Company Overview: EBOS Group Limited is the largest and most diversified Australasian marketer, wholesaler and distributor of healthcare, medical and pharmaceuticals products. It is also a leading marketer and distributor of recognised consumer products and animal care brands. It has more than 3,600 employees in 57 locations across Australasia. The company is listed on the New Zealand and Australian stock exchanges. The company’s major products and services are the same as reportable segments, i.e. Healthcare and Animal Care, and no major products and services are allocated to the corporate.

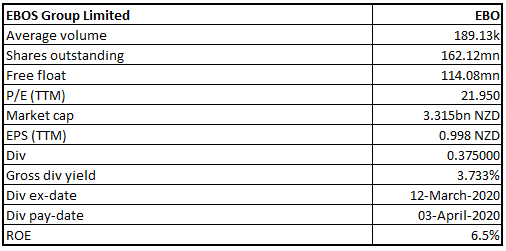

EBO Details

Investment Summary

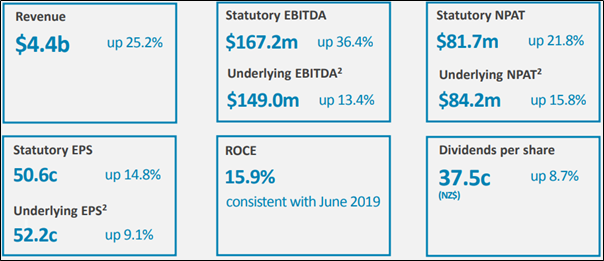

Decent Results Posted in 1H FY 2020: EBOS Group Limited (NZX: EBO) happens to be a leading marketer and distributor of recognised consumer products and animal care brands which has a market capitalisation amounting to ~$3.315 billion on 16th March 2020. For the six months ended 31st December 2019, the company reported total revenue of A$4.4 billion, up by 25.2% and statutory EBITDA of A$167.2 million, up by 36.4%. The growth in total revenue was primarily due to strong sales growth in Healthcare business which was up 26.1% on last year, and Animal Care growth of 9.5% on the previous year’s first half.

Underlying EBITDA stood at A$149.0 million, and underlying NPAT stood at A$84.2 million, both up by 13.4% and 15.8%, respectively. The results indicate commencement of CWG (Chemist Warehouse Group) pharmaceutical wholesale contract, combined with strong performances from Contract Logistics, Institutional Healthcare and TerryWhite Chemmart (TWC) Group businesses indicating the strength of the company’s business model. The company declared an interim dividend of NZ 37.5 cents per share, an increase of 8.7% on the prior corresponding period.

Result Summary (Source: Company Reports)

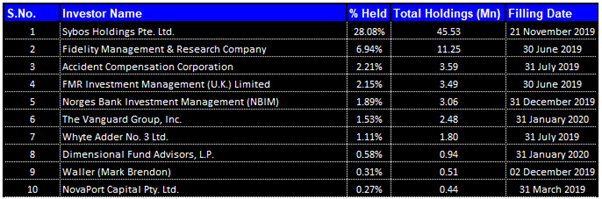

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together forms around 45.07% of the total shareholding. Sybos Holdings Pte. Ltd. and Fidelity Management & Research Company are holding maximum interests in the company at 28.08% and 6.94%, respectively (as shown in the table below):

Top 10 Shareholders (Source: Thomson Reuters)

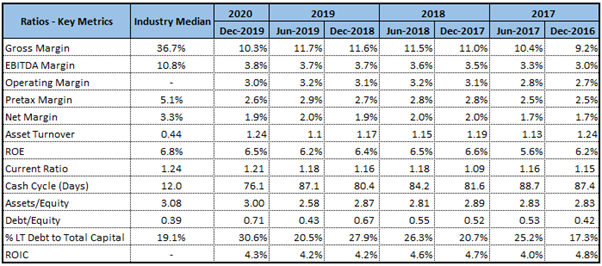

Brief Overview of Key Metrics: In 1HFY20, the company reported EBITDA margin of 3.8%, up from 3.7% in 1HFY19. Its RoE also increased from 6.4% in 1HFY19 to 6.5% in 1HFY20. This implies that the company generated a better return for its shareholders than the previous half and this might attract the attention of the market participants moving forward.

