Overview: Chorus Limited (NZX: CNU) happens to be NZ’s leading fixed-line telecommunications network operator. The company is engaged in building as well as managing an open access internet network, rolling out ultra-fast broadband which is expected to help the generations to come. The phone and broadband providers in New Zealand access the company’s network to provide innovative products as well as services to their customers. The company continues to expand its network as well as improve its performance in order to support New Zealand to grow. The company has been maintaining as well as building the network mainly made up of local telephone exchanges, cabinets, as well as copper and fibre cables.

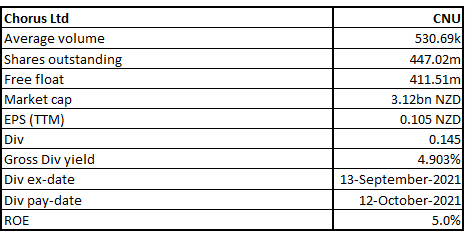

CNU Details

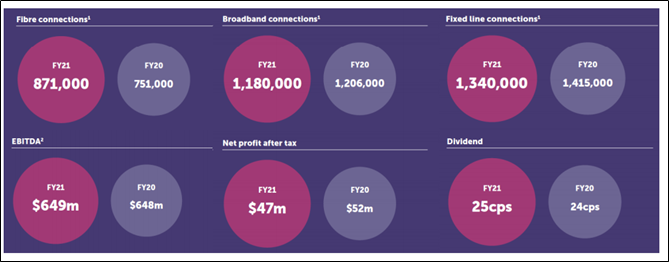

Results Performance (Audited Annual Results for the year ended 30th June 2021)

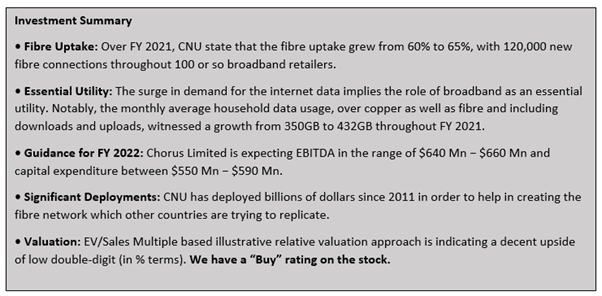

Decent Annual Results: Chorus Limited posted EBITDA for FY 2021 amounting to $649 Mn as compared to the FY 2020 figure of $648 Mn and its NPAT amounted to $47 Mn as compared to $52 Mn in FY 2020. The company’s operating revenue for FY 2021 came at $947 Mn, while in FY 2020, it was $959 Mn. Over the year, fibre uptake witnessed the growth from 60% to 65%, with 120,000 new fibre connections throughout 100 or so broadband retailers.

Exhibit 1: Overview of FY 2021

Key Data (Source: Company Reports)

