Company Overview: Energy generator and digital retailer, Contact Energy Limited (NZX: CEN) is involved in providing electricity, natural gas and liquefied petroleum gas (LPG), along with broadband services. The electricity is generated via thermal, hydro, and geothermal sources. CEN operates the business through two segments which are Customer segment and Generation segment. The Customer segment is involved in delivering, servicing and distributing energy to customers. It sells gas, LPG products and electricity, and services to small business, residential, commercial and industrial customers. The Generation segment is engaged in the business of selling electricity to the wholesale electricity market and to the Customer segment. The Company's stations include Ohaaki, Poihipi and Te Rapa in Waikato, Te Huka and Te Mihi in Taupo Wairakei in Taupo, and Whirinaki in Hawke’s Bay along with Ahuroa and Stratford in Taranaki. CEN is also engaged in the development of geothermal energy projects.

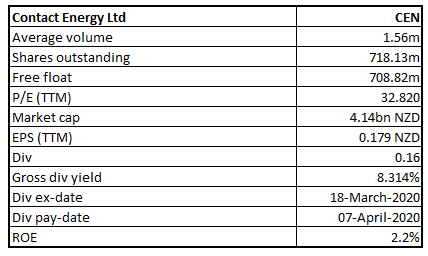

CEN Details

Investment Summary:

Power Consumption is Expected to Rise as Business Activities Resume: Contact Energy Limited (NZX: CEN) is a New Zealand-based energy company with a diverse mix of assets to maintain a reliable, affordable as well as environmentally sustainable electricity supply for NZ. It also has strong presence in wholesale gas distribution, gas retailing and electricity retailing. It has a market capitalization of ~$4.14 billion as on July 27, 2020.

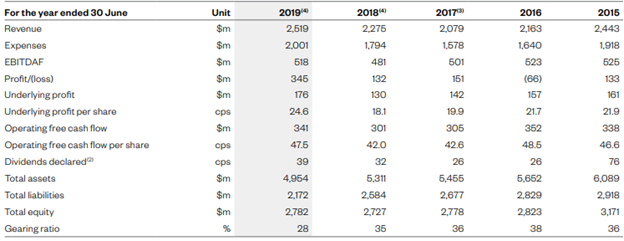

Looking at the past performance over FY15 to FY19, bottom line of the company witnessed a compounded annual growth rate (CAGR) of ~27%. The company’s net income improved from $133 million in FY15 to $345 million in FY19.

The company is currently executing various mitigation options to help move renewable electricity generation in the lower South Island north through the national transmission network and it is also working with commercial and industrial customers to deliver reductions to their carbon footprints by connecting them with low-carbon, reliable electricity.

Historical Financial Performance (Source: Company Reports)

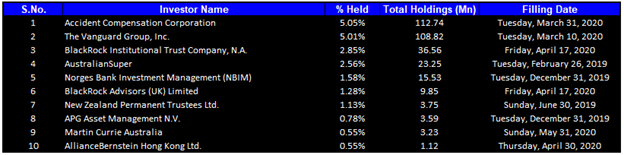

Top 10 Shareholders: The top 10 shareholders have been highlighted in the below table:

Top 10 Shareholders (Source: Refinitiv (Thomson Reuters))

