New Zealand’s financial system is characterized by stability and a robust institutional framework. Strong regulatory framework of the banks and financial companies coupled with the resilient securities market and robust insurance sector help in channelling savings into investments, thereby bolstering economic growth in New Zealand. According to Financial Services Council, the contribution of financial services industry to NZ economy is significant and is evolving with the help of innovation and technology. NZ banking sector is robust and is primarily characterized by continuous developments in the field of technology and digitization.

According to the New Zealand Bankers Association (or NZBA):

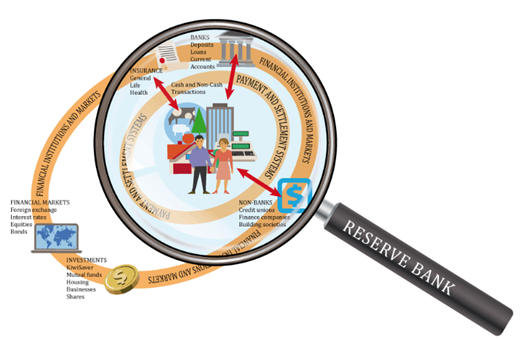

FIG.:1. Financial System in New Zealand (Source: Reserve Bank of New Zealand)

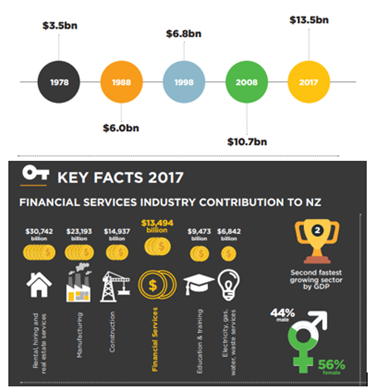

According to New Zealand Institute of Economic Research (or NZIER), financial services sector helps the wider New Zealand economy and plays a critical part in supporting all the industries in New Zealand. The sector happens to be the second fastest-growing and third largest contributor to broader economic growth. It made the contribution of $13.5 billion to GDP in 2017, which was well-ahead of agriculture which contributed $12.9 billion, transport ($10.6 billion) and utilities ($6.8 billion).

Developments in NZ’s Financial System Further Strengthens Fundamentals

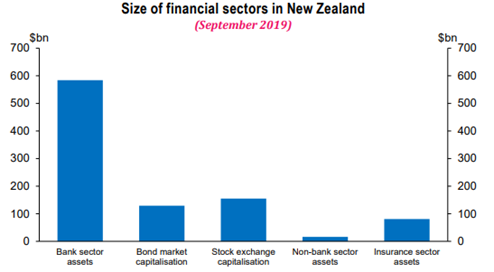

The financial system in New Zealand underpins health of the broader economy. A properly functioning financial system allows for the efficient distribution of risks making it more resilient to the downturns. According to Reserve Bank of New Zealand’s financial stability report (November 2019):

FIG.:2. Size of Financial Sectors (Source: Reserve Bank of New Zealand)

Growing Importance of Financial Services Provides Solid Base for Future Growth

According to the Financial Services Council, the contribution of financial services industry to NZ’s economy, or GDP, quadrupled between 1978 and 2017, growing substantially from NZ$3.5 billion to NZ$13.5 billion. Overall percentage contribution from the industry rose to 6% of the country’s GDP. This is ahead of utility, education, and transport industries.

Unlike most other industries, financial services sector plays a critical role in supporting the production of other NZ industries which contribute to the broader economy. The sector supports the industries in making deployments towards growth objectives which can add to the growth of resilient NZ economy.

FIG.:3. Key Numbers (Source: Financial Services Council)

How Resilient is Insurance Industry in New Zealand?

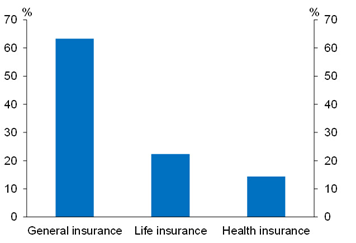

There are approximately 90 licensed insurers that are operating in New Zealand, making up for around $30 billion in assets, or 12% of GDP. On the basis of premium revenue earned in quarter ended June 2019, general insurance makes up 61% of the reported large private insurer business in NZ. However, life insurance and health insurance represent approximately 23% and 15%, respectively.

