Company Overview: CIMIC Group Limited (ASX: CIM) is an engineering-led construction, mining and services group focused on generating sustainable shareholder returns by delivering innovative and competitive solutions for its clients. The Group comprises several companies including mining and mineral processing companies Thiess and Sedgman, construction business CPB Contractors, including Leighton Asia and Broad, Services specialist UGL, and public private partnerships arm Pacific Partnerships. The company’s businesses deliver services in Australia as well as in various markets in Asia, Southern Africa, the near Pacific, and the Americas.

.png)

CIM Details

.png)

Focused on Providing Sustainable Returns to Shareholders: CIMIC Group Limited (ASX: CIM) is an engineering-led construction, mining, services, and public private partnerships leader that provides services in Australia as well as in various select markets of Asia, the near Pacific, Southern Africa, and the Americas regions. The company is in pursuit of operational excellence in terms of identifying value-adding engineering solutions; applying a disciplined approach to risk management; rigorously managing cash; maintaining tight control on costs and ensuring an uncompromising focus on safety. The company’s mission is to provide sustainable shareholder returns by delivering projects for its clients while providing safe, rewarding and fulfilling careers for its people. From 2016 to 2019, the company’s revenue and gross profit have increased at a CAGR of 10.6% and 15.5%, respectively.

Amid COVID-19 pandemic, the company is focused on the continued provision of essential services and critical infrastructure while it maintains a disciplined focus on sustaining a strong balance sheet with enough cash balance. Right now, CIMIC Group is well placed in geographies and markets that are expected to continue to grow and provide a broad range of opportunities for the foreseeable future.

FY19 Performance Highlights: During FY19, CIMIC’s operating companies achieved improved returns, with net profit after tax (NPAT) of $800 million, up 3% on the previous year. The company reported revenue of $14.7 billion in FY19 with stable operating profit, PBT and NPAT margins of 8.4%, 7.5% and 5.4%, respectively. Further, the company reported operating cash flow of $1.7 billion with 80% EBITDA cash conversion.

During the year, the company saw one-off post tax impact of $(1.8) billion relating to the financial investment of BIC Contracting (BICC) as a result of the decision to exit the Middle East region which will allow it to focus on its resources on the growth opportunities in its core markets.

The Mining & mineral processing segment reported revenue of $4,496.9 million, up by 13.4% on 2018, driven by the contributions from a diverse range of mining and mineral processing contracts and increased production levels. The Construction and Services segment reported revenues of $7,532.1 million and $2,626.4 million, respectively.

Over the year, the company developed a strong pipeline of new work by securing various new contracts. During the year, the company returned $525.8 million of cash to shareholders through dividends and share buyback. .png)

Key Financial Highlights (Source: Company Reports, Thomson Reuters)

Q1FY20 Highlights: In the first quarter of FY20, the company reported revenue of $3.3 billion, compared to $3.4bn in 1Q19. For the quarter, the company reported robust operating profit, PBT and NPAT margins of 8.4%, 6.9% and 5.0% respectively.

For the quarter, the company generated operating cash flow pre-factoring of $1.6 billion in last 12 months (LTM) and Delivered 76% EBITDA cash conversion pre-factoring in last 12 months (LTM). During the quarter, the company was awarded new work of $2.5 billion while it continued to deliver essential construction work. The company ended the quarter in a strong liquidity position with gross cash of $4.5 billion. .png)

Q1FY20 Financial Performance (Source: Company Reports)

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 80.07%. HOCHTIEF Australia Holdings Ltd. and The Vanguard Group, Inc. hold the maximum interest in the company at 76.60% and 0.92%, respectively..png)

Top 10 Shareholders (Source: Refinitiv, Thomson Reuters)

A Quick Look at Key Ratios: For FY19, the company’s gross margin stood at 44.1%, higher than the prior corresponding year margin of 42.5% and the industry median of 14.7%. Further, the company’s EBITDA margin stood at 14.4% in FY19, higher than FY18 margin of 11.4% and the industry median of 6.9%. The company’s asset turnover ratio stood at 1.43x, higher than the industry median of 0.75x..png)