Key Metrics (Source: Thomson Reuters)

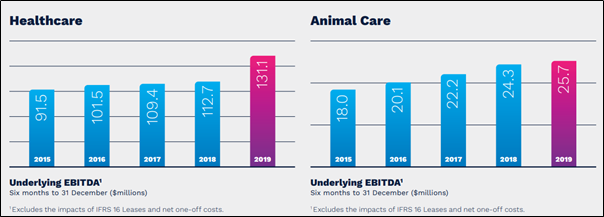

Decent Growth in Both the Segments: The Healthcare segment registered revenue of A$4.2 billion, up by 26.1% for the period, supported by substantially higher Pharmacy sales volumes and continued growth in the Contract Logistics, Institutional Healthcare and TWC businesses. In Australia, Healthcare revenue increased by A$786 million (30.9%) and Underlying EBITDA increased by 22.3% driven by the performance of Pharmacy, Institutional Healthcare and Contract Logistics businesses and the commencement of the Chemist Warehouse Group (CWG) pharmaceutical wholesale contract.

New Zealand Healthcare revenue was up by 9.9%. However, underlying EBITDA was impacted by weaker overseas demand for consumer products, reflective of the changes which have affected the daigou export channel. The Animal Care segment registered revenue of $211 million, up by 9.5% for the period, mainly due to a combination of the continued outstanding performance from the branded products portfolio along with higher wholesale volumes.

Segment Overview (Source: Company Reports)

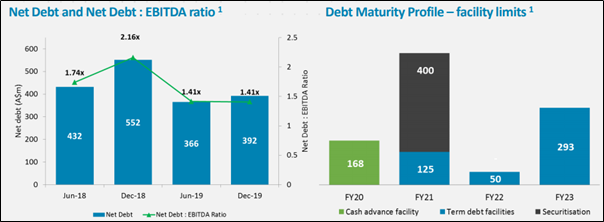

Robust Financial Position in First Half: For the six months period, the capital expenditure was A$13.7 million primarily comprised spend on the new Consumer Products facility in Auckland and other smaller projects. During the period, the Group purchased LMT/NS for $34 million. Return on Capital Employed (ROCE) stood at 15.9%, consistent with June 2019 with the strong earnings growth partially offset by the seasonality of the working capital cycle.

The company’s Net Debt/EBITDA ratio at 31 December 2019 was consistent with 30th June 2019 at 1.41 times. Operating cash flow before the capital expenditure was strong at A$74.2 million.

Net Debt and Maturity Profile (Source: Company Reports)

Strategic Highlights During First Half: The Australian wholesale business demonstrated its leading competitive position with a substantial increase in revenues and profit, again reflecting the strength of the company’s long term plan of driving productivity and consistently building capacity to create Australia’s leading network of pharmacy distribution infrastructure. The acquisition of LMT/NS for $34 million indicates the company’s access to the A$8 billion Australian and New Zealand medical device sector establishing a new platform of growth for EBO. The new 25,000m² Contract Logistics facility in Sydney has allowed strong growth in Australian Contract Logistics business.

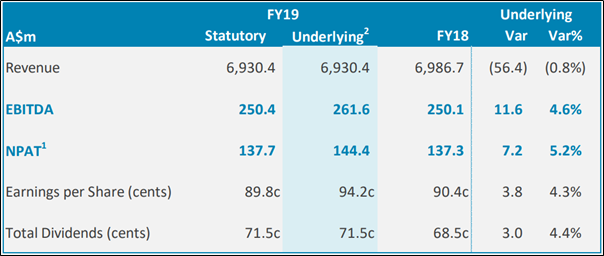

Strong Growth in Underlying Earnings: During FY19, the company reported underlying EBITDA of A$261.6 million, up 4.6% and underlying net profit after tax of A$144.4 million, up 5.2%. The company declared a final dividend of NZ 37 cents per share, taking the full-year dividends to NZ 71.5 cents per share, up 4.4% from the previous year.

FY19 Summary Results (Source: Company Reports)

Segmental Performance: The healthcare segment reported underlying EBITDA of A$226.6 million, up 4.6% as a result of solid growth from Australian business unit. However, in Australia, Healthcare revenue declined by $183 million (-3.5%). The New Zealand Healthcare business posted earnings in line with the last year, and the revenue growth of 8.7% was largely offset by increased labour as well as freight costs in wholesale businesses.

