.png)

I. Sector Landscape and Outlook

As per the Ministry of Business, Innovation & Employment, the government plans a market study on supermarkets. It identified some discrepancy in the bargaining power of supermarkets and suppliers that is shifting prices unreasonably low for suppliers, which could impact investment in innovation and quality. However, this difference benefits consumers, but it is uncertain how much of this is passed onto consumers, with the cost of food comprising 17% of household weekly expenses. As per the Commerce Commission New Zealand (COMCOM), groceries are the primary purchase for all New Zealanders in the year to December 2020, touched $22 billion. In the year to June 2019, food happened to be the second-largest expenditure item for households, with average spending of $234 a week on it.

Consumer Spending Rose in September 2021 Quarter

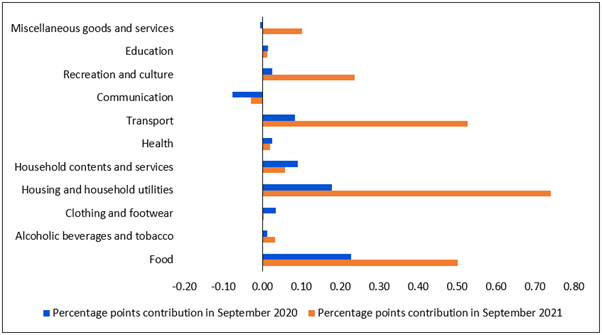

As per Stats.NZ, the consumer price index (CPI) increased 2.2% in the September 2021 quarter versus June 2021 quarter (up 2.1% with seasonal adjustment), where transport grew 4.2%, driven by private transport supplies and services (up 5.1%) and passenger transport services (up 17%). This was followed by recreation and culture that increased 2.9%, driven by other recreational equipment and supplies (up 5.6%) and accommodation services (up 3.2%). The food grew 2.7%, driven by fruit and vegetables (up 11%) and grocery food (up 1.3%), and housing and household utilities increased 2.6%, driven by higher prices for homeownership (up 4.5%) and property rates and related services (up 7.0%).

Exhibit 1: Quarterly Percentage Points Contribution to CPI, by Group, September 2021 Quarter

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

Electronic Card Transactions Surged in October 2021 Over September 2021

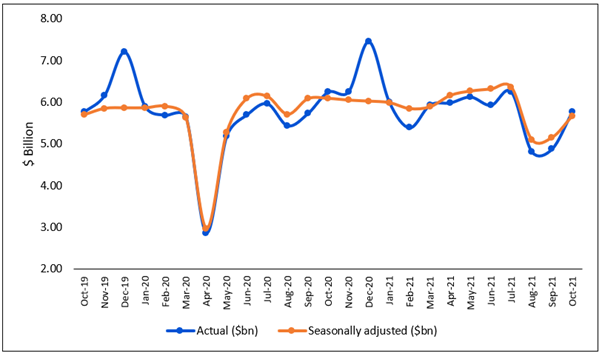

As per Stats.NZ, the electronic card transactions relating to spending in the retail industries increased 10.1% ($519 million) in October 2021 versus September 2021. Also, the spending in the core retail industries grew 8.7% MoM ($397 million). When analysed spending by category, the motor vehicles (excluding fuel) grew $40 million (up 26.9% MoM), apparel grew $35 million (up 18.6% MoM), fuel grew $69 million (up 16.3% MoM), durables grew $149 million (up 11.5% MoM), while consumables decreased $6 million (0.2% MoM).

In addition, the electronic card transactions in supermarkets and grocery stores grew $181 million (9.5% YoY) in October 2021 versus October 2020, while specialised food decreased $18 million (7.8% YoY) and liquor decreased by $8 million (3.8% YoY).

