Company Overview: Contact Energy Limited (NZX: CEN) is engaged in providing utility services such as electricity, natural gas and liquefied petroleum gas (LPG), and telecom service such as broadband to the residents. It generates electricity via thermal, hydro and geothermal sources. Its two important operational segments are Customer segment and Generation segment, where the customer segment delivers, services and distributes energy to customers, while the generation segment is involved in the business of selling electricity to the wholesale electricity market and the customer segment.

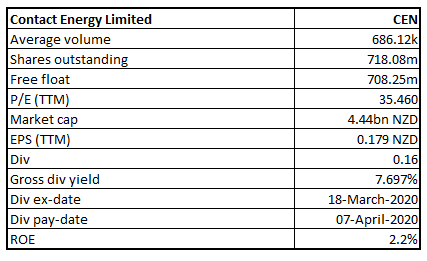

CEN Details

Investment Summary:

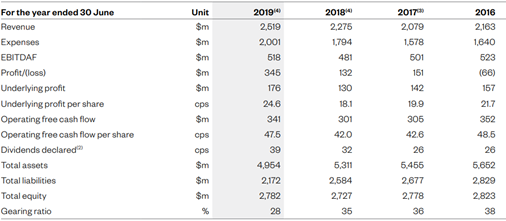

Utilities to Remain in Demand Irrespective of Situation: Contact Energy Limited (NZX: CEN) is involved in electricity generators and digital retailing for the residents of New Zealand. The market capitalisation of the company stood at around $4.44 billion as on May 4, 2020. Looking at the past performance over FY16 to FY19, total revenue of the company has grown at a CAGR (compounded annual growth rate) of ~5.21%. The company’s total revenue improved from $2,163.0 million in FY16 to $2,519.0 million in FY19, and net income improved from a loss of $66.0 million in FY16 to a profit of $345.0 million in FY19.

The first half period of FY20 highlighted important points such as average electricity tariffs for customers were lower than last year despite increases in wholesale electricity costs. There was constructive participation by the company in the Electricity Price Review to ensure delivery of reliable, low-carbon electricity for New Zealanders. The period also witnessed accelerated work programme by Transpower (co-funded) to help move renewable electricity generation north in the event of a disorderly Tiwai Point smelter exit. The company remained focused on delivering on its transformation programme to reduce controllable costs, and capture value from scale efficiencies through geothermal development and leveraging its customer systems and lean operating model.

Historical Financial Performance (Source: Company Reports)

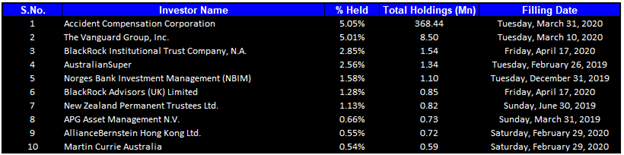

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 21.21% of the total shareholding. Accident Compensation Corporation and The Vanguard Group, Inc. hold maximum interests in the company at 5.05% and 5.01%, respectively.

Top 10 Shareholders (Source: Refinitiv (Thomson Reuters))

