increasing gross written premium (GWP).

For the valuation purpose, we have taken peers such as Harmoney Corp Ltd. (HMY.NZ), AMP Ltd. (AMP.NZ) and Suncorp Group Ltd. (SUN.AX), to name a few.

Considering the facts above, we give a “Buy” recommendation on the stock at the closing market price of $0.635 per share, down 0.78% as of 14th October 2021.

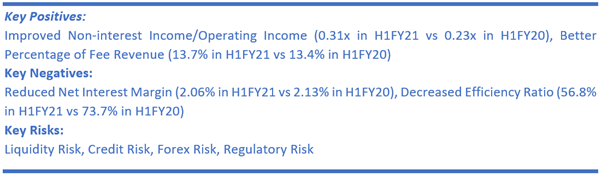

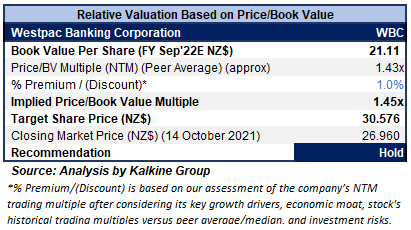

3) Westpac Banking Corporation (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$98.91 billion, Gross Dividend Yield: 3.816%)

Business Description:

Westpac Banking Corporation (NZX: WBC) is one of four major banking organizations in Australia and one of the largest banks in New Zealand. The company offers a spectrum of consumer, business, and institutional banking and wealth management services.

Outlook

As per H2FY21, the company would report a decrease in net profit and cash earnings by $1.3 billion (after-tax), primarily due to a $965 million write-down of assets in Westpac Institutional Bank following their annual impairment test. In addition, it made an additional provision of $172 million, followed by costs relating to Westpac Life Insurance Services Limited of $267 million and other expenses relating to the divestment of its Specialist Businesses of $24 million. Partially, the cost was offset by the gain on sale of Westpac General Insurance of $55 million, followed by a reversal of the earlier write-downs relating to Westpac Pacific as the business is no longer held for sale $54 million.

Valuation Methodology: Price/Book Value Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using a P/BV multiple based illustrative relative valuation method. The target price so arrived reflects the potential rise of low double-digit (in percentage terms). The company might trade at a slight premium to its peers’ average, considering a better net interest margin at 2.06% in H1FY21 versus an industry median of 1.92% and strong fundamentals of the company.

For the valuation purpose, we have taken peers such as Heartland Group Holdings Ltd. (HGH.NZ), National Australia Bank Ltd. (NAB.AX) and Suncorp Group Ltd. (SUN.AX), to name a few.

Considering the facts above, we give a “Hold” recommendation on the stock at the closing market price of $26.96 per share, up 0.71% as of 14th October 2021.

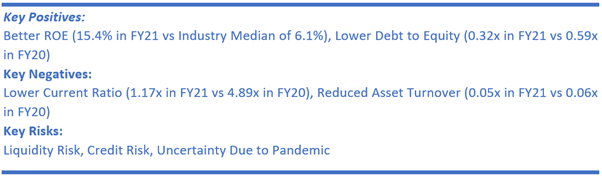

4) Stride Property Ltd & Stride Investment Management Ltd (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$1.15 billion, Gross Dividend Yield: 5.151%)

Business Description:

Stride Property Ltd & Stride Investment Management Ltd (NZX: SPG) consists of Stride Investment Management Limited (SIML) and Stride Property Limited (SPL). SIML is an investment manager and staff employer for the group company, and SPL owns the property portfolio and has an ownership interest in each of the Stride portfolios.

Outlook

On 21 September 2021, the company announced a withdrawal from the current demerger plan and the IPO of Fabric Property Limited. Broadly, the company would continue strengthening its real estate investment management business and continuing a core investment in the office sector. The acquisition of property at 110 Carlton Gore Road, Newmarket, Auckland, is conditional, purely dependent on the success of the IPO before 31 March 2022. As per the management, the company will continue to assess market conditions and evaluate an approach in the interests of both existing Stride shareholders and potential investors.

Valuation Methodology: Price/Earnings Per Share Multiple Based Relative Valuation (illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation:

The stock has been valued using a P/E multiple based illustrative relative valuation method. The target price so arrived reflects the potential rise of low double-digit (in percentage terms). As a result, the company might trade at a slight premium to its peers’ average, considering a higher current ratio at 1.17x in FY21 versus an industry median of 0.74x and a lower debt to equity at 0.32x in FY21 versus an industry median of 0.42x.

For the valuation purpose, we have taken peers such as Property for Industry Ltd. (PFI.NZ), Precinct Properties New Zealand Ltd. (PCT.NZ) and Vital Healthcare Property Trust. (VHP.NZ), to name a few.

Considering the facts above and the current trading level, we give a “Hold” recommendation on the stock at the closing market price of $2.43 per share, down 0.41% as of 14th October 2021.

Note 1: The reference data in this report has been partly sourced from REFINITIV.

Note 2: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the analysis has been achieved and subject to the factors discussed above alongside support levels provided.

Technical Indicators Defined: -

Support: A level where-in the stock prices tend to find support if they are falling, and downtrend may take a pause backed by demand or buying interest.

Resistance: A level where-in the stock prices tend to find resistance when they are rising, and uptrend may take a pause due to profit booking or selling interest.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is authorised to provide general advice only. The information on this website does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...