According to Financial Services Council, in 2017, the life insurance industry in NZ managed NZ$9.3 billion of assets throughout 12 providers and NZ$2.5 billion of received in-force premiums. Since NZ has high exposure to natural hazard risk, general insurance penetration is high as compared to other countries/regions with same levels of natural hazard risk. The market is dependent on offshore foreign capital, in the form of reinsurance, in order to help existing coverage levels.

FIG.:4. Insurance Policy and Premium Revenue Earned by Sub-sector (June Quarter 2019) (Source: Reserve Bank of New Zealand)

Technology Continues to Revamp Financial Sector in New Zealand

The financial services industry strives to provide a range of advice and support to the people in New Zealand.

Range of technological tools might help the broader financial sector in simplifying the distribution and investment processes. With higher offshore investments, the sector’s fundamentals might strengthen further, thereby contributing to the overall economic development of New Zealand.

Financial Sector Set to Drive Economic Growth: A Look at Key Demand Drivers

Given the backdrop that majority of lending to the private sector happens via banking system, it plays a dominant role in promoting economic growth with stability. The banking role has become all the more important as the economy is passing through global economic shock caused by COVID-19.

Governments across the world are raising debt to pay for increased spending and support for their economies. Developed countries are raising debt despite having an average net debt position above 70% of GDP with the UK about 75%, the US above 80%, Italy above 120%, and Ireland above 50% of GDP. Fortunately, New Zealand has a sound financial position with net debt below 19.2% of GDP, enabling it to go early in the fight against COVID-19. The international credit rating agency has re-affirmed its highest Aaa credit rating on New Zealand, saying that the economy is expected to remain resilient.

Financial System Robust Enough to Counter Risks

Even though the financial system in New Zealand is well-placed to weather out the economic impacts of the pandemic, it is exposed to risks of being stressed by failing business and loan default. COVID-19 might give rise to credit impairment as viability of businesses in many sectors are under question. The situation can further deteriorate with prolonged downtrend in economic activities as loss of income will cause financial distress for a number of households and businesses. Housing and agriculture sector are more prone to risks of downturn in economy.

Prolonged economic slump will put downward pressure on rents and lead to rise in empty commercial and residential property. Similarly, agriculture is also vulnerable to slowdown in economy, posing risks to the banking sector. Agriculture accounts for around 13% of bank lending of which around two thirds is to dairy sector. Notably, expected growth in dairy sector might help the broader banking sector in countering risks. According to Ministry of Primary Industries (or MPI), dairy export revenue has been forecasted to increase 6.3% to $19.2 billion for the year ending June 2020, on the back of robust domestic production and favourable export prices.

Even though, there exists considerable uncertainty about economic outlook, stress tests conducted for banks in New Zealand suggest that banks will be able to withstand adverse scenario.

After having a view of the financial sector in New Zealand, we will now look at the companies operating in the sector (GFL, ANZ, NZX, BIT).

1. Geneva Finance Limited (NZX: GFL) (Recommendation: Buy, Potential Upside: Lower Double-Digit) (M-Cap: ~NZ$32.09 million, Gross Dividend Yield: 7.955%)

Business Description: Geneva Finance Limited (NZX: GFL) is a New Zealand owned finance company which offers finance and financial services to the consumer credit and small to medium enterprise markets.

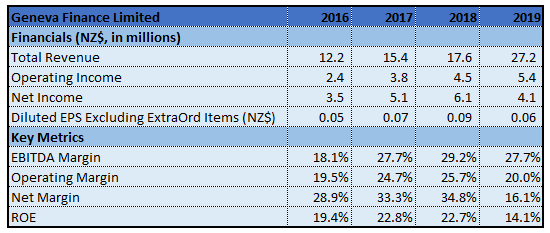

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The key focus of the company continues to be on the implementation and development of the lending and sale platforms of the trading businesses, comprising the company’s IT infrastructure, the new invoice factoring system, Quest’s in-house claim management system and Stellar’s debt collection software. Also, the company remains in a strong position to develop on the core infrastructures that it has in place in the four trading businesses. The changes that have been made were necessary for the long-term benefit of the group and focus remains on continuing to deliver the profit growth.