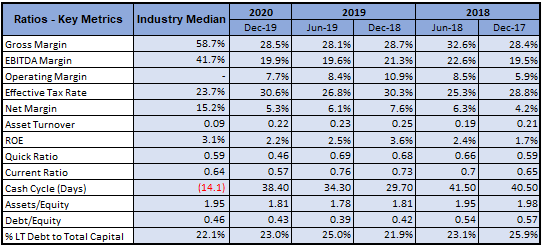

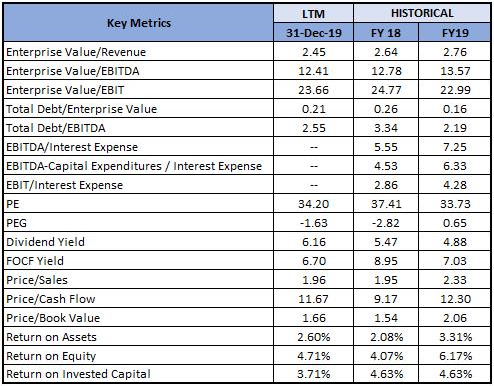

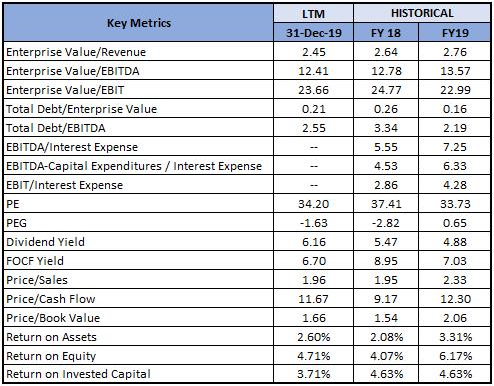

A Quick Look at Key Metrics: Its gross margin and EBITDA margin for H1FY20 stood at 28.5% and 19.9%, better than H2FY19 result of 28.1% and 19.6%, respectively. Its Debt to Equity ratio for H1FY20 stood at 0.43x, lower than the industry median of 0.46x, depicting reasonable leverage position of the company.

Key Metrics (Source: Refinitiv (Thomson Reuters))

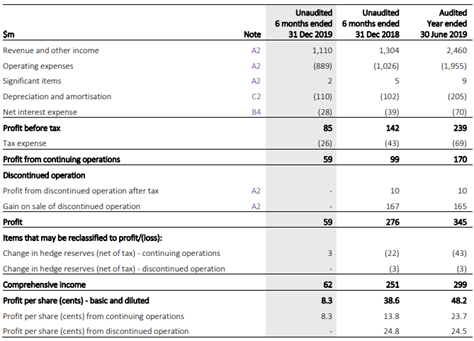

Subdued First Half Performance for FY20: The company reported statutory profit for the first half period of FY20 (ended on December 31, 2019) at $59 million, a decrease of $217 million than the previous corresponding period (pcp) that included Rockgas profit of $10 million and $172 million gain on the sale of both Rockgas and Ahuroa gas storage. EBITDAF from continuing operations for the period was reported at $221 million, a decline of 21% on the pcp, mainly due to rising thermal generation costs, lower sales to commercial and industrial customers and strong financial performance under unique wholesale market conditions in the prior period. Operational improvements and portfolio changes resulted in a decline of other operating costs of $8 million, down 7% on a year ago. Operating free cash flow for the first half period declined by 39% (on pcp) to $120 million, mainly due to a combination of lower operating earnings (EBITDAF), partially offset by lower stay in business capital expenditure and interest costs.

Cash tax for the period stood at $56 million, an increase of $15 million on pcp, reflecting tax payable on the strong profit realised in FY19. The Board of Directors approved an interim ordinary dividend of 16 cents per share (imputed up to 10 cents per share for qualifying shareholders), with payment date on April 7, 2020. CEN expects for the full year ordinary dividend of 39 cents per share. Operational performance within its customer business witnessed demand for its broadband and energy bundles surpassing even its most optimistic forecasts with more than 17,000 new broadband connections over the past 12 months, giving the rise of confidence around its transformation into a customer-centric digital energy company. Despite strong operational performance on many metrics and underlying efficiency improvements of 6%, EBITDAF in the customer business declined by 38% (y-o-y) to $30 million, as rising input costs for electricity, gas, carbon and distribution networks were not recovered.

Under wholesale business, the company reported decline in EBITDAF by $39 million (y-o-y) to $204 million, as production from hydro generation declined by 8%. Further, there was an increase in thermal generation costs by 10%, driven by gas, carbon and gas storage facility costs.

H1FY20 Income Statement (Source: Company Reports)

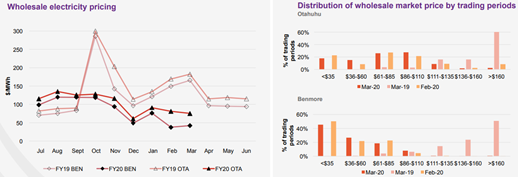

Overview of Recent Updates: On April 16, 2020, the company provided monthly operating report for March 2020, where it highlighted that, under its customer business, mass market electricity and gas sales stood at 310 GWh, as compared to 287 GWh in the previous corresponding period (pcp). The mass market electricity and gas netback stood at $92.71/MWh, as compared to $88.06/MWh in the pcp. Under wholesale business, contracted Wholesale electricity sales, including that sold to the Customer business, stood at 577 GWh, as compared to 814 GWh in pcp. The electricity and steam net revenue for the period stood at $87.29/MWh, as compared to $82.52/MWh in the pcp. Electricity generated (or acquired) for March 2020, was reported at 672 GWh, as compared to 853 GWh in the pcp. The unit generation cost, which includes acquired generation stood at $25.90/MWh, as compared to $41.18/MWh in the pcp, where its own generation cost in the month stood at $25.14/MWh, lower than the pcp at $32.17/MWh.

