I. Sector Landscape and Outlook

The New Zealand government launched its digital technologies industry transformation plan in 2019, however revised its plan in June 2020 in response to the impact of COVID-19. The tech plan is required because digital technologies will be crucial for forthcoming economic and social development and will drive future growth. For this purpose, this sector was added to the initial set of ITPs. Moreover, technology is both a high value, and an internationally oriented sector and a key enabler for efficiency enhancement for other sectors. Growing the sector will add value to a productive, sustainable, inclusive, and resilient economy.

The Rise in Internet Usage Led by Addition of New Users and New Usage

As per the Commerce Commission New Zealand, for the year ended 30 June 2020, the broadband usage increased 37% YoY on the back of strong usage during Covid-19 lockdown, and more people taking unlimited usage plans. However, text messages sent decreased 13% and landline connections were down 12%, followed by a fall in copper connections by 24% as more households shifted to fibre networks. However, by June 2023, 87% of households should be able to connect to fibre.

Exhibit 1: Telecommunication Trend in 2020

Data Source: comcom.govt.nz, Chart Created by Kalkine Group

Overall Progress in Ultra-Fast Broadband and Fibre

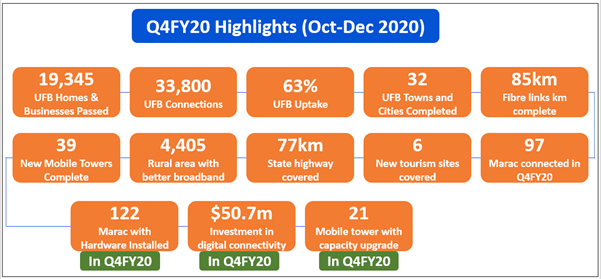

As per the report released by the Ministry of Business, Innovation & Employment, over 1,079,643 households and businesses gained access to UFB in the three months from October to December 2020. UFB program is the urban broadband plan deploying fibre-to-the-premises to 87% of the population by 2022, covering 411 towns and cities in New Zealand. On completion of the scheme in 2022, there will be over 1.8 million homes and businesses accessing UFB. Importantly, as per the government’s overall plan, ~99.8% of New Zealand population will be able to access improved broadband by the end of 2023.

The Rural Broadband Initiative programme (RBI2) and Mobile black spot fund (MBSF) targets: (a) 872 eligible Marae, who can connect to broadband on request, (b) 84,000 rural homes and businesses will receive improved broadband by the end of 2023 (c) ~1,400 km of State Highway and over 168 tourism sites will receive mobile coverage, (d) 372km fibre links kms, and (e) 70 mobile tower capacity upgrades.

Exhibit 2: Q4FY20 Connectivity Update – Expanding its Reach in Rural & Urban Areas

Data Source: mbie.govt.nz, Chart Created by Kalkine Group

Rural Broadband Funding

The Minister for Broadcasting, Communications, and Digital Media has announced an additional $50 million fund for rural broadband digital connectivity from the $3 billion infrastructure fund announced in the COVID Response and Recovery. The fund is expected to boost broadband access and capacity across New Zealand. Importantly, this funding is complementary to the $15 million announced on 29th April 2020 to support rural network capacity, aiming to provide quality broadband with reliability and consistency, especially during peak hours.

Fixed Broadband Market Share

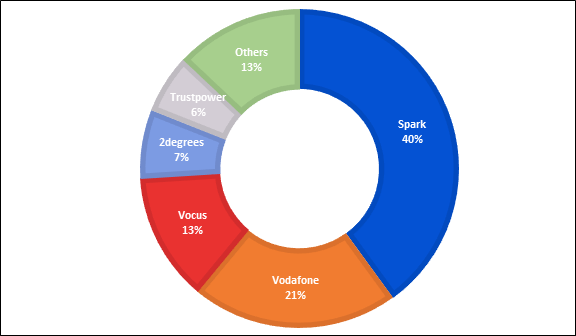

As per the estimates by the Commerce Commission report, the biggest retailer of fixed-line broadband by the number of connections is Spark with a 40% market share in 2020, including its sub-brand Skinny. Meanwhile, other smaller retailers continue to expand their market share to 13% in 2020 from 11% in 2019. In addition, 2degrees surpassed Trustpower to become the fourth biggest provider with a 7% market share in 2020. Vodafone’s market share also decreased, from 24% in 2019 to 21% in 2020. However, Vocus retained its position with market share at 13% in 2020.

