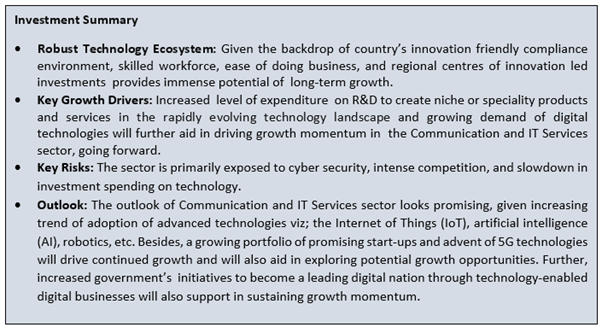

Sector Landscape

New Zealand’s Information and Communications Technologies (ICT) sector is one of the major contributors to the country’s economic growth. The sector is more diversified with its services spread across wireless infrastructure, health IT, digital content, payments, geospatial, telecommunications, agricultural technology, among others.

As can be seen from the below chart, S&P/NZX All Information Technology (Sector) has outperformed S&P/NZX All Index by ~2% in the span of past 5 years.

*Till January 14, 2021.

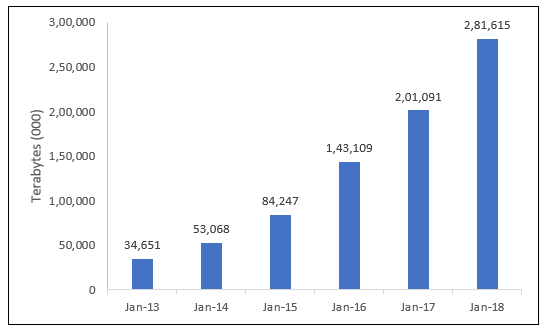

Exhibit 2: Data on The Supply and Use of ICT

Data Source: Stats NZ; Chart Created by Kalkine Group

Key Growth Drivers

Some of the key growth drivers for the communication and IT services sector have been highlighted below: -

Evolving Technology trends mandated higher R&D

The country’s technology sector offers multiple investment opportunities due to its ambitious and scalable firms that remain on the edge of innovation to stay afoot in the evolving technology trends with market-leading solutions that will cater to the global problems. Resultantly, the sector continues to invest more in R&D than any other industry to develop niche or speciality products and services that will provide a key competitive advantage in the global arena. Owing to its consistent R&D initiatives, the sector plays a key role in the digitisation and diversification of the country’s economy. This has also aided in the sustained growth momentum of the sector as visible in the Exhibit 3 below.

The sales of domestic published software and information technology services witnessed an improvement in overall performances during 18 June 2018 to 5 March 2020 period as the decline in the sales of domestic information technology of 3.2% could only partially affect 6.6% growth in sales of published software. On the other hand, the overall exports of published software and information technology services witnessed a growth of around 15% over period 18 June 2018 to 5 March 2020 with export declining by mere 1%.

Exhibit 3: Performance of the Sector

.png)

Data Source: Stats NZ; Table Created by Kalkine Group

Increasing Trend of Building Digital Capability

The demand of communication and IT services sector globally have also been driven by digital disruption due to the rise of advanced technologies viz; the Internet of Things (IoT), artificial intelligence (AI), robotics, among others. Further, the emergence of 5G technologies also throws a robust growth potential for the sector going forward as this will aid in providing further scope for scalability and revenue visibility. It throws opportunities for enhancement in wireless broadband services, self-driving cars potential, enhanced use of robotics and industry automation and immense machine type communications (the internet of things), thus brightening the long-term growth visibility of the sector. Apart from this, the growth of the sector has also been supported by the government’s initiatives to become a leading digital nation through technology-enabled digital businesses coupled with increasing adoption of digital technologies viz; IoT and AI technologies, exploiting ICT-enabled opportunities, digital health mission, among others. All these activities will continue to have a positive bearing on the growing visibility of the overall sector.