Going forward, the stock may have resistance around $0.50 as has been provided by 50% retracement level while on price retracing further, it may have support around $0.41 as has been provided by 23.6% retracement level.

2. Australia and New Zealand Banking Group Limited (NZX: ANZ) (Recommendation: Buy, Potential Upside: Lower Double Digit) (M-Cap: ~NZ$56.15 billion, Gross Dividend Yield: 4.857%)

Business Description: Australia and New Zealand Banking Group Limited (NZX: ANZ) provides banking and financial products and services to individual and business customers and operate in and across 33 markets.

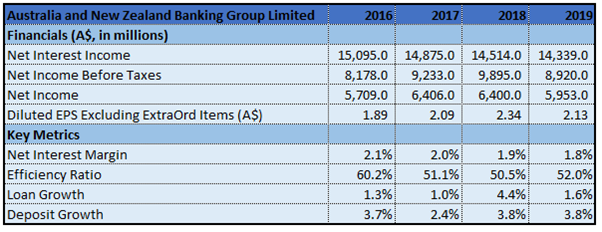

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The bank has decided not to give any interim dividends for FY20 until there is greater clarity regarding the economic impact of COVID-19. With regards to capital, the bank started in a position of strength with CET1 ratio at 10.8%, even after bolstering reserves to record levels. In the short-term, the bank is tightly managing its costs, while providing as much job security as it can for people. The bank has decided to freeze the salary for at least 12 months.

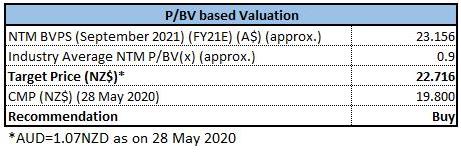

Valuation: The bank’s priorities mainly revolve around 1) Focusing on liquidity, 2) Operational agility, 3) Continued focus on productivity, and 4) Making investment for the long-term. We have applied P/BV based relative valuation (on an illustrative basis) and the target price reflects a growth of lower double-digit (in % terms).

3. NZX Limited (NZX: NZX) (Recommendation: Buy, Potential Upside: Lower Double-Digit) (M-Cap: ~NZ$38832 Million, Gross Dividend Yield: 5.966%)

Business Description: NZX Limited operates New Zealand’s equity, debt, derivatives, and energy markets. It also provides clearing, trading, depository, settlement, and data services.

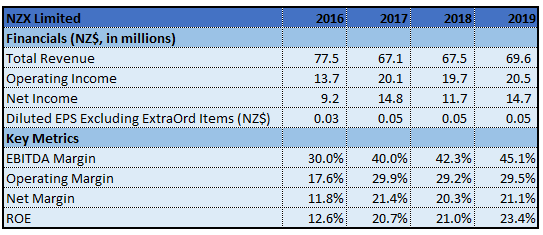

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The company was classified as an essential service to New Zealand and has remained fully operational. Delivery of a broad platform of growth in FY19 has provided a strong base for FY20 operating earnings guidance, which is expected to be in the range of $30.0 million to $33.5 million. The company has widened the guidance at the lower end of the range, reflecting the current uncertain global environment.

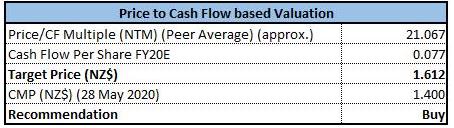

P/CF Based Relative Valuation (Source: Refinitiv (Thomson Reuters)) (Illustrative)

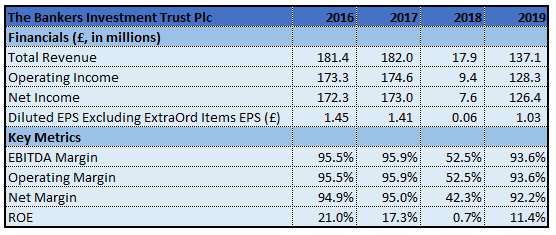

Business Description: The Bankers Investment Trust Plc (NZX: BIT) targets capital growth in excess of the FTSE World Index and income growth greater than UK inflation rate, by investing in companies listed across the world.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Going forward, the stock may have resistance around its recent high of $21.06 while support could be around $18.41 as has been provided by 61.8% retracement level.

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...