Exhibit 2: Trend in Retail Card Spending ($), Monthly, October 2019–2021

Data Source: This work is based on/includes the Ministry for Primary Industries data which are licensed under Crown for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

Impact of COVID-19 Continues to Disrupt International Travel

As per Stats.NZ, the number of visitor arrivals stood at 208,000, down by 2.0 million in September 2021 versus the September 2020 year. This was primarily led by Australia (down 639,000), the United States (down 235,000), the United Kingdom (down 165,000), and China (down 160,000). In addition, the number of NZ-resident traveller arrivals stood at 139,000, down by 1.3 million in the said period.

In addition, overseas visitor arrivals decreased by 3,200 to 2,300 in September 2021 versus September 2020, primarily led by Australia (down 1,400), the United Kingdom (down 500), and the United States (down 300). However, NZ residents returning from an overseas trip in September 2021 increased by 500 to 3,200 versus September 2020.

Supermarket and Grocery Stores Reported the Biggest Rise in September 2021 Quarter

As per Stats.NZ, supermarket and grocery stores reported the most significant rise in the volume of 7.5%, followed by non-store and commission-based retailing, which grew 2.5% in September 2021 quarter over June 2021 quarter. However, 12 of 15 industries had reported lower sales volumes in the September 2021 quarter versus June 2021 quarter, driven by food and beverage services that decreased 19%, motor vehicle and parts retailing decreased 12%, department stores decreased 24%, and hardware, building, and garden supplies decreased 15%.

Index Performance:

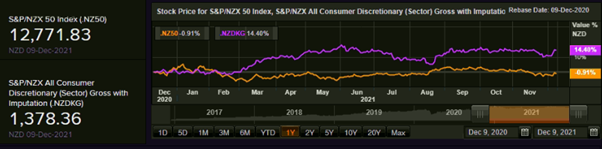

The S&P/NZX All Consumer Discretionary Index generated a 1-year return of ~14.40% versus ~-0.91% by the S&P/NZX 50 Index. Therefore, S&P/NZX All Consumer Discretionary Index overperformed S&P/NZX 50 Index by ~15.31% in 1-year.

Exhibit 3: S&P/NZX All Consumer Discretionary Index vs S&P/NZX All Index

Source: REFINITIV

Key Risks and Challenges:

As per COMCOM, the retail market is exposed to an expected rise in prices in the future if some suppliers plan to exit the market, thereby reducing competition between the remaining suppliers. Meanwhile, the consumers could benefit from private label products through reduced prices and multiple choice. This will favour private label products in the short term, but there is a risk that the rise of private labels could crowd out supplier branded products. This may lead to a loss of consumer choice and higher prices in the longer term.

As per Stats.NZ, since January 2020, the government imposed international travel restrictions due to COVID-19 related circumstances, effectively limiting travel to NZ. Two-way quarantine-free travel opened with Australia on 19 April 2021 and the Cook Islands on 17 May 2021. Since then, the restrictions have continued to impact travel with Australia and, more recently, with the Cook Islands. These circumstances are expected to continue further round the world until confidence in travel and the situation returns to pre-Covid level.

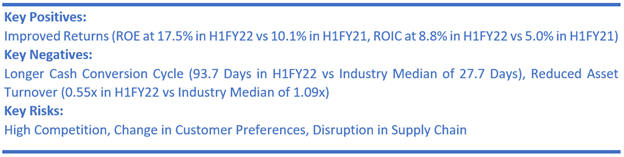

Exhibit 4. Key Risks in Consumer Discretionary Sector:

Sources: Analysis by Kalkine Group

Outlook:

The Reserve Bank of New Zealand's seasonally adjusted total monthly credit card billings stood at $3.6 billion in October 2021, up 8.4% from $3.3 billion in September 2021. In addition, seasonally adjusted domestic billings on NZ issued cards stood at $3.4 billion, up 9.3% from September 2021. This indicates growing confidence and recovery in the economy to rise further. However, some short-term headwinds were identified as per the September 2021 quarter retail trade survey compared with the June 2021 quarter. In September 2021 quarter, the sales volume in food and beverage services decreased 19%, motor vehicle and parts retailing fell 12%, and department stores decreased 24%.