Wholesale Market Pricing Data (Source: Company Reports)

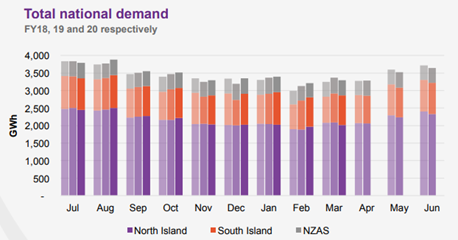

Under the electricity demand, New Zealand electricity demand declined by 2.0% on March 2019, while there was improvement of 0.7% on March 2018. Cumulative 12 months demand for April 2019 to March 2020, stood at 41,746 GWh, an improvement of 0.6% on the prior comparative period.

Total National Demand Data (Source: Company Reports)

On May 4, 2020, CEN highlighted that the Clutha-Upper Waitaki Lines Project (CUWLP) work programme is expected to get delayed from its targeted commissioning date of June 2022, because national grid operator Transpower will not be funding work to accelerate the CUWLP transmission build in the lower South Island beyond the $10 million which was committed by Contact and Meridian Energy in December 2019. The company, while reiterating that it would not make additional financial contribution, gave to understand that it would continue to work with Transpower and look after all the aspects to reduce the delay in the work as the goal is to move towards renewable electricity generation in the lower South Island north as soon as possible.

Key Risks: The company is susceptible to certain risks such as climate change and the transitional risks including regulatory changes, consumer behavioural shifts and wider societal responses.

What to Expect: As per the release, the company highlighted that the Rio Tinto-initiated strategic review of the Tiwai aluminium smelter remained firmly on the radar, whose disorderly exit would be a poor outcome for New Zealand. CEN is actively engaged in negotiations for revised terms for electricity supply to Tiwai. Additionally, the company is also executing on a range of mitigation options, including co-funding an accelerated work programme by Transpower, which will help move renewable electricity generation in the lower South Island north through the national transmission network, if the smelter review leads to curtailment or closure.

Contact energy is working with commercial and industrial customers to deliver reductions to their carbon footprints by connecting them with low-carbon, reliable electricity, underpinned by signing of long-term 13 MW renewable agreement.

Key Valuation Metrics (Source: Refinitiv (Thomson Reuters))

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation

EV/EBITDA Multiple Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Technical Overview:

Weekly Chart:

Source: Refinitiv (Thomson Reuters)

Note: Note: Purple colour lines are Bollinger Bands, yellow lines are retracement lines and orange colour dotted line is Parabolic SAR.

The stock came under intensified selling pressure from its recent high of $7.73, resulting into low of $4.50. From the low, the stock retraced up, surpassing 61.8% retracement level of $6.50. But the stock could not hold on bullish momentum and fell from there and gave close around 50% retracement level, a week ago the prior week. In the prior week, the stock again moved up close to 61.8% retracement level and gave higher close. In 1st trading session of the current week, the stock has traded with little volatility wherein it opened around the previous week close and gave closure around 50% retracement level at $6.19.

Technical indicators such as MACD with bearish cross-over and RSI with around 42 reading suggest softer momentum for the stock.

Going forward, the stock is likely to find good resistance around $6.70, as provided by 20 period SMA on the chart whereas on further retreating of prices, the stock would have good support at $6.00.

Stock Recommendation: The company’s operations have been deemed as ‘essential services’ amidst lockdown measures to restrict the spread of Covid-19. It aims to drive reductions in costs and deliver strong returns to shareholders at the same time as it develop a large-scale consented geothermal development at Tauhara, which will help reduce the nation’s carbon emissions, backed by its world-class geothermal capability and strong balance sheet.

Considering the aforesaid facts, recent updates and H1FY20 results, we have valued the stock using EV/EBITDA Multiple Based Relative Valuation (on an illustrative basis) and we have arrived at a target price of higher single-digit growth (in % terms).

Hence, we give a “Buy” recommendation on the stock at the current market price of NZ$6.190 per share, down by 2.21% on May 4, 2020.

.png)

CEN Daily Technical (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...