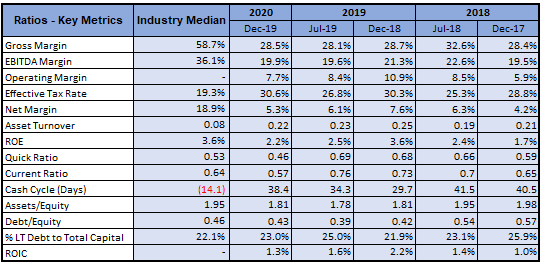

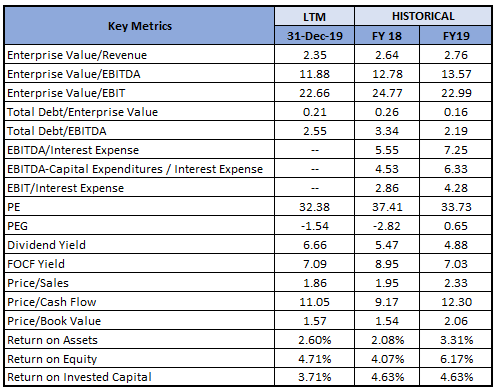

A Quick Look at Key Metrics: Its gross margin and net margin for H1FY20 stood at 28.5% and 19.9%, better than the H2FY19 result of 28.1% and 19.6%, respectively, implying improvement in operating efficiency of the company. Its Debt to Equity ratio for H1FY20 stood at 0.43x, lower than the industry median of 0.46x, depicting reasonable leverage position of the company.

Key Metrics (Source: Refinitiv (Thomson Reuters))

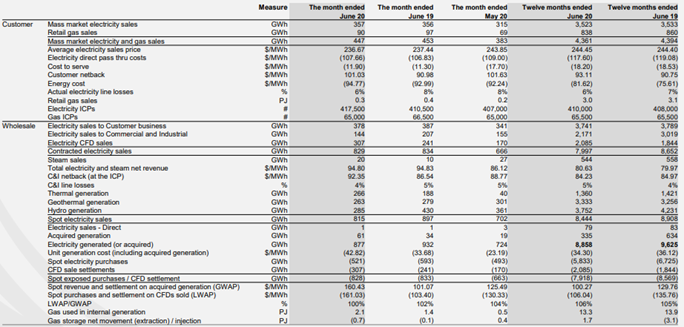

June 2020 Operational Performance: Under the Customer business, Mass market electricity and gas sales stood at 447 GWh (June 2019: 453 GWh), and Mass market electricity and gas netback stood at $101.03/MWh (June 2019: $90.98/MWh). Under the Wholesale business, Contracted Wholesale electricity sales, including that sold to the Customer business, totalled 829 GWh (June 2019: 834 GWh); Electricity and steam net revenue stood at $94.80/MWh (June 2019: $94.83/MWh) and Electricity generated (or acquired) stood at 877 GWh (June 2019: 932 GWh). The unit generation cost, which includes acquired generation was $42.82/MWh (June 2019: $33.68/MWh).

June 2020 Operational Data Metrics (Source: Company Reports)

As on July 9, 2020, South Island controlled storage was 77% of mean, as compared to 78% as on June 30, 2020. North Island controlled storage was 70% of mean, as compared to 73% as on June 30, 2020. Total Clutha scheme storage (including uncontrolled storage) was 63% of mean. Inflows into Contact’s Clutha catchment for June 2020 were 93% of mean.

Data on Electricity Demand (Source: Company Reports)

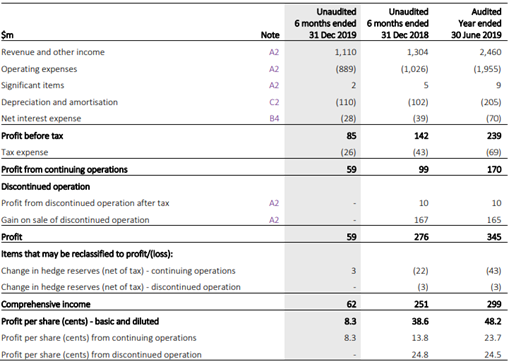

Subdued H1FY20 Financial Performance: The company reported operating earnings (EBITDAF) of NZD 221 million for the first half of FY20 (ended December 31st, 2019), down by 21% on the previous corresponding period (pcp), due to rising thermal generation costs, lower sales to commercial and industrial customers and strong financial performance under unique wholesale market conditions in the prior period. Further, the company reported profit of NZD 59 million, down 40% on pcp.

During the period, the average electricity tariffs for customers were lower than last year, despite increases in wholesale electricity costs. Operating free cash flow for 1H20 was NZD 120 million, down 39% on pcp, due to a combination of lower operating earnings (EBITDAF), partially offset by lower stay in business capital expenditure and interest costs.