Meanwhile, the tourism industry is asking the government to relent and abandon self-isolation for visitors coming from Australians sometime in 2022. Australians accounted for ~40% of NZ's international visitors during pre-pandemic or 1.5 million visitors and 20% of the global tourism spending on the travelling front.

Apart from the sector-specific factors, we have also analysed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

1) Briscoe Group Limited (Recommendation: Buy, Potential Upside: Low Double-Digit (M-Cap: NZ$1.51 billion, Gross Dividend Yield: 6.286%)

Business Description:

Briscoe Group Limited (NZX: BGP) operates more than 85 stores across NZ within two retail sectors, homeware, and sporting goods, under the three brand names: Briscoes Homeware, Living & Giving and Rebel Sport.

Outlook:

Driven by last year's performance, the company anticipates pent-up demand to drive strong sales from October 2021 to 30 January 2022. If that holds and NZ continues to progress without other lockdowns or outbreaks, the company expects to produce an NPAT above last year’s record of $73.2 million and up to $85 million.

On 5 November 2021, the company released its year-to-date to 31 October 2021 performance highlights, where the group sales stood at $496.9 million (up 9.52%), homeware sales growth grew 9.53%, sporting goods sales grew 9.50%, and online sales as a mix of total Group sales stood at 22.14%.

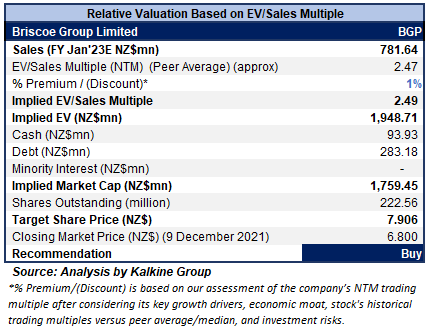

Valuation Methodology: EV/Sales Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

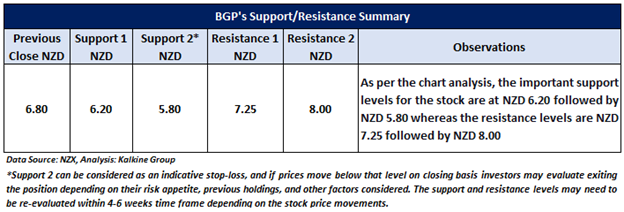

Stock Recommendation

The stock has been valued using an EV/Sales multiple-based illustrative relative valuation, and the target price so arrived reflects a rise of low double-digit (in % terms). A slight premium has been assigned to EV/Sales Multiple (NTM) (Peer Average), as online sales reported 98% growth in Q3FY22 and represented 38% of all total sales. Also, the managed continues to maintain a high standard of service despite the massive increase in online demand.

Considering the facts above, we give a “Buy” recommendation on the stock at the closing market price of $6.80 per share, down 0.73% as of 9th December 2021.

2) Burger Fuel Group Limited (Recommendation: Speculative Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$17.87 million)

Business Description:

Burger Fuel Group Limited (NZX: BFG) has experience in the restaurant sector, stretching over 20 years, going back to the original BurgerFuel store that opened in 1995. It operates three brands: Shake Out, BurgerFuel and Winner Winner.

Outlook

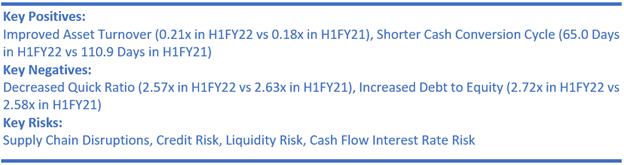

The company has proven to be robust throughout the pandemic alert levels. There are expectations that it could remain stable and continue to deliver a solid performance in the future period. However, the new brands are less confident, whereas whilst Shake Out is performing well enough, Winner Winner is far more affected in certain areas. Moreover, the company maintains substantial cash reserves. It will continue to see new opportunities to develop current brands and future company growth that may place the company in the new future.

