Company Overview: Energy generator and digital retailer, Contact Energy Limited (NZX: CEN) is engaged in providing electricity, natural gas, and liquefied petroleum gas (LPG), and broadband services. It generates electricity through hydro, geothermal, and thermal sources.

It operates under two segments including Generation segment and Customer segment. The Generation segment is engaged in the business of selling electricity to the wholesale electricity market and to the Customer segment. The Customer segment delivers services and distributes energy to customers. It sells electricity, gas and LPG products and services to residential, small business, commercial and industrial customers. The Company's stations include Ahuroa and Stratford in Taranaki; Ohaaki, Poihipi and Te Rapa in Waikato, Te Huka and Te Mihi in Taupo Wairakei in Taupo, and Whirinaki in Hawke’s Bay. It is also involved in the development of geothermal energy projects.

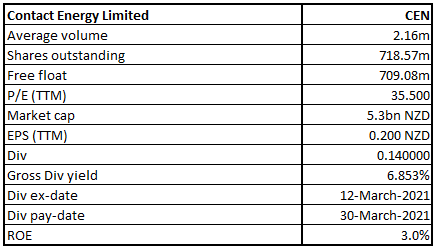

CEN Details

CEN is at the forefront of electricity generators in NZ. The company happens to be strongly positioned in wholesale gas distribution, gas retailing as well as electricity retailing.

Result Performance (Ended December 31, 2020)