Outlook

The sector growth is to be driven by the country’s innovation friendly compliance environment, highly educated workforce, ease of doing business and quality of life. Moreover, the outlook looks promising considering its robust primary industry, large regional centres of innovation in the country and access to global markets. With the strong growth of the primary sector, the agritech companies have increased their investment in the digital space leaving no stone unturned to capitalize on opportunity and are creating innovative solutions in order to enhance the productivity and efficiencies of New Zealand’s farming, fishing, food, animal welfare, biosecurity and forestry industries. In line with this, the disruption in the FinTech space also bodes well for the sector. This was supported by various factors that includes a business friendly and agile regulatory system and highly competitive domestic environment that led to constant innovation and process automation. Resultantly, the FinTech companies are consistently redefining the process of financial transactions in the country and aids in bringing efficiencies in the system. Besides, a growing portfolio of promising start ups and advent of 5G technologies will also aid in exploring potential growth opportunities.

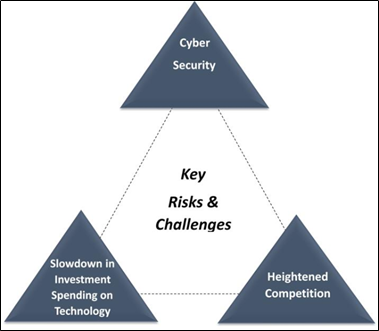

Key Risks and Challenges

Exhibit 4: Key Risks and Challenges

Source: Kalkine Group

CyberSecurity

The increasing adoption of digital technologies by the public as well as private companies towards implementing transformation of the business has given rise to cybersecurity risks. So, this will have an adverse impact on the organisations ability to deliver digital products and services in a way that retains the trust and confidence of their customers or stakeholders. In order to ensure business transformation to remain sustainable and achievable, organisations are required to effectively address cybersecurity concerns through increasing investment in technology upgradation, which will enable the companies in consistently developing and delivering digital products and services.

Slowdown in Investment Spending on Technology

Increased Level of Competition

The sector has suffered from the impact of heightened competition due to the presence of lot of players in the space - both global as well as domestic players. Due to the increased competition, the companies opt for higher spend on sales as well as marketing and branding activities resulting in enhanced product pricing pressure. In order to stay afloat in competitive world stage, improvisation of technological products and services would be very much required forcing the companies to remain at the forefront of innovation. This will be achieved through consistent investment on R&D, creation of intellectual property, and acquiring of right talent.

Apart from the sector-specific factors, we have also analyzed operating and financial performances of four NZX-listed companies operating in this sector, and have provided insights on their performance and growth prospects .

1) Solution Dynamics Ltd (Recommendation: Speculative Buy, Potential Upside: Higher Single-Digit) (M-Cap: NZ$46.115 Million, Gross Dividend Yield: 3.968%)

Business Description:

Solution Dynamics Ltd (NZX: SDL) is a full-service technology-focused communications solutions provider and is engaged in improving customer communication delivery through digital transformation. SDL helps in streamline customer communications delivery for businesses through its integrated solutions.

Outlook

The company stated that strong underlying international growth prospects are accessible for SDL’s software platforms. Therefore, SDL will maintain its investment activities directed towards sales channel development and customer support infrastructure globally so that growth momentum can be maintained.

While the company anticipates continued growth in FY 2021 – the Directors of SDL reiterated earnings guidance of $2.0 to $2.5 million. However, this has been lowered by drags from COVID-19.

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status. https://www.bollingerbands.com/

The stock seems to be correcting from its recent high of $3.34 which is obvious from two consecutive weeks of lower closing around its low prices. However, the magnitude of the fall is not steeper. The technical indicator RSI with a reading around 65 but a curve at the end bending down, suggests the softening of bullish momentum.

Going forward, the stock may have resistance around the previous high of $3.34 whereas support could be around 20 periods SMA of $3.00.

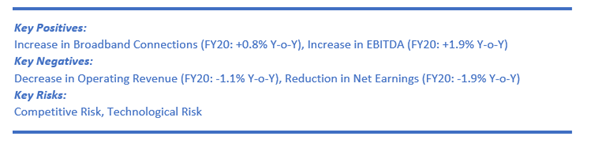

2) Chorus Ltd (Recommendation: Buy, Potential Upside: Lower Double-Digit) (M-Cap: NZ$3.6 Billion, Gross Dividend Yield: 4.141%)

Business Description:

Chorus Ltd (NZX: CNU) is New Zealand’s largest fixed line telecommunications network operator.

