Company Overview: Chorus Limited (NZX: CNU) is a leading telecommunications infrastructure company that provides broadband, data, and voice services. The company’s product portfolio includes fibre broadband, fibre premium, copper-based voice, data services and copper-based broadband. The company’s strategy is focused on developing long-term future of its business, growing new revenues, optimizing non-fibre business, and wining core fibre business.

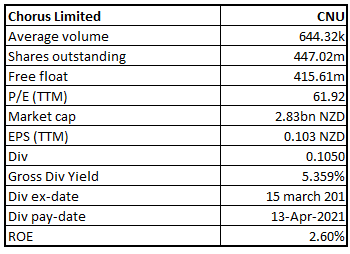

CNU Details

The provider of Fixed Line Communication Infrastructure, Chorus Limited (NZX: CNU) is New Zealand’s leading telecommunications infrastructure company. The company has a market capitalisation of ~$2.83 billion as on June 28, 2021.

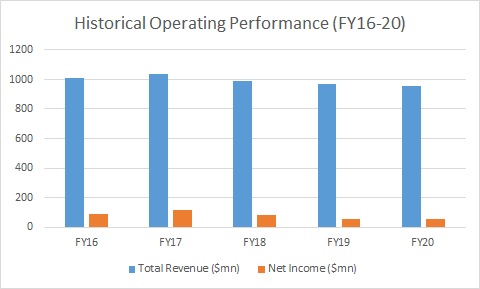

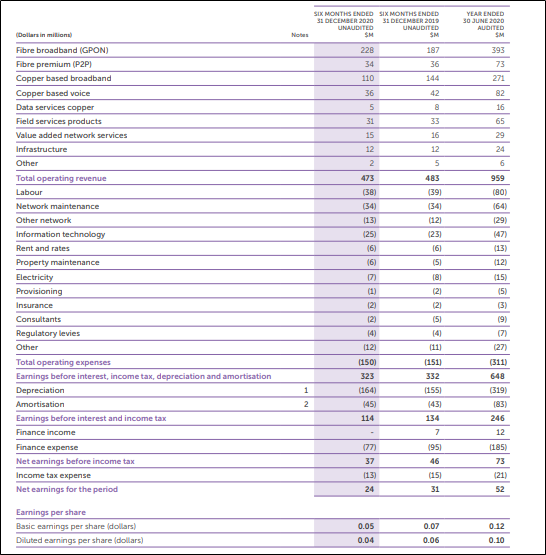

Exhibit 1: Historical Operating Performance

(Source: Company Reports, Analysis by Kalkine Team)

Recent Updates

As per an update from The Commerce Commission as on 27 May 2021, the commission provided the draft decision on CNU’s estimation of the price-quality determination for the first regulatory period for fibre (2022-2024), annual revenue is expected in the range of $689-$786million, including pass-through costs, which remains primarily consistent with CNU’s forecast fibre revenues for the period.

Results Performance (Half-Year ended 31 December 2020 – H1FY21)

The company’s revenue from continuing operations for the interim period stood at $473 million, a decline of 2% on the previous corresponding period (pcp). The period witnessed continued growth in broadband revenue as more consumers transition from copper to fibre services. However, mass market broadband connections fell across reflecting ongoing competition from alternative fibre and wireless network. Connection revenues across legacy fibre premium and copper voice continued to experience a decline on account of consumers migration to alternative services. The company’s continued focus on reducing discretionary costs has resulted in a $1 million reduction in total expenses during the period to $150 million. Thus, reduction in operating expenses and D&A led to a restricted decline in EBIT for the period to $114 million as against $134 million in the same period last year.

Interest expense for the period decreased by $18 million due to the repayment of the GBP EMTN in April 2020 and the weighted average effective interest rate moving from 5.2% to 4.0% in the period. This decrease was partially offset by increased interest on fixed rate NZD bonds in comparison to HY20 due to the issue of new NZD bonds of $400 million in December 2020. Net profit for the period stood at $24.00 million, a decline of 22.6% on pcp.

The Board of Directors declared an interim dividend of 10.5 cents per share (fully imputed) with payment date as on 13 April 2021.

Exhibit 2: Income Statement (1HFY21 vs 1HFY20)

(Source: Company Reports)

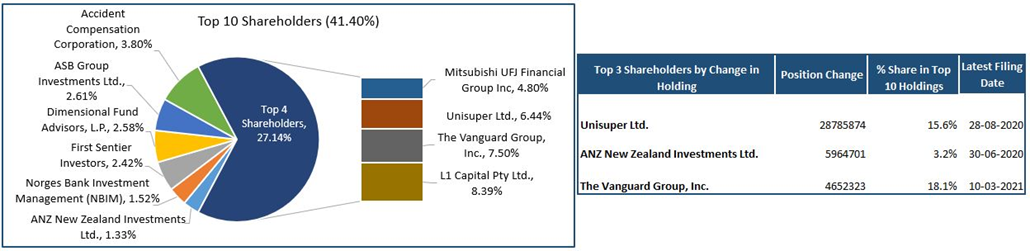

Top 10 Shareholders: The top 10 shareholders have been highlighted in the pie-chart, which together forms around 41.40% of the total shareholding. L1 Capital Pty Ltd. and The Vanguard Group, Inc. are holding maximum stake in the company at 8.39% and 7.50%, respectively, as provided in the table below:

