This report is an updated version of the report published on 16 June 2025 at 2:47 pm AEST.

Company Overview: Nido Education Limited (ASX: NDO), an Australian company, specializes in owning, operating, and managing long-term early childhood education and care services. It provides a nurturing, secure, and serene environment for children from six weeks old up to school age. The company operates under the Nido Early School brand, delivering high-quality education and care. Maas Group Holdings Limited (ASX: MGH) is an Australian company that provides construction materials, equipment, and services providers with diversified exposures across the civil and infrastructure market. Kalkine’s Market Event Report covers the Investment Summary, Event Summary, Data Insights & Analysis, Key Financial Metrics, Risks, Outlook, Technical Analysis along with the Valuation, Target Price, and Recommendation on the stock.

Investment Summary

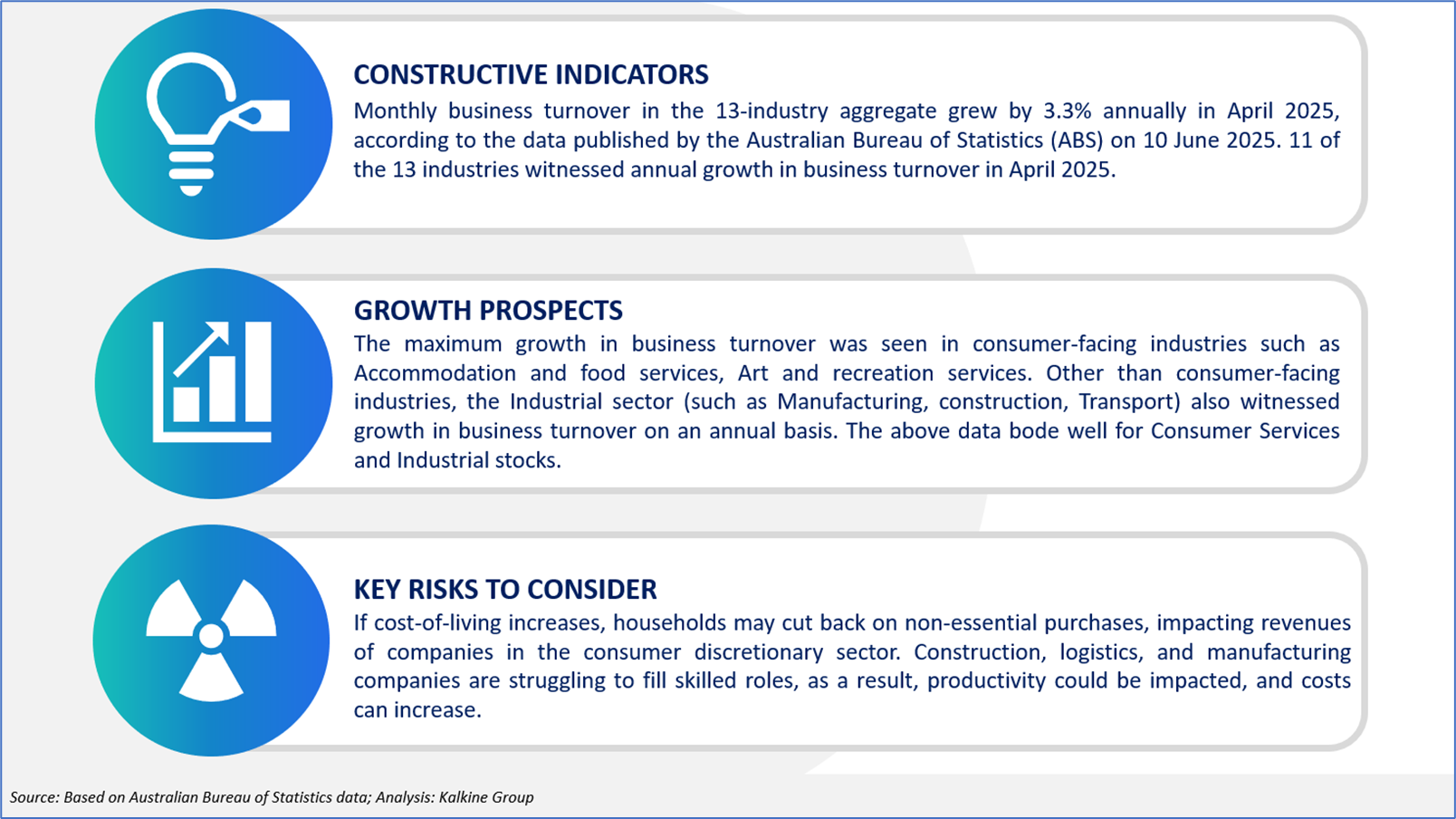

Event Highlights

Data Insights and Analysis

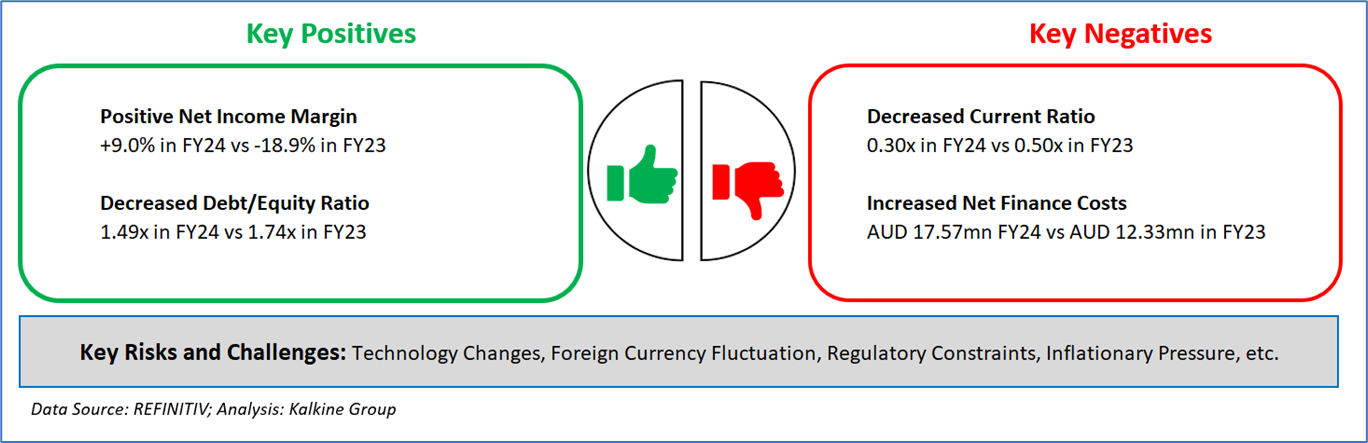

Key Drivers versus Key Challenges

Based on the above data, two ASX stocks have been identified to showcase the momentum.

