Sector Landscape

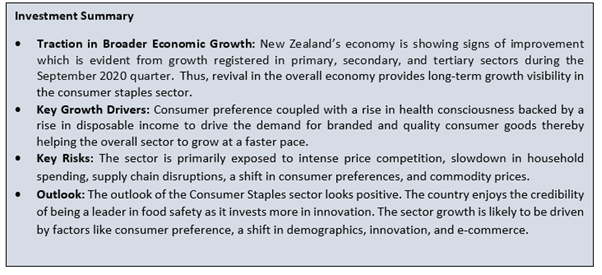

The consumer staples sector deals in essential items that are in constant demand and demand for the same remains relatively stable over time. It continues to be one of the prominent wealth generating sector of New Zealand. This sector falls under the ambit of the country’s primary sector and includes mix of businesses such as dairy, meat & wool, forestry, horticulture, seafood, arable, processed foods, among others. As per an economic update provided by the Ministry for the Primary Industries December 2020, export revenue for the year ending June 2021 is forecasted to fall by 1.0% to $47.5 billion due to appreciating NZD and a lower outlook for meat and wool, dairy, and seafood due to COVID-19 related challenges. However, export revenue has been forecasted to increase by 3.6% to $49.2 billion in 2022. Thus, the sector is quite resilient as there has been an improvement in the overall economic growth environment. Of the overall GDP improvement in September 2020 quarter, the primary industries registered a growth of 4.6% during the period as visible in the Exhibit 1 below.

Exhibit 1: Sectoral Performance in September 2020 Quarter

Data Source: Stats NZ; Chart Created by Kalkine Group

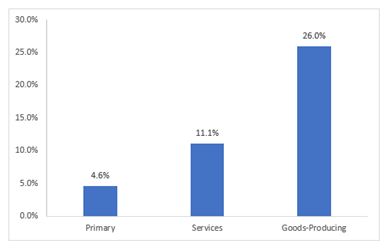

Although the primary sector witnessed a slower growth as compared to other broader sectors of the economy in the September 2020 quarter, the industries among the primary sector did not fall by as much in the June 2020 quarter. The uptick in the sector was driven by mining and forestry during September 2020 quarter which was up by 16.1% and 23.2%, respectively, unlike agriculture, forestry was not deemed essential during the alert level 4 lockdown as reflected in Exhibit 2 below.

Exhibit 2: GDP by Industry (change from June 2020 - September 2020)

.png)

Data Source: Stats NZ; Chart Created by Kalkine Group

Note: Seasonally Adjusted Chain Volume Series in 2009/2010 prices

Key Growth Drivers

Some of the key growth drivers for the consumer staples sector have been highlighted below: -

Consumer Staples Sector: A Key Economic Growth Driver

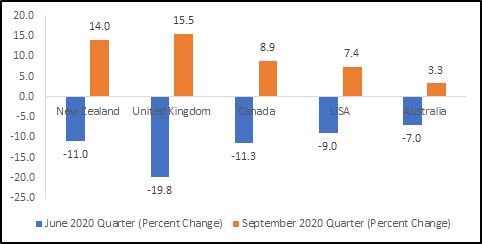

The Consumer Staple sector is part of the broader primary sector accounting for about 46% of all goods and services exports thereby contributing hugely to New Zealand’s economic growth. With the prevailing Covid-19 pandemic having taken a toll on the global economy, New Zealand’s economy is no exception as the national GDP shrunk by 11% in June 2020 quarter. Following the gradual easing of restrictions by the government, the New Zealand economy has started showing signs of resilience with the latest September 2020 GDP figures suggesting rebound in the economy. GDP witnessed a sharp rebound of 14% in the September 2020 quarter as against a revised figure of 11% in the June 2020 quarter, as is reflected in Exhibit 3 below. This marked the strongest quarterly growth in GDP on record in New Zealand due to the benefit of fewer restrictions on activity in the September 2020 quarter. Although on annualised basis, GDP shrunk 2.2% for the year ended September 2020, it looks impressive following a record fall in the June 2020 quarter.

With the easing of restrictions worldwide, a significant rebound in economic activities have led to a rebound in GDP across many countries.

Exhibit 3: GDP Movement in Major Economies (% quarter-on-quarter)

Data Source: StatsNZ, Analysis by Kalkine Group

Change in Consumer Preference Amidst Rising Disposable Income Augurs well for Growth

The demand of the consumer staples sector has also been driven by the change in consumer preference and increase in disposable income. There has been a rise in demand for organic and healthy food by more health-conscious consumers. Due to the competitive intensity in the sector, the companies are really focused towards creating product differentiation by bringing about certain qualitative changes in their products. With the lifting of Covid-19 related restrictions and resultant improvement in economic activities, consumer spending is likely to receive a big boost, going ahead, benefitting from increased employment and disposable income which will eventually be driving discretionary spending. Notably, this has been reflected in the improvement in New Zealand’s Real gross national disposable income (RGNDI), which measures the real purchasing power of the country’s disposable income and has registered a growth of 13.9% in the September 2020 quarter.

