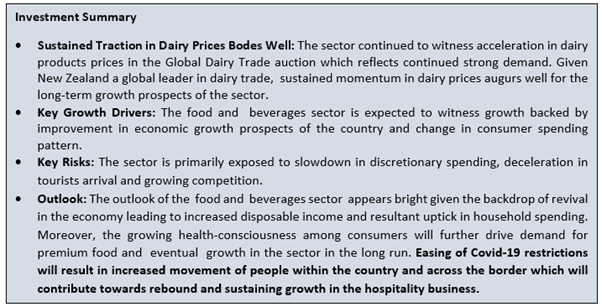

Sector Landscape

New Zealand Food and Beverage sector is one of the prominent drivers of the country’s tourism sector as it caters to the requirements of the rising consumer demand for food and beverage products and services in the country. The growth of this sector is closely linked with the growth in tourism which is one of the mainstays of the economic growth drivers of New Zealand. New Zealand’s food and beverage sector has largely been benefited from the uptick in discretionary spending and mostly improved consumer sentiment over the years. New Zealand enjoys a leadership position in non-alcoholic beverages i.e. the dairy trade globally with improving market share. Globally, New Zealand is the eighth largest milk-producing nation and the country accounts for 3% of global milk production. It is also a leader in the exporting of powders, caseins, butter/dairy fats, and powders, with a strong position in cheese and lactose in the world.

Key Growth Drivers

Some of the key growth drivers of the Foods and beverages sector have been highlighted below:-

Sustained Acceleration in Dairy Products Prices

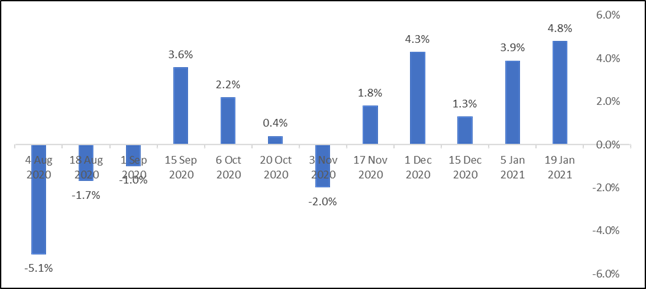

Continued acceleration in dairy products prices in the Global Dairy Trade auction reflects continued strong demand. Given New Zealand is a global leader in the dairy trade, sustained momentum in dairy prices augurs well for the long-term growth prospects of the sector. According to the data from the Global Dairy Trade, the Global Dairy Trade (GDT) index in the latest GDT event on 19 January 2021 witnessed growth of 4.8% as compared to the 3.9% growth in the previous event occurred on 5 January 2021.

The growth was primarily driven by a 17.2% rise in the weighted average price of anhydrous milk fat to USD 5,398/MT followed by a 7% increase in skim milk powder prices to USD3,243/MT. Further, lactose prices witnessed a growth of 6.6% to USD 1,173/MT, while butter prices rose 4.6% to USD 4,735/MT. Whole Milk powder also grew by 2.2% to USD 3,380/MT. However, prices of Cheddar bucked the trend which registered a marginal decline of 0.3% to USD 4,082/MT.

Meanwhile, Fonterra Co-operative Group’s management has updated on 4 December 2020 that it raised the bottom-end of the 2020/21 forecast Farmgate Milk Price range to NZ$6.70 - $7.30 per kgMS from NZ$6.30 - $7.30 per kgMS, while also enhanced the midpoint of the price to $7.00 due to robust demand for New Zealand dairy.

Exhibit 1: Movement in GDT Price Index

Data Source: Global Dairy Trade; Chart Created by Kalkine Group

Revival in Economic Growth

New Zealand food and beverage sector has largely been benefited from the uptick in discretionary spending and mostly improved consumer sentiments over the years. However, in 2020 this particular sector has been hit hard by the adverse impact of the global pandemic which forced the various governments to impose lockdowns in their respective countries to contain the spread of the pandemic.

However, going forward the sector is expected to witness a revival with the improvement in economic growth prospects of the country which managed to contain the spread of the virus at early stage and embarked on fiscal and monetary stimulus of the size about 10% of GDP thereby helping in business and consumer sentiment revived. New Zealand has also been ahead of the rest of the countries in the world in lifting restrictions.