Exhibit 3: Fixed Broadband Retailer Market Share by Connections

Data Source: comcom.govt.nz, Chart Created by Kalkine Group

New Zealand Technology Companies Attracting Fresh Investments and Contributing to Export

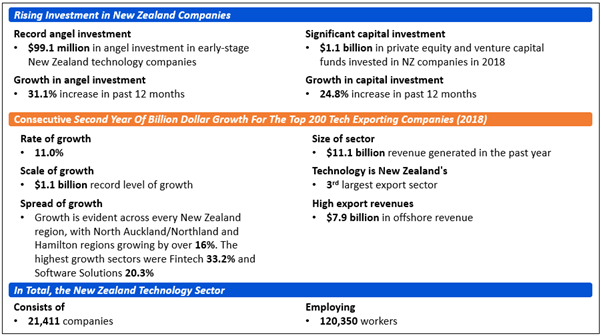

As per the Ministry of Business, Innovation, and Employment, the New Zealand technology export sector increased by over one billion dollars in 2018, making tech the country’s third-largest export sector. Primarily, New Zealand's technology sector is distinct & innovative and competes effectively on the world stage. The industry is a rising business for New Zealand, accounting for 8% of GDP and employing 5% of the workforce.

Exhibit 4: Increasing Investments in New Zealand Technology Companies

Data Source: mbie.govt.nz, Chart Created by Kalkine Group

Index Performance:

The S&P/NZX All Information Technology (Industry Group) Index generated a 1-year return of ~23.33% as compared to ~15.29% by the S&P/NZX 50 Index.NZX All Information Technology (Industry Group) overperformed NZX50 Index by ~8.04% in one year period.

Exhibit 5: S&P/NZX All Information Technology (Sector) vs S&P/NZX50 Index

Source: Refinitiv (Thomson Reuters)

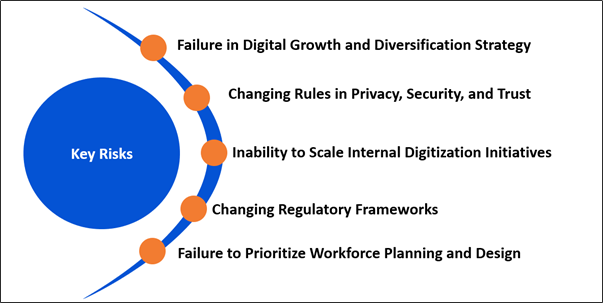

Key Risks and Challenges:

The sector is exposed to various key risks due to the increasing usage of developed technologies and applications such as an Internet-of-Things (IoT), which is leading to the risk of cybersecurity. Therefore, it has created the need for resilience and the importance of data protection.

Further, access to telecommunication services to the rural communities of the country proved to be a challenge, and with the sector dominated by private capital, it not economically viable to provide affordable infrastructure. The long-term solution to this problem is not clear, although it has been addressed through Crown-Private cooperation and infrastructure sharing.

Exhibit 6: Key Risks in the Communication Services and Technology Sector:

Sources: Analysis by Kalkine Group

Outlook:

The telecom sector is the support line of all businesses and individuals. There has been a robust demand for the telecommunication sector’s products and services since the Covid-19 pandemic started. Therefore, the telecommunication sector is expected to report a major growth spurt in 2021. Meanwhile, in 2020, New Zealand ranked 12th in the OECD, with average fixed broadband download speeds of nearly 67Mbps.

Meanwhile, the Telecommunications infrastructure sector is going through a transformational period with the national rollout of fibre broadband. Post the completion of the transformational phase, it is expected that 87% of the country’s population will have access to fibre by end of 2022. This will aid New Zealand in becoming one of the leading countries in the OECD in fibre availability.