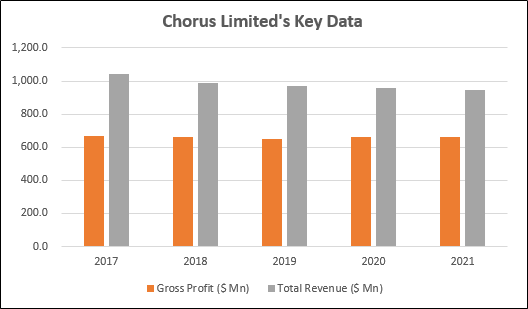

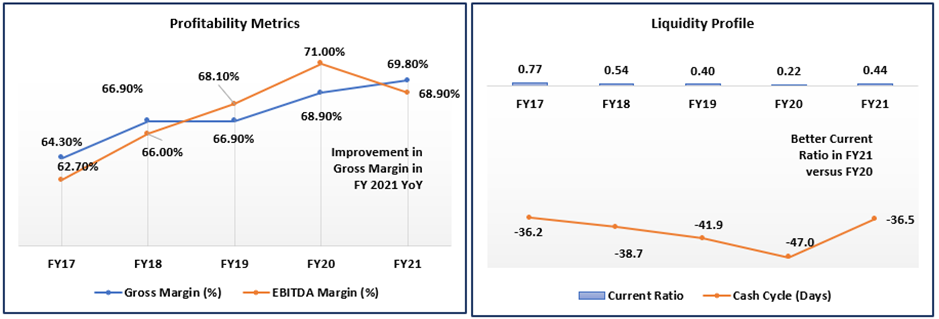

Tight Management of Costs: Despite the disruptions related to the COVID-19 during FY 2021, the company stated that the customer satisfaction encountered a rise from 8.1 to 8.2 for the installations as well as 7.3 to 7.5 for the service to homes with an existing or 'intact' fibre socket. It was mentioned that the unfavourable market conditions due to the COVID-19 on the broadband demand, along with the competition from other fibre as well as wireless networks, resulted in the drop of $12 Mn in revenue as compared to FY 2020. Having said that, prudent management of costs as well as absence of the one-off costs related to the COVID-19 pandemic which was incurred in FY 2020 supported the company in achieving its goal of the marginal growth in EBITDA.

Exhibit 2: Overview of Gross Profit and Total Revenue

Source: Company Reports, Analysis by Kalkine Group

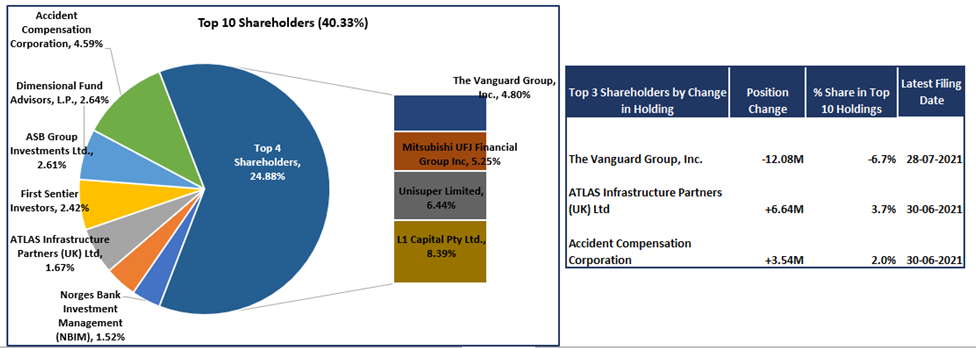

Top 10 Shareholders:

The top 10 shareholders of the company form ~40.33% of the total shareholding as shown in the chart below. Notably, L1 Capital Pty Ltd. and Unisuper Limited are holding 8.3919% and 6.4394%, respectively.

Exhibit 3: Top 10 Shareholders

Source: Analysis by Kalkine Group

Key Metrics:

The company’s gross margin stood at 69.8% in FY 2021 as compared to the industry median of 65.3%. Also, its EBITDA margin was 68.9% in FY 2021 as compared to industry median of 32.3%. CNU’s current ratio stood at 0.44x in FY 2021 as compared to 0.22x in FY 2020 and, therefore, it could be said that the company is possessing decent liquidity position.

Exhibit 4: Key Metrics

Source: Analysis by Kalkine Group

Recent Update

Commerce Commission Released Draft RAB Decision for Fibre Business of CNU: In the release dated 19th August 2021, it was mentioned that the Commerce Commission published the draft decision proposing an initial RAB (or regulated asset base) of $5.427 Bn for Chorus Limited’s regulated fibre business from the month of January 2022. Also, it needs to be noted that the Commission’s draft RAB is made up of core fibre assets of $3.98 Bn as well as the financial loss asset of $1.446 Bn.

In the month of March, CNU proposed the conservative starting RAB of $5.5 Bn based on the modelling work by the international experts Analysys Mason.

Strong Digital Infrastructure

The company has stated that NZ has strong digital infrastructure which provides options to the consumers about how they decide to access the broadband. As surge in the data demand during the lockdowns shows, peak time capacity as well as performance is of priority for the consumers. The company is also encouraged by the recent Commerce Commission proposals which require retailers to offer clearer and proper product disclosure for the consumers. The people of NZ should be able to take decisions which are based on facts as well as unbiased equivalent data, instead of taking decisions based on the partial information as well as hype.