With more than 90% of restrictions lifted, economic activities are rebounding. It has also eased out border restrictions which will help increase tourists visiting the country. These developments will lead to increased individual income and thereby revival in consumer discretionary spending. This will further strengthen the country’s GDP.

The latest GDP number marked the strongest quarterly growth on record in New Zealand. This showed signs of resilience and suggested a rebound in the economy. Driven by the benefit of easing of restrictions on activities, New Zealand’s GDP has witnessed a sharp rebound of 14% in the September 2020 quarter as against a revised 11% decline in GDP in June 2020 quarter, as demonstrated in Exhibit 2 below.

Exhibit 2: GDP Movements in Major Economies

.png)

Data Source: Stats NZ; Chart Created by Kalkine Group

Uptick in Consumer Spending

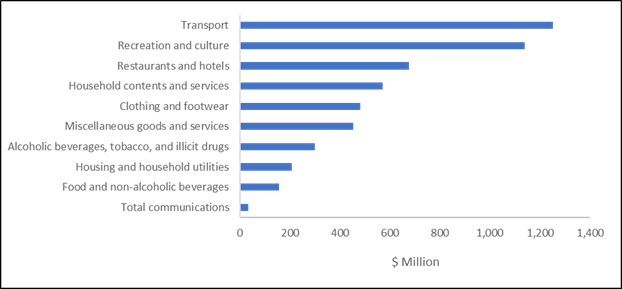

The recent data pertaining to the value of electronic card transactions for December 2020 showed signs of improvement in spending on liquor as well as on food and services which registered a growth of 16% YoY and 1.8% YoY, respectively. Moreover, the household spending in the September 2020 quarter also showed signs of improvement with the country’s household spending soaring by 14.8% as a result of a significant acceleration in spending seen in restaurants and ready-to-eat meals as is reflected in Exhibit 3 below.

Thus, revival in consumer spending lends visibility on the uplift in consumer demand and growth prospects of the sector, going forward.

Exhibit 3: Change in Household Consumption Expenditure from June 2020 to September 2020 Quarter

Data Source: Stats NZ; Chart Created by Kalkine Group

Key Risks and Challenges

Below are some of the risks and challenges the broader sector is exposed to:

The Slowdown in Discretionary Spend

Household spending as well as discretionary spending are key drivers of growth of the country’s food and beverage sector. The global pandemic has created an environment of restricted discretionary spend by households as well consumers which had a negative bearing on the sector’s performance. Any further delay in pandemic dissipation will weigh on the long-term growth prospects of the sector.

A Deceleration in Tourists Arrival

The influx of international tourists also plays a crucial role in the development of the sector as a whole. However, the slowdown in the global economies, as well as restrictions on international tourist arrivals had cast a dark shadow on the growth prospects of the sector. Meanwhile, the easing of travel restrictions and the gradual opening of international borders offers a positive outlook for the sector as this move will boost the flow of international tourists into the country which will eventually be aiding the overall sector to grow at a faster pace.

Growing Competition

In the global pandemic environment, the increasing competition has dealt another blow to the visibility of the sector, resulting in a price war in an increased cost environment. However, the impact of the same can partially be mitigated by the strengthening of delivery service and focus on innovation and delivering quality of services in order to attract customers’ confidence. The easing of Covid-19-related restrictions will drive consumer spending behaviour and will eventually lead to the strengthening of demand and will ultimately boost growth of the sector.

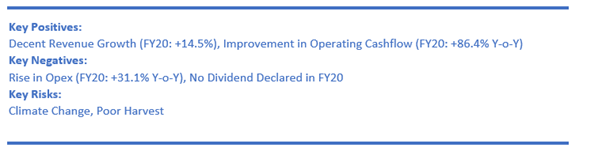

Exhibit 4: Key Risks and Challenges

.png)

Source: Kalkine Group

Outlook

Given the gradual uptick in New Zealand’s economic activities on the back of easing of the Covid-19 related restrictions, there has been an improvement in consumer demand in the September 2020 quarter. This is clearly reflected from the rise in the real gross national disposable income of the country (RGNDI), which measures the real purchasing power of the country’s disposable income which posted a growth of 13.9% in the September 2020 quarter. Thus, it will assist in driving discretionary spending as well as household spending as higher income will lead to enhanced purchasing power to spend on dining out on restaurants and beverages sold by cafes and restaurants. This will ultimately boost the demand for consumer-orientated products and sector, particularly for the food and beverage sector.