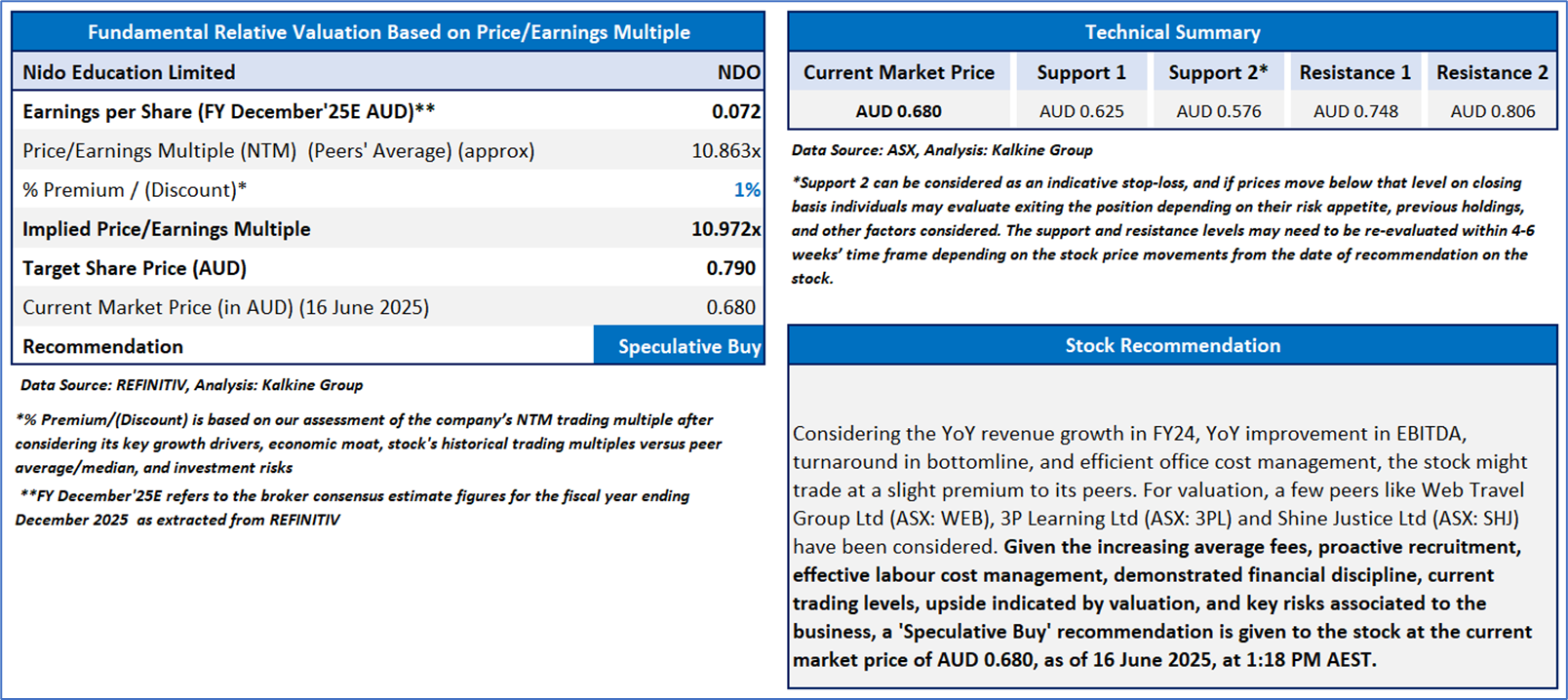

1) Nido Education Limited (ASX: NDO) (Recommendation: ‘Speculative Buy’ at AUD 0.680, Potential Upside: Low Double-Digit) (M-cap: AUD 161.76mn)

Company Overview: NDO, an Australian company, specializes in owning, operating, and managing long-term early childhood education and care services. It provides a nurturing, secure, and serene environment for children from six weeks old up to school age. The company operates under the Nido Early School brand, delivering high-quality education and care.

12-month ended 31 December 2024 Financial Year (FY24) Financial Performance: Revenue from ordinary activities jumped 75.2% YoY, reaching AUD 163.63mn in FY24, up from AUD 93.37mn in FY23. This growth was primarily driven by an 81% increase in service revenue during the period. Furthermore, service EBITDA turned positive, recording AUD 42.27mn in FY24, up from a negative AUD 2.66mn in FY23. Consequently, the company's statutory profit from ordinary activities after tax also turned positive to AUD 14.65mn in FY24, compared to a loss of AUD 18.11mn in FY23.

Recent Update: NDO has reported the on-market repurchase of 18,065 fully paid ordinary shares, effective 16 June 2025.

Outlook: NDO's proactive stance and strategic market placement establish a firm basis for sustained success. The forthcoming alterations to the childcare subsidy activity test, alongside prospective policy adjustments, are anticipated to generate novel growth opportunities. Management believes, the company is well positioned to address the requirements of families and consistently generate value for its stakeholders.

The stock has witnessed a correction of ~16.36% in last nine months, and over the past one year, it has decreased by ~23.33%. The stock has a 52-week low and 52-week high of AUD 0.680 and AUD 0.920, respectively, and is currently trading near its 52-week low. NDO was last covered in a report dated ‘05 May 2025’.