Capital Management

The company has stated that it would be paying the final dividend of 14.5 cps, fully imputed, on 12th October 2021. Additionally, the supplementary dividend of 2.56 cps would also be payable to the shareholders who are not resident in NZ. It needs to be noted that the dividend reinvestment plan would remain in place for the final dividend at the discount rate of 2%.

The NZ$400 Mn bond was repaid in the month of May 2021. It was mentioned that this bond was refinanced in the month of December 2020 with the dual tranche $400 Mn bond due to mature in the month of December 2027 as well as December 2030. CNU’s board is of the view that the ‘BBB’ or equivalent credit rating is appropriate for Chorus. The company is expected to maintain the capital management as well as financial policies which are consistent with these credit ratings. At 30th June 2021, the company was having long-term credit rating of BBB/stable outlook by Standard & Poor’s as well as Baa2/stable by the Moody’s Investors Service.

Outlook

Guidance for FY 2022: The company has stated that guidance for FY 2022 is subject to no material changes in the regulatory or competitive outlook. Therefore, for FY 2022, the company is expecting an EBITDA in the range of $640 Mn − $660 Mn. Notably, for FY 2022, the capital expenditure is anticipated to be between $550 Mn − $590 Mn. The company has given FY 2022 initial dividend guidance of 26 cps.

Key Risks:

Chorus is exposed to the variety of financial risks, including the volatility in the electricity prices. The effects of COVID-19 pandemic can result in unfavourable market conditions. The company is also exposed to the risk of competition from other fibre as well as wireless networks. These factors have the potential to impact the company’s revenue.

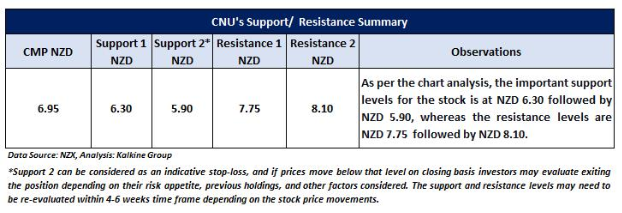

Technical Overview:

Chart:

Source: REFINITIV

Note: Purple Color Line Reflects RSI (14-Period)

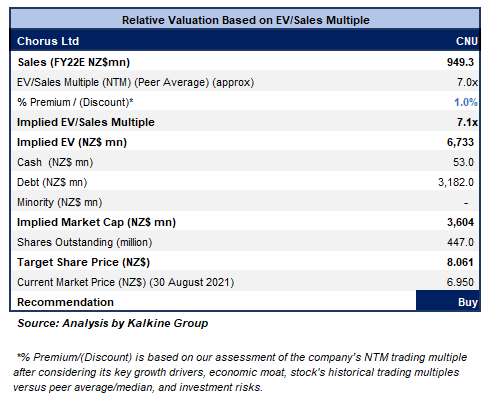

Valuation Methodology: EV/Sales Based Relative Valuation (Illustrative)

Stock Recommendation

The company stated that broadband’s role as an essential utility has been reflected in surge in the data demand. Notably, monthly average household data usage, including downloads as well as uploads, encountered a growth from 350 gigabytes (GB) to 432GB throughout the year. Also, fibre customers averaged 500GB in June, reflecting a rise from 436GB the year before.

The stock has been valued using an EV/Sales multiple- based illustrative relative valuation method and a target price with the potential of low double-digit (in percentage terms) upside, has been arrived. The company might trade at a slight premium to EV/Sales Multiple (NTM) (Peer Average) considering significant deployments which the company has made as well as higher EBITDA margin as compared to the industry median.

Thus, we give a “Buy” rating on the stock at the price of NZ$6.950 per share (New Zealand Time: 1:19 PM (GMT +12)) on 30th August 2021.

Note 1: The reference data in this report has been partly sourced from REFINITIV.

Note 2: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the analysis has been achieved and subject to the factors discussed above alongside support levels provided.

Technical Indicators Defined:-

Support: A level where-in the stock prices tend to find support if they are falling, and downtrend may take a pause backed by demand or buying interest.

Resistance: A level where-in the stock prices tend to find resistance when they are rising, and uptrend may take a pause due to profit booking or selling interest.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...