EBITDAF in the Wholesale business reduced by NZD 39 million to NZD 204 million year-on-year, as production from hydro generation was down by 8%. Despite strong operational performance on many metrics and underlying efficiency improvements of 6%, EBITDAF in the Customer business was down NZD 18 million year-on-year to NZD 30 million, as rising input costs for electricity, gas, carbon and distribution networks were not recovered.

The company declared an interim ordinary dividend of NZ 16 cents per share, in line with the dividend paid in the pcp.

H1FY20 Income Statement (Source: Company Reports)

A Look at Key Updates: The company recently made two changes to its leadership team with the appointment of James Kilty as Deputy Chief Executive Officer and Jacqui Nelson as Chief Generation Officer. James has a unique set of skills, capabilities, and over 20 years of experience in energy markets, operations and development and will provide strong leadership. Jacqui has been with Contact for more than 15 years in a wide range of roles across finance, resource management, trading and most recently as General Manager of Operations.

In another update, the company stated that Rio Tinto’s intention to effectively close New Zealand’s Aluminium Smelter (NZAS) by giving 14 months’ notice on their electricity contract with Meridian Energy was “very disappointing”. With the disorderly exit of Rio Tinto which has been consuming about 13% of electricity generated, there would be ripple effect on the entire energy sector as the closure means cheaper power. Contact Energy has initiated mitigation plans to minimize the financial impact.

What to Expect: The company is focused on delivering on its transformation programme to reduce controllable costs, and capture value from scale efficiencies through geothermal development and leveraging its customer systems and lean operating model. In FY20, the company expects cash spend to be in between NZD 255 million- NZD 265 million. Further, it targets to pay a total dividend of 39 cents per share in FY20.

Utility Sector Outlook: The power sector is united to decarbonise transport and accelerate the electrification of South Island industry away from a reliance on coal. NZAS has subsidised transmission costs to consumers for years. Not only will those costs now fall to other customers, there will also be additional costs for the significant transmission investment from Transpower now needed to shift surplus energy from the lower South Island north to where it is needed. In the meantime, the surplus water currently being used to generate renewable energy in Southland will in large part end up flowing down the Clutha River.

Key Risks: The company is exposed to certain financial risks like market risk, liquidity risk as well as credit risk. Exit of NZAS from New Zealand poses risk of uncertainty of reduction in demand and, therefore, leading to shrink in margins. Best way to mitigate the challenge is to optimize the operation and promote awareness towards utilizing of green energy.

Key Valuation Metrics (Source: Refinitiv (Thomson Reuters))

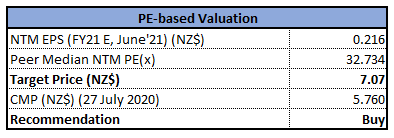

Valuation Methodology: Price to Earnings (P/E) Multiple Based Relative Valuation (Illustrative)

Price to Earnings (P/E) Multiple Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands with upper band suggesting overbought status while lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack.

The stock has given weaker close for the first trading day of the on-going week. Going by chart formation, two consecutive weeks of Hammer formation should have been bullish reversal and hence we consider softer close to be a minor deviation and the stock to resume uptrend shortly. Technical indicator RSI with 41 reading suggests neutral momentum for the stock.

Going forward, the stock may have resistance around the intersecting point of 50% retracement level and the upper Bollinger band of $6.80 while support could be around 23.6% retracement level of $5.60.

Stock Recommendation: The company is accelerating its mitigation plans to minimise the financial impact from the effect of COVID-19 and exit of NZAS. Portfolio of long-life renewable generation assets, flexible thermal assets and fuel contracts, and strong balance sheet places the company in a comfortable position even in a lower demand environment.

Considering the aforesaid facts, recent updates and H1FY20 results, we have valued the stock using Price to Earnings (P/E) multiple based relative valuation (on an illustrative basis) and we have arrived at a target price of lower double-digit growth (in % terms).

Hence, we give a “Buy” recommendation on the stock at the current market price of NZ$5.760 per share, down by 1.71% on July 27, 2020.

.png)

CEN Daily Technical Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...