On the technological front, cloud computing, Maori-Tech, and artificial intelligence are expected to expand further to dominate the technology industry. Artificial Intelligence is being significantly used around the world by governments, businesses, and individuals to drive digital innovation across industries in New Zealand’s future economy. Further, associating with Māori-Tech is a key principle guiding Government’s Industry Strategy to ensure that the ITP delivers step-change improvement for the Māori economy and facilitates Māori aspirations in the digital technologies sector.

Apart from the sector-specific factors, we have also analysed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance, and potential as expected to be delivered in the near to medium term.

1) Telstra Corporation Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$43.89 billion, Gross Dividend Yield: 4.746%)

Business Description:

Telstra Corporation Limited (NZX: TLS) is engaged in the telecommunications and information services business, offering the full range of communications services as well as competing in all the telecommunications markets.

Outlook:

The management is seeing a turning point in the mobile ARPU numbers in H1FY21 that are expected to grow in H2FY21. Further, the mobile business is building positive momentum with strong 5G leadership and differentiation, a higher proportion of customers taking plans of $65 or higher, digital engagement is growing, two-thirds of mass-market post-paid customers have taken in-market plans, and loyalty program continues to accelerate. These factors indicate that mobile EBITDA will increase again sequentially in 2H21. In addition, the management is also expecting growth in FY21 on a PCP basis.

Valuation Methodology: Price/Cash Flow Based Relative Valuation (Illustrative)

.png)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation

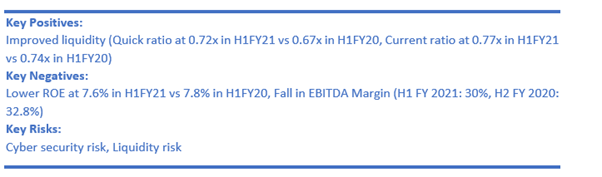

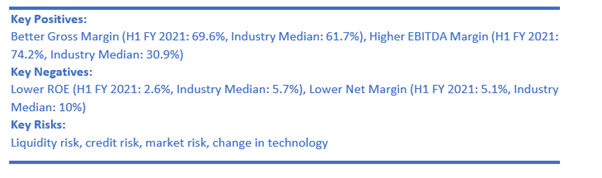

We have applied Price/Cash Flow (P/CF) based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied a slight discount to P/CF Multiple (NTM) (Peer Average) because of decline in EBITDA Margin in H1 FY 2021 as compared to H2 FY 2020 and lower ROE.

For the purposes, we have taken peers such as Spark New Zealand Ltd (SPK.NZ), Chorus Ltd (CNU.NZ), and Vocus Group Ltd (VOC.AX) to name a few.

Considering the aforesaid facts, we give a “Hold” recommendation on the stock at the current market price of $3.69 per share, up 1.10% on 20th May 2021.

2) Spark New Zealand Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$8.40 billion, Gross Dividend Yield: 7.847%)

Business Description:

Spark New Zealand Limited (NZX: SPK) is a telecommunications and digital services company. Spark New Zealand is made up of several core business areas, Spark Home, Mobile & Business, Spark Digital, Spark Ventures, as well as Spark Connect.

Outlook

The management has shifted its focus on delivering user-friendly and more intuitive customer experiences that have seen welcoming responses in recent times. With the launch of Spark App, an additional 18% of customer care interactions is being self-solved digitally, which is also retiring over 100 legacy plans. Further, the demand for business transformation and digitization continued further, supported by the acceptance of fresh ways of working due to COVID-19 lockdowns. Meanwhile, the company is making sound development in the Internet of Things (IoT), where the connections are growing by 65% during H1FY21.

However, the company has narrowed the FY21 EBITDAI guidance range to $1,100-$1,130 million, and full-year dividend guidance to the top end of the range at 25 cents per share.