Key Risks and Challenges

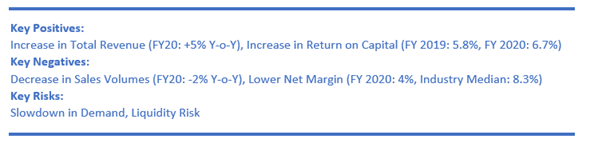

Exhibit 4: Key Risks and Challenges

.png)

Source: Kalkine Group

Increase in Investment Spending

Household spending has been a major contributor to the consumer staples sector. As a fall-out of adverse economic conditions in the face of Covid-19, there was cut back in discretionary spending by households and it was more directed towards value buying. However, the household spending is showing signs of improvement with the country’s household spending increasing by 14.8% in the September 2020 quarter across all expenditure categories and the durables, non-durables, and services was up significantly over the quarter.

Revival in Global Economic Growth

The country’s consumer staples sector also hinges on exports and the ongoing border restrictions has adversely impacted the export earnings. Further, increasing trade barriers is also creating supply-side risk. With the global economies gradually recovering from the initial setback of Covid-19, there has been easing of pressure on the supply side which brightens the long-term growth prospects of the sector. The country’s export sector has started to witness a rebound in activities that was visible from the uptick in the country’s overall exports which grew by 4.9% in the September 2020 quarter, supported by an increase of 6.4% in goods exports which included metal products, machinery, and equipment; agriculture and fishing primary products; meat products; and forestry primary products.

Increased Level of Competition

The sector has also been overburdened by the impact of intense competition, resulting in the lowering of product prices in an increased cost environment. Due to the higher competitive intensity in the market, the companies resort to higher branding and marketing of their products, thus adversely affecting the margins of the companies in the sector. Further, change in consumer preference towards modern retail which is disrupting traditional retail channels also remains a cause of concern. Companies in the sector need to be nimbler to innovate and focus on quality to create a niche in the space and enjoy a competitive advantage.

Outlook

The sector is now gradually recovering from the impact of Covid-19 that has dealt blow to the country’s consumer staples sector which was already feeling the pinch of slowing discretionary demand. This is evident from the recent rebound in the overall primary sector. Significant liquidity infused by the government into the economy and other kinds of stimulus provided to revive business activities in the country bodes well for the sector in the long run. Further, this will aid in boosting discretionary spending as well as household spending and resultantly lift in consumer demand in the long run. Moreover, with the increasing level of the educated labour force, and nuclear family penetration, one can easily bet that the growth prospects are brighter for the sector.

The support of the government liquidity measures and revival in the economy has also started to bear fruit as witnessed from the improvement in the household spending that increased by 14.8% in the September 2020 quarter across all categories and the consumer staples sector is not an exception. Additionally, with the lifting of most of the COVID-19 related restrictions in the country, business activities have resumed which has had a positive impact on employment generation. Further, the wage subsidies provided by the government helped companies to retain their employees. Wage subsidy along with schemes directly benefitting people prevented steeper fall in consumer demand during the lockdown periods.

Apart from the sector-specific factors, we have also analyzed four NZX-listed companies operating in the consumer staple sector. This report covers insights, outlook, performance, and potential to deliver in the near to medium term.

1. Fonterra Co-operative Group Ltd (Recommendation: Buy, Potential Upside: High Single Digit), (M-Cap: $7.08 billion, Gross Dividend Yield: 1.147%)

Business Description:

Fonterra Co-operative Group Ltd (NZX: FCG) is a multinational dairy company, which is owned by 13,000 NZ dairy farmers.

Outlook

To speed up demand for the foodservice products in the US, FCG has entered a sales and marketing agreement with one of America’s leading dairy co-operatives, Land O’Lakes, Inc.

The company stated that COVID-19 related challenges are still there, including how the global recession as well as new waves of the virus would be impacting customer demand, and there happens to be some congestion in the global supply chains that the company is actively managing.

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack. https://www.bollingerbands.com/

The ongoing week is going to be the fourth consecutive week wherein the stock would have given flattish closed at $4.39 suggesting a great deal of indecisiveness on the part of traders on the stock. The technical indicator RSI with a reading around 63 but with a flattish curve at the end suggests flattening of bullish momentum.

Going forward, if present indecisiveness gives the way to upside movements, then the stock will have resistance around the previous high of $4.72 while, on the price retreating, it will have support around the 38.2% retracement level of $4.21.

Considering the technical analysis and increase in total revenue, we give a “Buy” rating on the stock at the current market price of $4.390 per share, up by 0.69% on January 7, 2021.

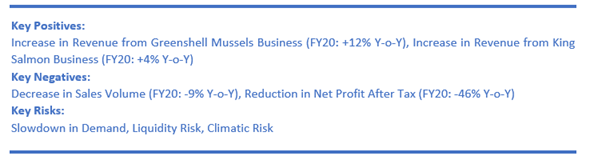

2. Sanford Ltd (Recommendation: Buy, Potential Upside: Low Double Digit), (M-Cap: $476.8 million, Gross Dividend Yield: 1.362%)

Business Description:

The vision of Sanford Ltd (NZX: SAN) is to become the best seafood company in the world. While the company holds 23% of the country’s quota, it has 49 vessels and 210 aquaculture farms.

