Investment Summary:

The hospitality industry is a comprehensive industry that covers restaurants, hotels, flights, and entertainment. Because of the extent of businesses in this industry, it is an enormous revenue maker for many developed countries.

NZ is a young country, which is still realizing its competitive advantages as new industries continue to develop. In the past 20 years, New Zealand wine, honey, aquaculture, and avocados have all developed from almost nothing into world-leading sectors.

Marginal Decrease In Wine Volumes

In 2019, the total volume of wine available for consumption dropped a little by 0.7 percent to 108 million litres. This follows a decline of 1.4% in 2018 and an increase of 1.5% in 2017.

Of the main categories of wine:

Card Spending Declines Due to Extended Lockdown

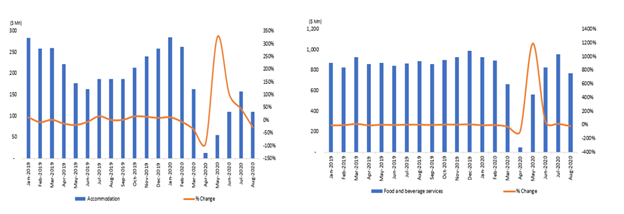

As per Stats NZ, the card spending in hospitality sector declined in August 2020. Spending on both accommodation away from home and eating out declined in August due to 19 days of COVID-19 alert level 3 restrictions in Auckland and alert level 2 restrictions for the rest of New Zealand.

In actual terms, spending on food and beverage services, which includes businesses like cafes, restaurants, takeaway food, and bars, decreased 13 per cent or $115 million Y-o-Y. This follows an 11 percent or $92 million increase in July 2020 Y-o-Y.

Spending on businesses like motels, hotels, and other accommodation decreased 41 percent or $77 million Y-o-Y. This follows a 16 percent or $30 million fall in July 2020 Y-o-Y.

Key Data (Source: Stats NZ)

A Look At New Zealand’s Alcohol Industry

The sale and production of alcohol is a multi-billion-dollar industry in New Zealand. The major players in this industry can be classified into four groups:

The Beer Industry

The Beer Industry is dominated by Lion and DB Breweries and is consumed by young adult males. Although beer became available in supermarkets in 1999, there has been a downward trend in the volume of beer sold in New Zealand, from 322.5 million litres in 2008 to 279.9 million litres in 2012. Since then, there appeared to have an increasing trend in the volume of beer available for consumption. In 2019, there were 297.8 million litres of beer available for consumption.

Outlook

The country’s economic plan envisions a more productive, sustainable, and inclusive economy with strong investment in the food and beverage value chain. The country has a significant untapped capacity to export more and triple its food and beverage exports over the next 15 years. It has attracted investment in food and beverage manufacturing from around the world due to its world-class innovation and production.

The country exports food and beverages to many destinations of which Asia is the largest. Within Asia, China, in particular, is driving exports from New Zealand. With the objective of controlling the spread of the Corona Virus, many countries enforced nationwide lockdowns. However, the Food and beverage industry continues to operate as it has been categorized to be in essential services.

Emerging Growth Opportunities

New Zealand has a long history of producing and exporting food and beverage products with a clear competitive advantage. The food and beverage industry has attracted a wide range of funds including regional and global funds. They are attracted to high growth in the industry. The country continues to be an attractive investment destination for global food and beverage multinationals. Private Equity and Venture Capital investors are attracted to high growth, on-trend segments. An incredible range of multinational food companies are currently invested in New Zealand food and beverages.

New Zealand has a stable democracy with economic freedom, excellent investor protection and low corruption. Thus, by all measures, it is the most attractive investment destination.

Hospitality Businesses Facing Liquidity Issues

As per Stats NZ, many hospitality businesses in New Zealand did not have a substantial amount of assets in their hand to meet short-term liabilities due to trading restrictions caused by COVID-19. As per annual enterprise survey:

Key Data (Source: Stats NZ)

Challenges Faced By Sector

The key risk facing the sector is the change in consumer preference and growth in consumer expectations. Of late, there has been a rise in demand for organic and healthy food traded ethically by millennials and more conscious consumers. Consumers are leaning more towards healthy products as they are becoming more health conscious. The sector is more vulnerable to disruption from consumers becoming more prominent than that of competition from companies within the sector.

Since we now have a broad idea of food and beverage sector, it is important to look at the performance of some companies operating in the same sector (DGL, FWL, MWE, CGF).

1. Delegat Group Limited (NZX: DGL) (Recommendation: Hold, Potential Upside: Higher Single-Digit), (M-Cap: ~NZ$1.46 Billion, Dividend Yield: 1.63%)

Business Description: Delegat Group Limited is one of the most successful and largest wine companies in Australasia, appreciated both globally and within New Zealand for its significant and positive contribution to the wine industry.

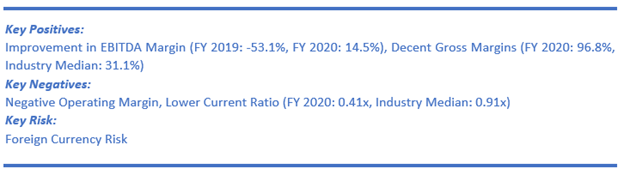

Outlook: The global economy is still uncertain, however, considering the company’s FY20 results, the company seems to be well-positioned to navigate through these uncertain times. The company continues to witness opportunities worldwide to further increase distribution and grow rate of sale per point of distribution. The company is expecting to increase sales by 17% to 3,840,000 cases over the next three years and for FY21, the company is expecting to grow sales by 2% to 3,346,000 cases. Operating profit is expected to be in the range of $60 million to $65 million for FY21.