2) Maas Group Holdings Limited (ASX: MGH) (Recommendation: ‘Hold’ at AUD 4.230, Potential Upside: Low Single-Digit) (M-cap: AUD 1.54bn)

Company Overview: MGH is an Australian company that provides construction materials, equipment, and services providers with diversified exposures across the civil and infrastructure market.

6-month ended 31 December 2024 (1HFY25) financial performance: In the first half of FY25, revenues from ordinary activities for the company saw a modest increase of 0.27% YoY, reaching AUD 473.94mn up from AUD 472.65mn in 1HFY24. This growth was primarily assisted by higher sales in concrete, asphalt, quarry products, and land inventory. However, Underlying EBITDA experienced a slight decline of 2.16% YoY, settling at AUD 95.01mn down from AUD 97.11mn in 1HFY24. Consequently, profit from ordinary activities after tax, attributable to the owner, decreased by nearly 7.5% YoY to AUD 31.33mn compared to AUD 33.85mn in 1HFY24.

Recent Update: On 5 June 2025, MGH announced that its existing construction materials operations are well-positioned to leverage economic growth, with significant capacity for further expansion. The company's recent acquisitions of R&C (asphalt paving) and CER (recycling) have also enhanced its integrated Melbourne Hub, providing more growth avenues.

Outlook: MGH reaffirmed its FY25 underlying EBITDA guidance of AUD 215 - 245mn. It expects asset recycling to contribute over AUD 100mn. Going forward, MGH would concentrate its capital and growth initiatives on Construction Materials, as it continues to simplify its overall group structure. The company also expects to selectively pursue M&A opportunities to enhance its organic expansion.

The stock has decreased by ~10.62% in last six months, and over the last nine months, it is down by ~9.27%. The stock has a 52-week low and 52-week high of AUD 3.300 and AUD 5.050, respectively and is currently trading above the 52-week high-low average. MGH was last covered in a report dated ‘12 May 2025’.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and geopolitical tensions prevailing. Therefore, it is prudent to follow a cautious approach while investing.

Note 1: Past performance is neither an Indicator nor a guarantee of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance levels is 16 June 2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual’s appetite for upside potential, risks, holding duration, and any previous holdings. An ‘Exit’ from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Kalkine reports are prepared based on the stock prices captured either from REFINITIV or Trading View. Typically, REFINITIV or Trading View may reflect stock prices with a delay which could be a lag of 25-30 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.

Technical Indicators Defined: -

Support: A level at which the stock prices tend to find support if they are falling, and a downtrend may take a pause backed by demand or buying interest. Support 1 refers to the nearby support level for the stock and if the price breaches the level, then Support 2 may act as the crucial support level for the stock.

Resistance: A level at which the stock prices tend to find resistance when they are rising, and an uptrend may take a pause due to profit booking or selling interest. Resistance 1 refers to the nearby resistance level for the stock and if the price surpasses the level, then Resistance 2 may act as the crucial resistance level for the stock.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer This report has been issued by Kalkine New Zealand Limited (FSP691351) (NZBN:9429047678101) (“Kalkine”). Kalkine is a Financial Advice Provider (“FAP”) and is authorised by a Class 1 Financial Advice Provider Licence issued by Financial Markets Authority (“FMA”) to provide financial advice. Kalkine provides only general financial advice through its research reports following a person becoming a member. The reports contain buy/sell/hold and other recommendations in relation to equity securities, managed funds and other managed investment schemes and other financial advice products. The recommendations and opinions in this report and on Kalkine website do not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions. If you act on the advice in the research reports, you may have to pay fees, expenses or other amounts (but not to Kalkine). Further information about the complaints and dispute resolution process, as well as information about Kalkine’s duties are available on Kalkine’s website. Please read our Financial Advice Provider (FAP) disclosure statement and Complaints Handling Guide, which are available on the website.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...