The animal care business generated EBITDA of A$48.3 million, up 5.7% as the business continues to gain from the excellent performance of branded products.

Financial Position in FY19: The company’s operating cash flow before capital expenditure stood at A$118.5 million. Net capital expenditure for the year was $26.6 million and mainly consisted of final payments on the new distribution facility in Brisbane and other improvements across Symbion’s warehouse network in preparation for the increased volumes from CWG stores. In the month of May 2019, the company raised NZ$175 million in new equity capital. The funds which were received from equity raise have initially been utilised towards the repayment of bank debt and are anticipated to be deployed from FY 2020 towards strategic acquisitions along with organic growth opportunities. As a result of debt repayment, the company’s Net Debt/EBITDA ratio, at June 30, 2019, stood at 1.41x.

Next Wave of Growth in FY20: FY19 was an important year for the company as it has set the groundwork for the next wave of growth. The company started operations in two brand new facilities in Sydney and Brisbane that provides further warehouse capacity. The company also retained Blooms the Chemist, moved to 100% ownership of TerryWhite Chemmart and signed the Chemist Warehouse Group pharmaceutical contract.

Changes in Top Management: The CFO of the company Shaun Hughes has resigned from the company and will leave the business on 10th June 2020. In the interim period, Mr Leonard Hansen, the company’s Chief Accountant, would be the acting CFO. As per another release, the company has appointed Mr Nick Dowling as an Independent Director.

Outlook for FY20: After doing the acquisition of established distribution business LMT and National Surgical at a purchase price of $34 million, the company has entered the A$8 billion Australian and New Zealand medical device sector. The company is confident about a significant increase in earnings in the current financial year. There has not been any significant impact of the coronavirus. However, the company is closely monitoring this issue and will take all necessary actions to ensure it is well placed to respond to any challenges that arise.

.png)

Key Valuation Metrics (Source: Thomson Reuters)

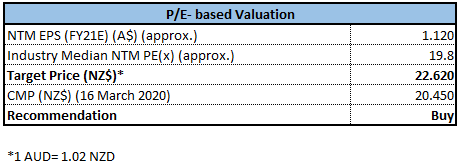

Valuation Methodology: P/E Based Relative Valuation

P/E Based Relative Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months.

Technical Overview:

Monthly Chart –

Source: Thomson Reuters

Weekly Chart –

Source: Thomson Reuters

Daily Chart –

Source: Thomson Reuters

Note: Purple colour lines are bollinger bands, yellow lines are retracement levels and orange colour dotted line is Parabolic SAR.

The stock made smart rally with periodic bullish consolidations and bullish break-out and reached the peak of $25.68 in the month of Nov. 2019. From the peak, the stock has slide to $19.6 by now. The fall in the stock price has been relatively steeper in the month of March 2020. There was gap down opening for the stock and by now, it has already made the low of $19.6 and is currently around $20.26.

While MACD with bullish cross-over and RSI reading of 45 show bullish momentum for the stock remaining intact in the medium-term, bearish cross-over for MACD, and RSI reading of 33 and 23 on the weekly and daily charts, suggest near-term weakness in trend for the stock.

We believe that the resilience in the stock continues and the oversold status would limit the downside for it to its low of $19.60 which may act as an initial support and it is only when greater sell-off take place that stock would fall below, finding strong support around $19.00. While on technical rebound, the stock might move up around $22.00 where it will have initial resistance and beyond that 50% retracement level of $22.63 would provide strong resistance.

Stock Recommendation: In the time period of FY15 to FY19, the company’s net income has grown at a CAGR of 8.71%. Its gross profit has also grown at a CAGR of 9.61% in FY15 to FY19. Currently, the stock is trading below the average of 52-week low and high of $19.60 and $25.600, respectively. Therefore, it can be said that current trading levels are offering decent opportunity for accumulation. Considering the growth opportunities in Australasian market after the acquisition of LMT/NS, current trading levels and decent outlook, we have valued the stock using P/E based relative valuation approach and have arrived at a target price of lower double-digit growth (in percentage terms).

Hence, we recommend a “Buy” rating on the stock at the current market price of NZ$20.450 per share, down by 6.62% on March 16, 2020.

EBO Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...