Outlook

The company’s focus is all about connecting more New Zealanders to the fibre. The company has put this at the top of its strategic focus with the target of 1 million fibre connections by 2022. This happens to be a substantial step up from the 751,000 connections. At the time of FY 2020 results, the company provided FY 2021 guidance and mentioned that EBITDA is expected to be $640 million to $660 million.

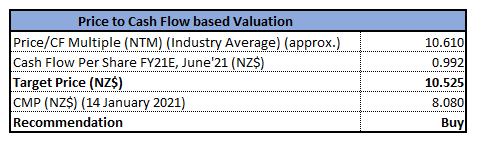

Valuation Methodology: P/CF Based Relative Valuation (Illustrative)

P/CF Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

We have applied P/CF multiple based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms).

Considering the expected upside and increase in EBITDA, we give a “Buy” rating on the stock at the current price of NZ$8.080 per share, up by 0.37% on Janaury 14, 2021.

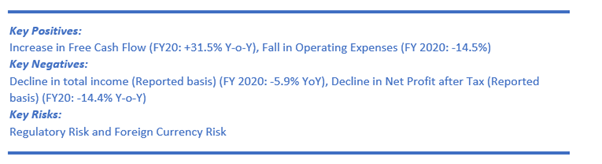

3) Telstra Corporation Ltd (Recommendation: Hold, Potential Upside: Lower Double-Digit) (M-Cap: NZ$39.7 Billion, Gross Dividend Yield: 5.203%)

Business Description:

Telstra is Australia's leading telecommunications as well as information services company. It offers the full range of communications services and it competes in all the telecommunications markets.

Outlook:

The company is on track to achieve $2.5 billion net cost reduction target in FY22. The company added that cost reductions in FY 2021 are expected to be achieved predominantly with the help of indirect as well as direct labour, enabled by the ongoing shift of customers onto digital sales and service channels and the strong focus on vendor costs and workforce efficiency. It was mentioned that with the nbn rollout effectively complete and being over half way through the T22 strategy, TLS believes it would be turning underlying EBITDA back to growth by FY 2022 and it was determined on delivering the ambition to be in the range of $7.5 to $8.5 billion of the underlying EBITDA by FY 2023.

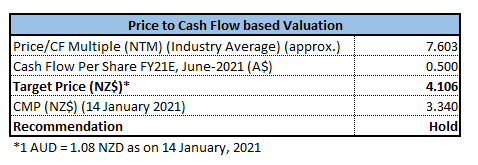

Valuation Methodology: P/CF Based Relative Valuation (Illustrative)

P/CF Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

We have applied P/CF multiple based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms).

Considering the expected upside and increase in FCF, we give a “Hold” rating on the stock at the current price of NZ$3.340 per share, up by 1.83% on January 14, 2021.

4) Smartpay Holdings Ltd (Recommendation: Hold, Potential Upside: Lower Double-Digit) (M-Cap: NZ$197.29 Million)

Business Description:

Smartpay Holdings Ltd (NZX: SPY) is ANZ’s largest independent full-service EFTPOS provider. It services more than 25,000 merchants with ~35,000 secure as well as feature-rich EFTPOS terminals.

Outlook:

The company has released presentation for half-year ended 30th September 2020 and it was stated that the robust growth being achieved in Australian Acquiring business is to some degree disguised by COVID impact on the early part of half-year results. Notably, NZ business has witnessed resilience through the COVID period. Considering the current level of growth as well as underlying performance of the business, the company expects to garner record revenue in H2.

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status. https://www.bollingerbands.com/

Giving outbreak from its bullish consolidation phase, the stock has given close at a peak price for the ongoing week thereby demonstrating strength in uptrend. The technical indicator RSI with a reading around 70 suggests strong bullish momentum besides indicating the overbought status for the stock.

Going forward, the stock may have resistance around $0.97 whereas support could be around $0.68.

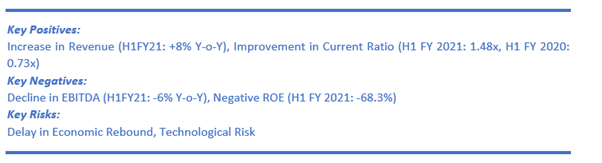

Considering the technical overview and improvement in current ratio, we give a “Hold” rating at NZ$0.850 per share, up by 7.59% on January 14, 2021.

Comparative Price Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...