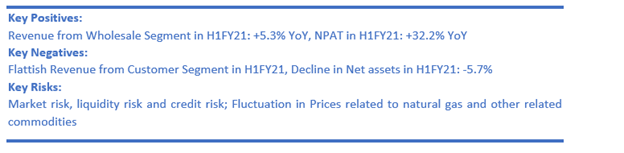

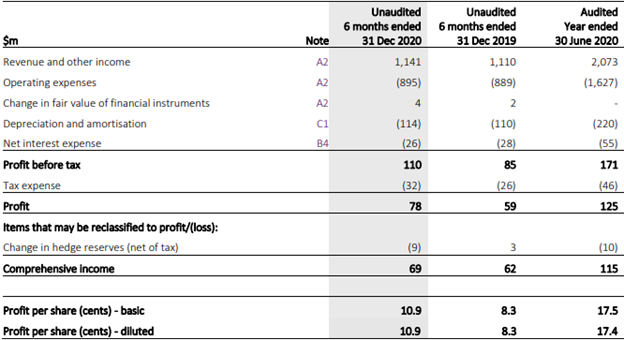

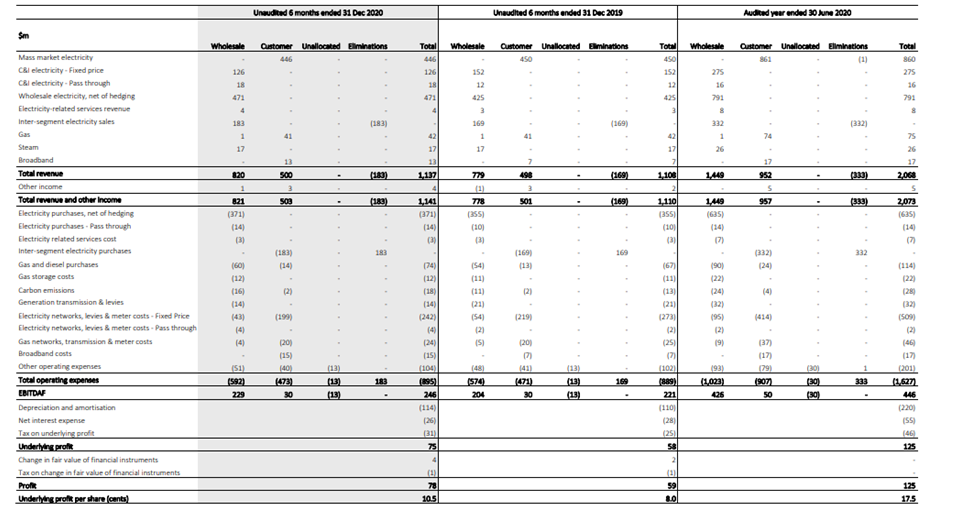

The company’s revenue and other income for FY20 stood at $1,141 million, as compared to $1,110 million in the previous corresponding period. EBITDAF for the interim period stood at $246 million, an increase of 11% on the prior year. Profit for the period stood at $78 million, an increase of 32% on the same period last year of $59 million. Operating free cash flow increased to $157 million, an increase of 31% on pcp. The company managed to deliver a strong result for the interim period despite headwinds in the form of ongoing uncertainty around gas availability and Tiwai Plant closure until an extension was announced recently. The good performance could be attributed to active channel management, strong asset availability, and a disciplined approach to managing commodity risks.

The company has come out with a revised dividend policy to distribute dividends targeting a payout ratio of between 80-100% of the average operating cash flow of the preceding four financial years. In the meanwhile, the Board of the company has approved an interim cash dividend of 14 cents per share with a payment date on 30 March 2021. For FY21, the target payment for the full-year dividend is 35 cents per share.

Exhibit 1: Income Statement

Key Data (Source: Company Reports)

Segment Performance:

Revenue from the wholesale segment stood at $820 million, as compared to $779 million in the previous corresponding period (pcp). EBITDAF stood at $229 million, as compared to $204 million in the pcp, implying improvement in the operating performance of the company.

Revenue under the customer segment stood at $500 million, as compared to $498 million in the pcp. EBITDAF stood at $30 million, in-line to the pcp.

Exhibit 2: Revenue Streams

(Source: Company Reports)

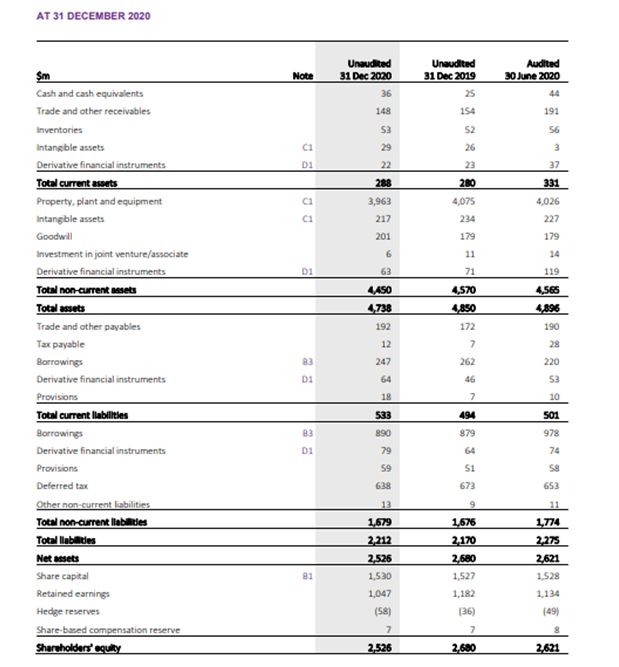

The cash balance as on December 31, 2020, stood at $36 million, as compared to $25 million in the previous corresponding period (pcp). Inventories value stood at $53 million, close to the level of the previous corresponding period (pcp). Trade and other receivables for the period stood at $148 million, as compared to $154 million in the pcp.