Key Metrics (Source: Refinitiv, Thomson Reuters)

Rewarding Shareholders through Dividend: During FY19, the company paid an interim dividend of 71 cents per share, up 1.4% YOY, fully franked. Due to the BICC one-off impairment, CIMIC decided not to declare a final dividend for FY19. The company’s payout ratio for ordinary dividends stood at 28.8% in FY19, lower than the payout ratio of 65% reported in FY18, impacted by the Middle East one-off. For FY18, the company had paid a total dividend of 156 cents per share. It is worth noting that over the past five years, the company has returned $2,523.9 million to its shareholders in the form of dividends and share buybacks. .png)

Shareholder Returns (Source: Company Reports)

Ventia’s Proposed Acquisition of Broadspectrum: Ventia, an independent company formed by a 50/50 investment partnership between funds managed by affiliates of Apollo Global Management and the CIMIC Group, was recently notified by the Foreign Investment Review Board (FIRB) that the Australian Government has no objection to Ventia’s proposed acquisition of Broadspectrum. If the acquisition gets completed, the combined group is expected to generate revenue of over $5 billion.

Recent Contracts: Over Q1FY20, CIMIC’s services specialist, UGL, secured contracts to provide maintenance, shutdown and project services for its clients in the mining sector and it was also awarded contracts to operate and maintain a tram and bus network in Adelaide and manufacture locomotives in Newcastle, NSW.

The company’s construction business, CPB Contractors, was recently selected to deliver upgrades to two major regional highway projects in Victoria and Queensland, and it was also selected to deliver three road projects under the Port Wakefield to Port Augusta Regional Projects Alliance.

COVID-19 Update: In response to COVID-19, the company has implemented various protocols to manage the risk of infection, including setting standards for routine prevention activities and increased cleaning, management of critical business teams, social distancing and flexible work regimes including working from home where available. The company is continuously monitoring the risks and responding to the changing conditions, to ensure the safety of its workforce and operations.

Key Risks: The company is exposed to the risk of COVID-19 pandemic as it could impact the company’s operations. Further, the company’s operations are also exposed to the risk of changes in economic, political, or societal trends, or unforeseen external events and actions may affect business development and project delivery.

What to Expect: In line with its FY20 focus on sustainable growth and returns, CIMIC Group is continuously pursuing various new contracts. Notwithstanding the short-term impacts from the current COVID-19 pandemic, the outlook across the company’s core markets remains positive as the Governments across various markets have announced their support to major social, transport and economic infrastructure projects. CIMIC Group intends to support this demand for critical infrastructure.

For FY20, the company expects its NPAT to be in the range of $810 million - $850 million, subject to market conditions and COVID-19 impacts. The company’s results are expected to be supported by the strong level of work in hand and positive outlook across its core markets. It is to be noted that, as CIMIC Group is still monitoring the impacts of COVID-19, if required it will provide an update to FY20 profit guidance..png)

NPAT Guidance (Source: Company reports).png)

Key Valuation Metrics (Source: Refinitiv, Thomson Reuters)

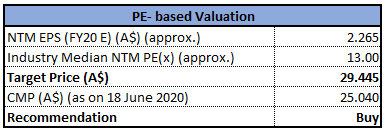

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation (Illustrative)

Price to Earnings Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Over the past six months, the company’s stock has corrected by 26.47% and is trading below the average of 52-week low and high of $11.87 and $47.14, respectively, offering a decent opportunity for accumulation. The company currently has an annual dividend yield of 6.11%. The company has a strong financial position and a balance sheet that gives it the flexibility to pursue strategic growth initiatives and capital allocation opportunities. The company’s future results are supported by a strong level of work in hand and a positive outlook across the Group’s core markets. We have valued the stock using Price to Earnings multiple based illustrative relative valuation method and have arrived at a target price with low double-digit upside (in % terms). Considering the aforesaid facts, the company’s decent operating and financial performance, decent outlook, work pipeline, and current trading levels, we give a “Buy” recommendation on the stock at the current market price of $25.04, down by 2.568% on 18 June 2020.

.png)

CIM Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...