Moreover, the growing health-consciousness among consumers will further drive demand for premium food products and will eventually augur well for the sector in the long run. The receding level of the COVID-19 restrictions in the country will result in regaining demand from arriving international tourists which further strengthens visibility on the long-term growth prospects of the sector.

Apart from the sector-specific factors, we have also analysed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

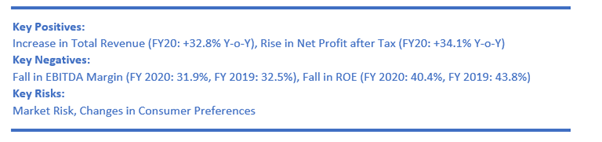

1. Comvita Ltd (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$219.586 million)

Business Description:

Comvita Ltd (NZX: CVT) is currently one of the leading players globally of the Mānuka honey category.

Outlook

In a bid to boost organisational resilience and fortify its balance sheet strength, CVT wrapped up raising of capital worth $50 million (gross capital) in June 2020. The company is having a stronger financial position which could help it in achieving long-term growth objectives.

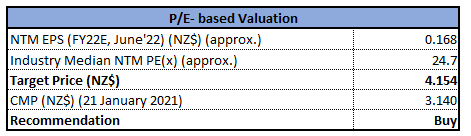

Valuation Methodology: P/E Based Relative Valuation (Illustrative)

P/E Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

We have applied P/E multiple Based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms).

Considering the expected upside and decent revenue growth, we give a “Buy” rating on the stock at the current price of NZ$3.140 per share, down by 0.63% on January 21, 2021.

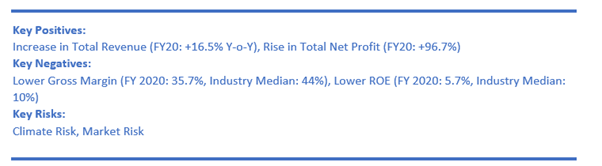

2. The a2 Milk Company Ltd (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$8.1 billion)

Business Description:

The a2 Milk Company Ltd (NZX: ATM) happens to be a premium branded dairy nutritional company which has a market capitalisation of ~$8.1 billion as on January 21, 2021.

Outlook

The company continues to focus on strengthening its supply chain strategy. The company is assessing opportunities to participate in manufacturing nutritional products that complements its existing supply arrangements to create supplier as well as geographic diversification.

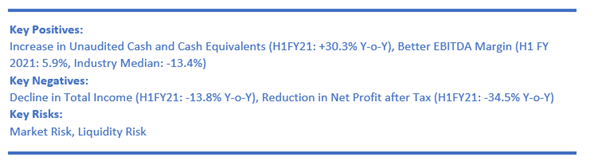

The company is expecting Group revenue for H1 FY 2021 in the order of $670 million, noting that Q2 FY 2021 will be higher than Q1 FY 2021 and group EBITDA margin for H1 FY 2021 in the order of 27%. For FY 2021, group revenue is expected to be in the range of $1.40 billion- $1.55 billion and group EBITDA margin for FY 2021 is expected to be between 26%- 29%.

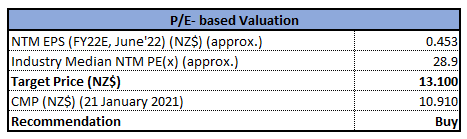

Valuation Methodology: P/E Based Relative Valuation (Illustrative)

P/E Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

We have applied P/E multiple Based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms).

Considering the expected upside and rise in net profit after tax, we give a “Buy” rating on the stock at the current price of NZ$10.910 per share, down by 0.91% on January 21, 2021.

3. Foley Wines Ltd (Recommendation: Hold, Potential Upside: Mid-Single-Digit) (M-Cap: NZ$126.871 million, Gross Dividend Yield: 2.115%)

Business Description:

Foley Wines Ltd (NZX: FWL) is engaged in the wineries business and is a collection of iconic wineries and brands from New Zealand’s most acclaimed wine regions.

Outlook

FWL has set a target of achieving 600,000 cases in 2021. The company added that EBITDA margin improvement is the key focus for the company and a fundamental strategy to improve this is via premiumisation. Notably, markets are extremely volatile, particularly for the brands which have high hospitality focus.

