Company Overview: EBOS Group Limited (NZX: EBO) is a marketer, wholesaler and distributor of healthcare, medical and pharmaceutical products. The company is also a leading marketer as well as a distributor of recognised consumer products and animal care brands. The Healthcare segment incorporates the sale of healthcare products in a range of sectors, own brands, retail healthcare, wholesale activities and logistics. The Animal care segment incorporates the sale of animal care products in a range of sectors, own brands, retail and wholesale activities. Its businesses include Community Pharmacy, Institutional Healthcare, Contract Logistics and Animal Care. Community Pharmacy includes Symbion, Endeavour Consumer Health, ProPharma, DoseAid and Intellipharm. Institutional Healthcare includes EBOS Healthcare, Onelink, Clinect and Zest.

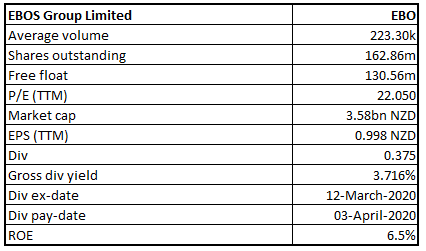

EBO Details

Investment Summary:

Decent Performance in 1H FY 2020: EBOS Group Limited (NZX: EBO) is a leading marketer and distributor of healthcare products and animal care brands. The company generates more than A$7 billion of revenue in FY19 and has leading market positions across Australia and New Zealand. It is a diverse group with presence across sectors and geographies and operates across the value chain, which has supported stability in its earnings growth and cash flow generation.

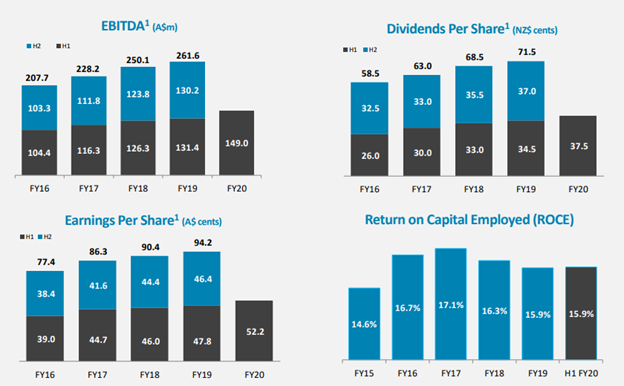

Looking at the past performance over FY15 to FY19, top line and bottom line of the company witnessed a compounded annual growth rate (CAGR) of ~5.25% and ~8.71%, respectively. The company’s total revenue improved from A$5,648.2 million in FY15 to A$6,930.4 million in FY19, and its net income improved from $98.6 million in FY15 to $137.7 million in FY19.

Group revenue increased by 25.2% to $4.4 billion in H1FY20, evidencing the strength of the company’s portfolio of businesses with substantial growth in Pharmacy Wholesale and strong performances from TerryWhite Chemmart, Institutional Healthcare and Contract Logistics. The Australian wholesale business demonstrated its leading competitive position with a significant increase in revenues and profit. It reignited the growth of TerryWhite Chemmart (TWC), one of Australia's leading community pharmacy networks. The TWC network delivered 5.7% sales growth on the prior period and added 16 new stores to the network. There was successful commencement of the Chemist Warehouse Group contract from 1 July 2019.

The acquisition of LMT and National Surgical (LMT/NS) for $34m signals EBOS’ entry into the A$8 billion Australian and New Zealand medical device sector creating a new platform of growth for the Group. It expects a significant rise in FY20 earnings.

Historical Performance (Source: Company Reports)

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together forms around 35.07% of the total shareholding. Sybos Holdings Pte. Ltd. and Fidelity Management & Research Company are holding maximum interests in the company at 18.74% and 5.70%, respectively, as provided in the table below:

Top 10 Shareholders (Source: Refinitiv (Thomson Reuters))

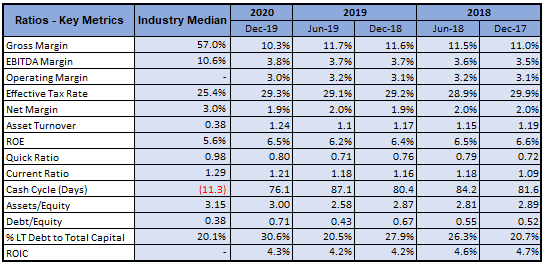

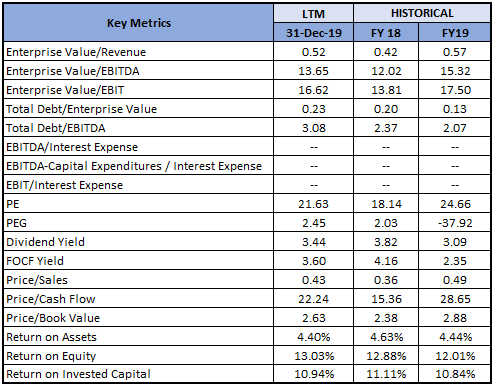

A Quick Look at Key Metrics: The company recorded an improvement in EBITDA margin to 3.8% in H1FY20 as against 3.7% in the previous corresponding period. Its net margin in H1FY20 stood at 1.9%, in-line to the previous corresponding period. Its RoE for first half FY20 stood at 6.5%, better than the industry median of 5.6%, implying the company generated better returns for the shareholders than its peer group.