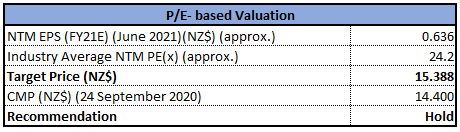

Valuation Methodology: P/E Based Relative Valuation (Illustrative)

P/E Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Thus, we give a “Hold” rating on the stock at the price of NZ$14.400 per share, down by 0.69% on September 24, 2020.

2. Foley Wines Limited (NZX: FWL) (Recommendation: Buy, Potential Upside: Lower Double-Digit), (M-Cap: ~NZ$121.61 Million, Dividend Yield: 2.15%)

Business Description: Foley Wines Limited is a collection of iconic wineries and brands from New Zealand’s most acclaimed wine regions.

Outlook: Over the past couple of years, the company has proven that it is achieving momentum with its premiumisation strategy. The company has laid a strong foundation for growth to take advantage of opportunities as they arise and will continue to focus on brand building and developing new routes to market at the premium price points.

Valuation: On TTM basis, its P/BV multiple stood at 1.0x as compared to industry median (Beverages) of 2.8x. Its EV/Sales multiple stood at 3.3x while industry average is 15.1x.

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack.

The stock witnessed a sharp rise in September, making all-time high of $2.13. However, for the past two weeks, the stock seems to have come under selling pressure. The stock for the ongoing week has given close at its low price of $1.85. Yet, uptrend for the stock is intact as it is yet to fall below 20 periods SMA of $1.77. The technical indicator RSI with a reading around 54 with a curve at the end pointing down, suggests the softening of strong bullish momentum for the stock.

Going forward, the stock may have resistance around $2.05 whereas strong support could be around 20 periods SMA of $1.77.

Thus, we give a “Buy” rating on the stock at the price of NZ$1.850 per share, down by 4.64% on September 24, 2020.

3. Marlborough Wine Estates Group Limited (NZX: MWE) (Recommendation: Speculative Buy, Potential Upside: Lower Double-Digit), (M-Cap: ~NZ$52.789 Million)

Business Description: Marlborough Wine Estates Group Limited produces some of NZ’s finest Awatere Valley (Marlborough) Sauvignon Blancs.

Outlook: The company has established its position in the country’s market and set up strong grounds for future growth in the international markets. It is looking forward to many thriving years ahead and will remain focused towards long term growth in revenue, profitability, and brand recognition in both domestic and international markets.

Valuation: On TTM basis, the company’s EV/Sales multiple stood at 9.7x as compared to industry average (Beverages) of 15.1x. Its P/BV multiple stood at 3.9x while industry average is 28.1x.

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack.

Having witnessed a sharp fall in the previous week, the ongoing week is proving to be strong with the stock giving close at the peak price of $0.181 demonstrating strength in bullish sentiment on the stock. The technical indicator RSI with around 41 reading and curve at the end pointing up, suggests gaining of the bullish momentum for the stock.

Going forward, the stock might have resistance around the converging point of 50% retracement level and the upper Bollinger band $0.191 whereas support could be around $0.175.

Thus, we give a “Speculative Buy” rating on the stock at the price of NZ$0.181 per share, up by 3.43% on September 24, 2020.

4. Cooks Global Foods Limited (NZX: CGF) (Recommendation: Hold, Potential Upside: Higher Single-Digit), (M-Cap: ~NZ$30.14 Million)

Business Description: Cooks Global Foods Limited owns the intellectual property and master franchising rights to Esquires Coffee Houses worldwide (excluding New Zealand and Australia).

Outlook: As per the release dated March 18, 2020, the company has been closely monitoring the effect of the COVID-19 outbreak, mainly on its Esquires café operations in Ireland and the United Kingdom, which are the two largest business units in revenue terms. In the United Kingdom, the company’s 40 franchised & 4 company operated stores remain open.

Technical Overview:

Weekly Chart–

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack.

The stock has given stronger close at $0.048 for the ongoing week having covered the loss it incurred during the previous week. The technical indicator RSI with around 43 reading and curve at the end pointing up, suggests gaining of the bullish momentum for the stock.

Going forward, the stock may have resistance around $0.0522 whereas support could be around $0.0438

Thus, we give a “Hold” rating on the stock at the price of NZ$0.048 per share, down by 2.04% on September 24, 2020.

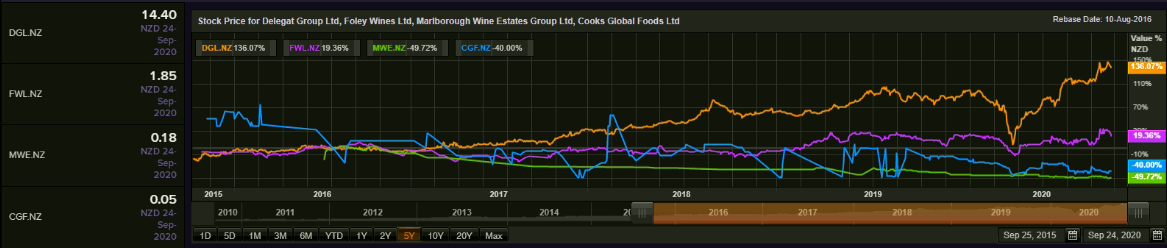

Comparative Price Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...