Outlook

The company has earmarked Capex level to be in the range of $45 million to $55 million in FY21. It also has a robust product innovation pipeline in place to cater to the requirements of high value customer trends. Further, lifting of COVID-19 related restrictions will translate into increased business activities and resultant rebound in the hospitality industry more specifically, in food industry on whom the seafood industry relies the most.

With a gearing of 30.6% at the end of September 2020, the company is possessing robust balance sheet which might help moving forward.

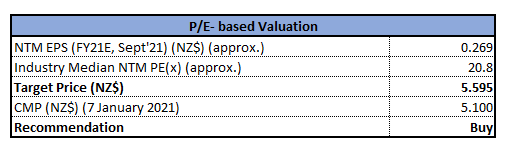

Valuation Methodology: P/E Based Relative Valuation (Illustrative)

P/E Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

We have applied P/E Based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms).

Considering the expected upside and robust balance sheet, we give a “Buy” rating on the stock at the current price of NZ$5.100 per share on January 7, 2021.

3. Livestock Improvement Corporation Ltd (Recommendation: Hold, Potential Upside: Low Double Digit), (M-Cap: $102.89 million, Gross Dividend Yield: 21.861%)

Business Description:

Livestock Improvement Corporation Ltd (NZX: LIC) is a farmer-owned co-operative having offices in the United Kingdom, Ireland and Australia. It provides range of services as well as solutions to improve the productivity and prosperity of the farmers.

Outlook

The company is expecting FY21 underlying earnings to be in the range of $16 million - $22 million. With the company continuing to increase investments on R&D that stood at $16 million, an increase of 17.5% YoY equating to 6.3% of revenue also bodes well for the company going ahead. LIC has a strong balance sheet with miniscule debt which could help the company moving forward. The investment towards R&D allows the company to give farmers numerous tools in the future to further improve genetic gain as well as address environmental challenges.

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack. https://www.bollingerbands.com/

The stock gave a gap up opening at $0.81 for the ongoing week but closed without any changes in its prices – a classic case of 4 Price Doji. The technical indicator RSI with a reading around 61 and a curve at the end pointing up, suggests strong bullish momentum.

Going forward, the stock may have resistance around the previous high of $0.90 whereas support could be around $0.79.

Considering the technical analysis and growth in total revenue, we give a “Hold” rating on the stock at the current price of $0.810 per share on January 7, 2021.

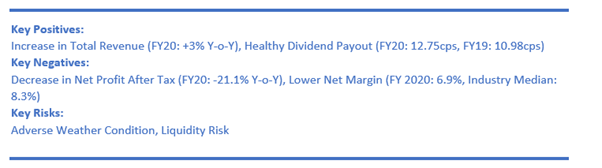

4. PGG Wrightson Ltd (Recommendation: Hold, Potential Upside: Low Double Digit), (M-Cap: $252.87 million, Gross Dividend Yield: 3.834%)

Business Description:

PGG Wrightson Ltd (NZX: PGW) happens to be an agricultural services business which operates throughout NZ. The company offers an extensive range of products as well as a full-service offering, complimented with the knowledge and expertise of the people, to the rural sector.

Outlook

The company has recently announced that it is well positioned to post an operating EBITDA result of ~$57 million (or ~$35 million excluding the impact of the new lease accounting standard). It was also added that achievement of this result would be representing a circa 27% improvement on the prior year on the NZ IFRS 16 inclusive basis (or the circa 50% improvement excluding the NZ IFRS 16).

The company witnessed a pleasing first 5 months of the financial year with the business trading well as well as surpassing the expectations. There was robust demand in Rural Supplies as well as Fruitfed Supplies retail businesses over the crucial spring period.

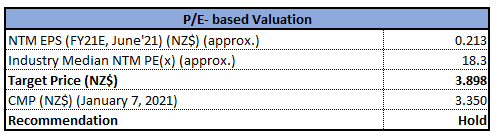

Valuation Methodology: P/E Based Relative Valuation (Illustrative)

P/E Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

We have applied P/E Based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms).

Considering the expected upside and improvement in net margin, we give a “Hold” rating on the stock at the current price of $3.350 per share, up by 2.76% on January 7, 2021.

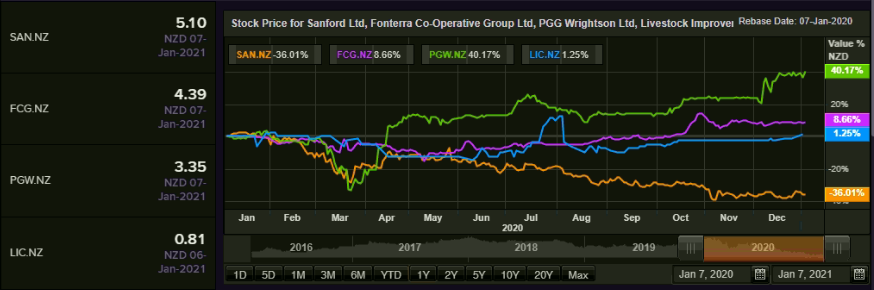

Comparative Price Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...