Key Metrics (Source: Refinitiv (Thomson Reuters))

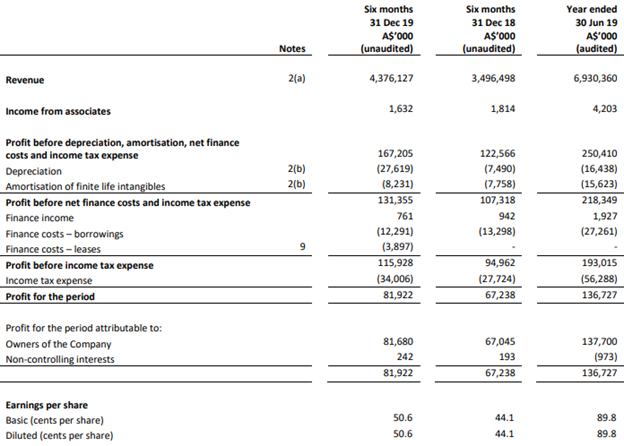

Robust Operating Cash Flow for First Half FY20: Significant revenue increase of 25.2% in the first half period of FY20 was primarily due to growth in Pharmacy Wholesale, TerryWhite Chemmart, Institutional Healthcare and Contract Logistics. Underlying EBITDA, Underlying NPAT and Underlying EPS increased by 13.4%, 15.8% and 9.1%, respectively on pcp. Healthcare growth in revenue of 26.1% and Underlying EBITDA of 16.3% was driven by the performances of Community Pharmacy, TWC, Institutional Healthcare and Contract Logistics businesses.

Revenue growth of $18.3 million in animal care segment, or 9.5%, was due to the continued excellent performance of its branded products portfolio and higher veterinary wholesale volumes.

Statutory Operating Cash Flow stood at $74.2 million, an increase of $34.0 million due to the significant increase in earnings and continued working capital management. Net debt, as on December 31, 2019, stood at $392 million as against $552 million in H1FY19.

H1FY20 Income Statement (Source: Company Reports)

A Look at Key Updates: On June 16, 2020, the company announced that a mutually beneficial outcome with the Federal Government had been achieved after the recent execution of 7th Community Pharmacy Agreement. The company, through its market-leading national healthcare wholesaler and wholly-owned subsidiary Symbion, together with members of the National Pharmaceutical Services Association (NPSA), was actively engaged in negotiations with the Department of Health and Federal Minister for Health, The Honourable Greg Hunt MP, with respect to a successful outcome for the 7th CPA. The new arrangements provide CSO wholesale distributors with an additional $92 million investment into the CSO funding pool, and introduction of a restructured wholesale mark-up for PBS medicines, to continue to support medicine supply through the wholesaler network over the next five years.

What to Expect: The company’s healthcare and animal care have a strategic focus on establishing and further strengthening the leading market positions and maximise opportunities across the diverse range of businesses. Under capital expenditure, the company is expected to maintain and extend its market leadership through continued investment in its lowest-cost-per-unit distribution network, allowing it to deliver optimal customer outcomes. Its cash generation is expected to drive further investment and pay dividends of not less than 60% of Net Profit After Tax. Its strategic focus is on assets with Return on Capital Employed (ROCE) of at least 15%.

Key Risks: EBO is exposed to foreign currency risk arising primarily from the procurement of goods denominated in foreign currencies (US dollar, Australian dollars, Thai baht, euro and British pound). It is exposed to interest rate risk as it borrows funds in both New Zealand dollars and Australian dollars at floating interest rates. It is exposed to the risk of default in relation to receivables owing from its healthcare and animal care customers, hedging instruments and guarantees and deposits held with banks and other financial institutions.

Key Valuation Metrics (Source: Refinitiv (Thomson Reuters))

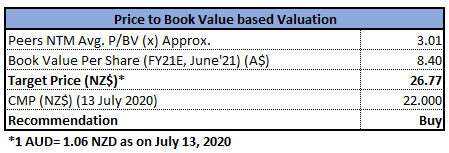

Valuation Methodology: Price to Book Value Multiple Based Relative Valuation (Illustrative)

Price to Book Value Multiple Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Technical Overview:

Weekly Chart –

.png)

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands with upper band suggesting overbought status while lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack.

Despite stronger start for the on-going week, the stock has given flattish close at $22.00 which is also the previous week closing price. The fact that, the closing for the stock is around 50% retracement level, we see the strength in bullish trend. Technical indicator RSI with 46 reading, suggests gaining of bullish momentum for the stock.

Going forward, the stock may have resistance around $23.67, as provided by the upper Bollinger band while support could be around a 38.2% retracement level of $21.18.

Stock Recommendation: The crisis caused by devastating bushfires and COVID-19 have demonstrated the critical role that the company plays in ensuring access to critical medicines even under the most challenging environment. Its strong balance sheet is supported by good liquidity and a Net Debt-to-EBITDA ratio of 1.41x.

Considering the aforesaid facts, we have valued the stock using a relative valuation method, i.e., Price to Book Value multiple based relative valuation (on an illustrative basis) and we have arrived at a target price of lower double-digit growth (in % terms).

Hence, we give a “Buy” recommendation on the stock at the current market price of NZ$22.000 per share on July 13, 2020.

EBO Daily Technical Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...