Exhibit 3: Balance Sheet

(Source: Company Reports)

Results Performance (Year Ended June 30, 2020)

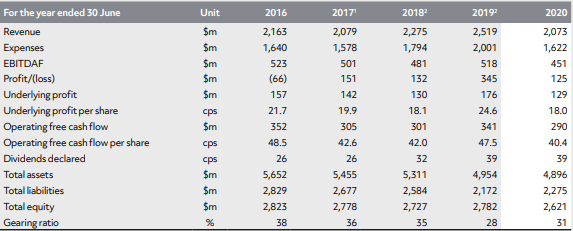

The company reported a decline of 26% in its profit from continuing operations for FY20 (ended June 30, 2020) to $125 million YoY. EBITDAF from continuing operations stood at $451 million, a decline of 11%, due to the impact of rising costs of thermal generation and restricted gas supply, along with lower renewable generation, and lower wholesale prices . CEN’s operating free cash flow for FY20 stood at $290 million, a decline of 15% on the previous year, mainly due to a combination of lower operating earnings, partially offset by lower stay-in-business capital expenditure and interest costs.

Exhibit 4: Key Financial Metrics

Key Data (Source: Company Reports)

Monthly Operating Report (December 2020)

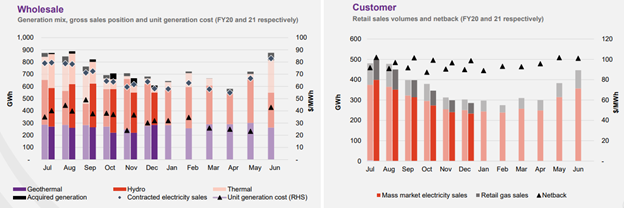

The customer business recorded mass market electricity and gas sales at 286 GWh, as compared to 303 GWh in the previous corresponding period (pcp) and mass-market electricity and gas netback of $98.67/MWh as compared to $89.89/MWh in pcp.

The wholesale business recorded contracted Wholesale electricity sales, including that sold to the Customer business, totaled 582 GWh, as compared to 639 GWh in pcp. Electricity and steam net revenue stood at $70.29/MWh, as compared to $69.64/MWh in pcp. Electricity generated (or acquired) in the period stood at 617 GWh, as compared to 691 GWh in pcp. The unit generation cost stood at $33.29/MWh against $30.13/MWh in the pcp.

Exhibit 5: Key Operating Metrics

Key Metrics (Source: Company Reports)

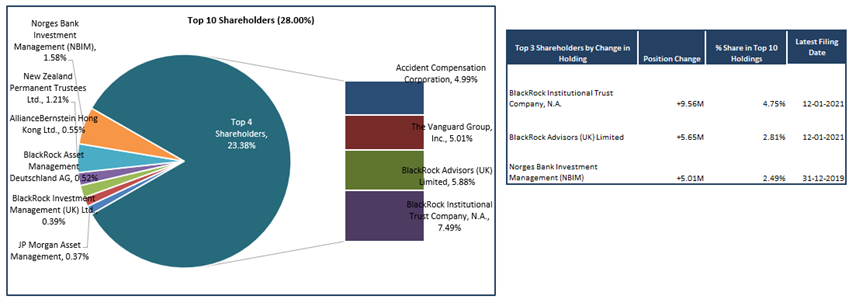

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together forms around 28.00% of the total shareholding. BlackRock Institutional Trust Company, N.A. and BlackRock Advisors (UK) Limited are holding a maximum stake in the company at 7.49% and 5.88%, respectively.

Exhibit 6: Top 10 Shareholders

(Source: Refinitiv (Thomson Reuters)), Analysis by Kalkine Group

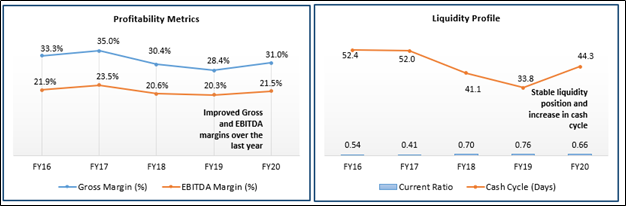

A Quick Look at Key Metrics: The company’s gross margin and EBITDA margin for FY20 stood at 31.0% and 21.5%, better than the FY19 result of 28.4% and 20.3%, respectively, implying an improvement in operating efficiency of the company over the previous year. The company’s debt-to-equity ratio for FY20 stood at 0.46x, better than the industry median of 0.51x, implying decent leverage position of the company.