Exhibit 3: Top 10 Shareholders

Source: Analysis by Kalkine Group

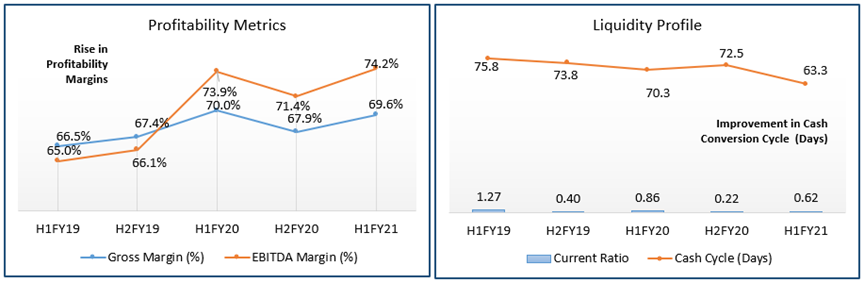

A Quick Look at Key Metrics: The company’s gross margin and EBITDA margin for H1FY21 stood at 69.6% and 74.2%, better than the industry median of 61.7% and 30.0%, respectively, implying greater efficiency in managing input and operating costs by the company than peers. Its cash cycle for H1FY21 stood at 63.3 days, lower than the H1FY20 result of 70.3 days, implying that the company efficiently managed its asset-liability balances. The period witnessed a significant increase in current ratio over the H2FY20 but a moderate decline over the H1FY20.

Exhibit 4: Key Metrics

Source: Analysis by Kalkine Group

Outlook:

There has been an increased demand for fibre installations on the back of strong housing growth. The pandemic which necessitates work-from-home culture is helping increased demand for fibre broadband while softening copper broadband which is reflected from Q3FY21 overview.

In the meanwhile, the company has provided FY21 guidance expecting EBITDA in the range of $640 million to $660 million, a marginal decline of 1.2% from FY20. Gross capex for FY21 has been increased to $670 - $700 million from prior range of $630 to $670 million. FY21 dividend is expected to be 25 cents per share, subject to no material adverse changes in circumstances or outlook.

Key Risks:

The company besides various financial risks, is also exposed to the risk of cybersecurity. The company does ensure cybersecurity is addressed through technology selection but completely ruling out the same is a difficult task.

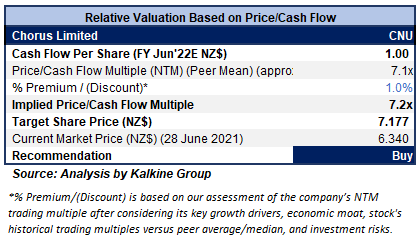

Valuation Methodology: Price/Cash Flow Multiple Based Relative Valuation (Illustrative)

Technical Overview:

Weekly Chart –

Source: REFINITIV

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack. https://www.bollingerbands.com/

The stock has given a flattish close on the first trading session of the ongoing week, forming a ‘Doji’ candle, implying a potential bullish reversal for the stock. The technical indicator RSI with a reading around 35 and a flattish curve at the end, suggests flattish momentum for the stock.

Going forward, the stock may have resistance around the 50% retracement level of $7.14 whereas support could be around the previous week’s low of $6.00.

Stock Recommendation:

The company’s fibre uptake lifted from 60% to 63% with 62,000 fibre connections added in the first six months, reflecting the current demand. Moreover, strong housing growth is fueling increased demand for fibre installations. Further, COVID-19’s effect on net migration into the country has softened demand on overall broadband connections and increased demand for fibre broadband. CNU’s second phase of fibre build, UFB2, continues to track ahead of schedule and is now taking the socio-economic benefits of fibre to many smaller communities.

We have applied P/CF based relative valuation (on an illustrative basis) and the target price so arrived reflects a rise of low double-digit (in % terms). We have applied a slight premium to P/CF Multiple (NTM) (Peer Average) considering shorter cash conversion cycle and lower debt to equity as compared with peers.

Considering the aforesaid facts, we give a “Buy” recommendation on the stock at the current market price of $6.34 per share, down 0.16% on June 28, 2021.

Note 1: The reference data in this report has been partly sourced from REFINITIV.

Note 2: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the analysis has been achieved and subject to the factors discussed above alongside support levels provided.

Technical Indicators Defined: -

Support: A level where-in the stock prices tend to find support if they are falling, and downtrend may take a pause backed by demand or buying interest.

Resistance: A level where-in the stock prices tend to find resistance when they are rising, and uptrend may take a pause due to profit booking or selling interest.

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...