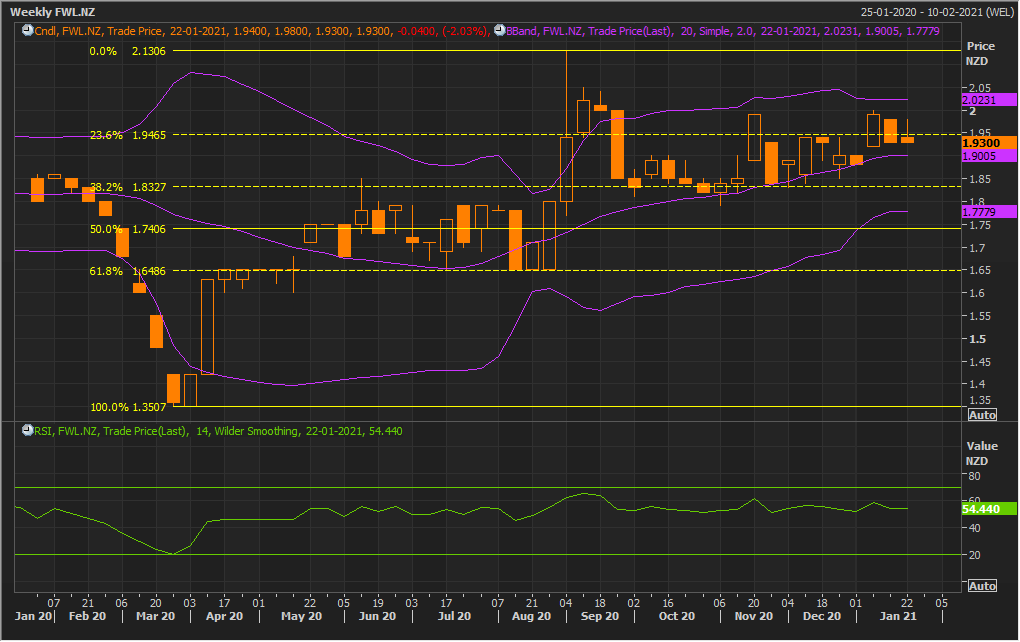

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack. https://www.bollingerbands.com/

The stock made the high of $2.13 and from there it took correction to the extent of the 38.2% retracement level of $1.83, and again moved up beyond 23.6% retracement level of $1.95. It has, however, given a flattish close at $1.93 for the ongoing week. The technical indicator RSI with a reading around 54 and a flattish curve at the end, suggests flattening of bullish momentum for the stock.

Going forward, the stock may have resistance around the upper Bollinger band of $2.023 whereas support could be around 20 periods SMA of $1.900 where a gap on the chart exists.

Considering the technical analysis and increase in total revenue, we give a “Hold” rating on the stock at the current price of NZ$1.930 per share, down by 2.03% on January 21, 2021.

4. Burger Fuel Group Ltd (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$20.890 million)

Burger Fuel Group is having experience in the restaurant sector which stretches over the time span of 20 years. It operates 3 brands, namely: BurgerFuel, Shake Out and Winner Winner.

Outlook

The Group has no debt as at 30 September 2020 and had cash reserves of $6.8 million at the end of 30 September 2020. Considering the fact that the company has no debt, there are expectations that it could focus towards achieving long-term growth objectives. BFG happens to be in a decent position as its finances, talent, intellectual property as well as future opportunities are well in place. Moreover, the cautious opening of new locations in New Zealand is well within the capabilities as well as financial position. However, franchise opportunities are limited.

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack.

While remaining in a major downtrend, the stock has given a stronger close, forming a ‘Hammer’ on the chart for the ongoing week. Forming of a hammer in a downtrend or bearish consolidation, suggests a bullish reversal for the stock. The technical indicator RSI with a reading around 51 and a curve at the end pointing up, indicates bullish momentum for the stock.

Going forward, the stock may have resistance around the 38.2% retracement level of $0.470 whereas support could be around the 61.8% retracement level of $0.383.

Considering the technical analysis and better EBITDA margin, we give a “Hold” rating on the stock at the current price of NZ$0.415 per share, up by 3.75% on January 21, 2021.

Comparative Price Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...