Exhibit 7: Key Metrics

(Source: Refinitiv (Thomson Reuters)), Analysis by Kalkine Group

Recent Update:

CEN recently announced the opening of the non-underwritten NZ$75 million retail offer. This offer is part of Contact’s NZ$400 million equity raising which was announced on 15th February 2021, pursuant to which it also undertook a fully underwritten NZ$325 million placement of the new shares to institutional shareholders in NZ, Australia as well as certain other jurisdictions. The company has announced the successful completion of the placement on 16th February 2021.

Outlook:

As per the recent announcement on 14 January 2021, Rio Tinto’s Aluminium Smelter in New Zealand will continue to operate until the end of 2024.

CEN has now reached its final investment decision on, and will proceed with, the development of the Tauhara geothermal plant. CEN is undertaking a strategic review of its thermal assets, from which Taranaki Combined Cycle (TCC) assets with a net book value of $107 million will be fully depreciated by 31 December 2023. A useful life review of existing Wairākei assets will also be undertaken in the second half of FY21, allowing for future considerations of how the existing Wairākei A & B stations will be replaced. This may impact the useful life assessment of Wairākei assets going forward.

Exhibit 8: Guidance

.png)

Key Data (Source: Company Reports)

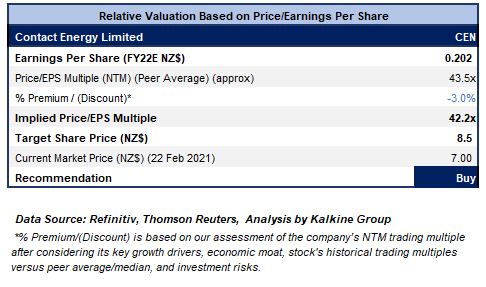

Valuation Methodology: P/E Multiple Based Relative Valuation (Illustrative)

Technical Overview:

Weekly Chart –

.png)

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack. https://www.bollingerbands.com/

The stock has corrected by 61.8% retracement level, by now. The technical indicator RSI with a reading around 43 suggests neutral momentum for the stock.

Stock Recommendation:

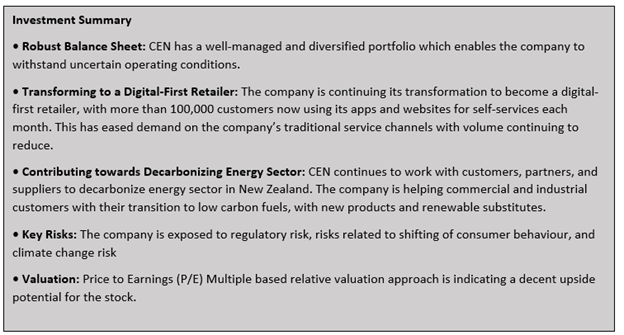

The company aims to optimize its operations in order to reduce costs and maximize shareholders’ return. Improvement in the top-line and bottom-line in the interim period, supports the development initiatives being taken by the company. Recovery in economic activities, non-exit of NZAS till 2024 would be key contributors in driving strong energy demand in the coming times, benefitting the utility companies. In the meanwhile, the company remains focused on improving operational efficiency and leveraging its lean operating model. The company has a robust balance sheet, an excellent portfolio of assets and capable teams which will enable it to capitalize on emerging opportunities.

We have applied P/E multiple Based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied a slight discount to P/E multiple (NTM) (Peer average) considering its historical trading multiple, decline in net assets and risks related to fluctuation in prices related to natural gas and other commodities.

Hence, we give a “Buy” recommendation on the stock at the current market price of $7.00 per share, down by 1.55% on February 22, 2021.

.png)

CEN Daily Technical Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...