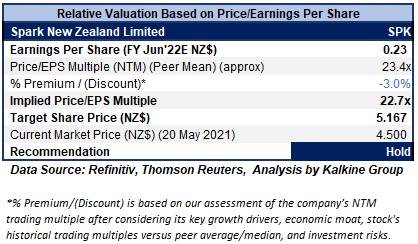

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation

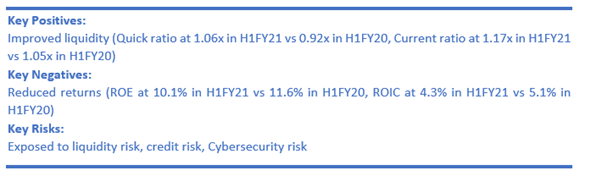

We have applied Price/Earnings Per Share (P/E) based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied a slight discount to P/E Multiple (NTM) (Peer Average) considering the fact that the company has narrowed FY 2021 EBITDAI guidance range and fall in ROE.

For the purposes, we have taken peers such as Chorus Ltd (CNU.NZ), Telstra Corporation Ltd (TLS.AX), and China Telecom Corp Ltd (0728.HK) to name a few.

Considering the aforesaid facts, we give a “Hold” recommendation on the stock at the current market price of $4.5 per share, up 1.69% on 20th May 2021.

3) Pushpay Holdings Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$1.82 billion)

Business Description:

Pushpay Holdings Limited (NZX: PPH) offers the donor management system, including donor tools, finance tools as well as custom community app, and a church management system (ChMS) to the faith sector, non-profit organisations as well as education providers located mainly in the US and other jurisdictions.

Outlook

The company is expected to grow the number of customers using the donor management system in FY22 and the overall growth is anticipated to be in line with US GDP growth. Further, it forecasts digital acceptance within the customer base to grow, though the growth rate will be slower than before the COVID-19 driven acceleration. Importantly, Earnings before Interest, Tax, Depreciation, Amortisation, Foreign Currency (gains)/losses and Impairments (EBITDAFI) is expected to be in the range of US$64.0-US$69.0 million.

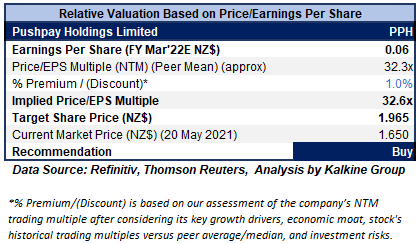

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation

We have applied Price/Earnings Per Share (P/E) based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied a slight premium to P/E Multiple (NTM) (Peer Average) considering the growth in digital acceptance and improvement in ROE in FY 2021.

For the purposes, we have taken peers such as Vista Group International Ltd (VGL.NZ), EML Payments Ltd (EML.AX), and Sezzle Inc (SZL.AX) to name a few.

Considering the aforesaid facts, we give a “Buy” recommendation on the stock at the current market price of $1.65 per share, up by 0.61% on 20th May 2021.

4) Chorus Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$2.88 billion, Gross Dividend Yield: 5.436%)

Business Description:

Chorus Limited (NZX: CNU) happens to be NZ’s largest fixed-line telecommunications network operator and it builds and manages an open-access internet network.

Outlook

The company expects EBITDA for FY21 to be in the range of $640-$660 million, subject to no significant changes in the expected regulatory as well as competitive outlook. Further, Capex is expected in the range of $125-$145 million for UFB2 communal, however, gross Capex has been planned between $670-$700 million. Importantly, the dividend is expected at 25 cps for FY 2021. This guidance indicates a strong plan of the company to capitalize on future opportunities and grow the business to the next phase.

Valuation Methodology: Price/CF Multiple Based Relative Valuation (Illustrative)

.png)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation

We have applied Price/Cash Flow (P/CF) based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied a slight premium to P/CF Multiple (NTM) (Peer Average) considering strong capex plan and constant strategy shift to capitalize on future opportunities.

For the purposes, we have taken peers such as Spark New Zealand Ltd (SPK.NZ), Telstra Corporation Ltd (TLS.NZ), and 5G Networks Ltd (5GN.AX)to name a few.

Considering the aforesaid facts, we give a “Buy” recommendation on the stock at the current market price of $6.44 per share, up 2.88% on 20th May 2021.

Comparative Price Chart (Source: Refinitiv (Thomson Reuters))

Note: Investment decision should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the Valuation has been achieved and subject to the factors discussed above.

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...