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

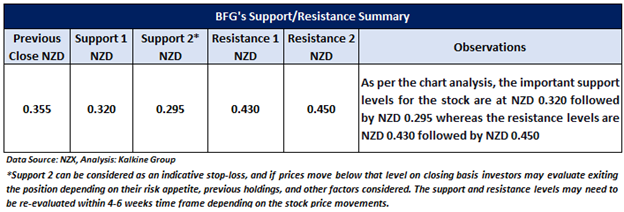

Stock Recommendation

Considering the facts above, we give a “Speculative Buy” recommendation on the stock at the closing market price of $0.355 per share, up 1.43% as of 9th December 2021.

3) Tourism Holdings Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$433.10 million)

Business Description:

Tourism Holdings Limited (NZX: THL) is the leading tourism company in New Zealand and is engaged in providing holiday vehicles for rent and sale in Australia, New Zealand & USA.

Outlook:

The company believes it is better to succeed when international tourism returns with the RV category growing worldwide. The company is increasing its revenue share in each of the RV markets of its operations. Further, the company continues to emphasise various domestic growth prospects to drive growth that includes setting up the RV Super Centre as the one-stop shop for entire RV-related work in New Zealand and expanding the vehicle sales businesses by launching new ‘direct-to-yard’ vehicles and updating fleet designs.

Valuation Methodology: EV/Sales Based Relative Valuation (Illustrative)

.png)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

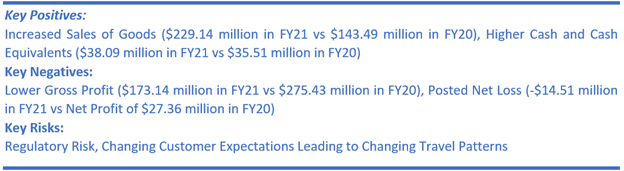

The stock has been valued using EV/Sales multiple-based illustrative relative valuation, and the target price so arrived reflects a rise of low double-digit (in % terms). A slight discount has been assigned to EV/Sales Multiple (NTM) (Peer Median), considering its net loss after tax of $14.5 million in FY21, uncertainty on the outlook for international tourism, mainly for New Zealand and Australia, and expectation of reporting a net loss for FY22.

Considering the facts above, as well as its well managed balance sheet with net debt of $49 million and refinanced debt facilities of up to $250 million through to 2024, and the associated business risks, we give a “Hold” recommendation on the stock at the closing price of $2.85 per share, down 1.04% as of 9th December 2021.

4) Hallenstein Glasson Holdings Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$423.51 million, Gross Dividend Yield: 8.638%)

Business Description:

Hallenstein Glasson Holdings Limited (NZX: HLG) is a retail company engaged in retailing menswear and womenswear. The company operates more than 130 stores, with 36 stores in Australia.

Outlook

The company continues its investment in digitization to stay ahead of the market in terms of functionality and technology and its web fulfilment in Distribution Centers. To drive online sales growth, HLG continues to focus on digital marketing and customer experience. Meanwhile, the group witnessed a decline in sales by 18.90% in the first eight weeks of FY22 compared to the prior year, mainly due to the impact of multiple store closures across both New Zealand and Australia amid the recent COVID‐19 outbreaks. Considering uncertainty about the date for reopening the Auckland stores and the opening of NSW and VIC, the group forecasts its FY22 profitability to be adversely impacted compared to FY21.

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

Considering the facts above, along with strong brand positioning in both established markets and new markets, and the associated business risks, we give a “Hold” recommendation on the stock at the closing price of $7.10 per share, down 0.14% as of 9th December 2021.

Note 1: The reference data in this report has been partly sourced from REFINITIV.

Note 2: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the analysis has been achieved and subject to the factors discussed above alongside support levels provided.

Technical Indicators Defined: -

Support: A level where-in the stock prices tend to find support if they are falling, and downtrend may take a pause backed by demand or buying interest.

Resistance: A level where-in the stock prices tend to find resistance when they are rising, and uptrend may take a pause due to profit booking or selling interest.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is authorised to provide general advice only. The information on this website does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...