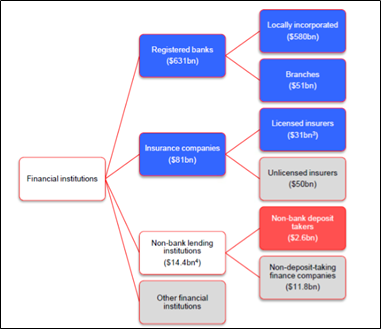

According to the Reserve Bank of New Zealand, the banking system of NZ is highly concentrated as there are 27 registered banks. However, 4 large Australian-owned banks (i.e. ANZ, ASB, BNZ, and Westpac) are responsible for 85% of the bank lending. Notably, five NZ-owned banks account for 8% of the bank lending. The NZ financial system is dominated by the banking sector, with banking assets accounting for a very large share of overall financial system assets. The managed fund industry is small compared to banks, with around $157 billion of assets under management.

Financial Institutions’ Total Assets (as at 31 March 2020) (Source: RBNZ)

Key Stats in Banking

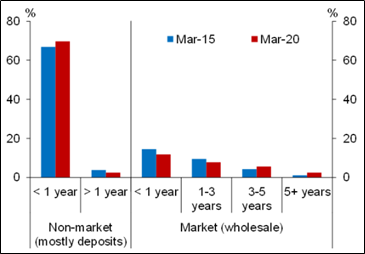

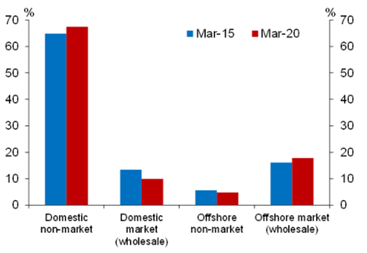

Majority of Bank Funding is Short-Term

The majority of bank funding happens to be short-term, with ~82% having a maturity of less than 1 year and just 12% with a maturity more than 2 years. Comparatively, bank assets have much greater maturities because of maturity transformation function of banks.

According to RBNZ, ~59% of lending is mortgages, at terms of up to 30 years. However, these assets have a relatively short time to re-price.

Bank Funding Composition (Source: RBNZ)

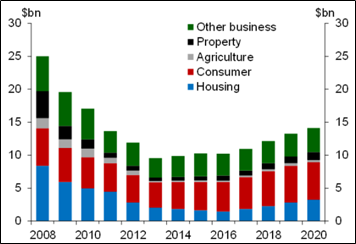

Overview of Non-Bank Lending Institution

The Non-bank lending institutions (NBLIs) comprise of non-bank deposit-taking institutions and non-deposit-taking finance companies. The Reserve Bank of New Zealand regulates NBDTs but does not regulate or supervise non-deposit-taking finance companies. NBLIs account for just over three per cent of intermediated credit, mainly focusing on the business and consumer sectors.

NBDTs are bodies that provide debt securities to the public and carry on the business of borrowing and lending money or providing financial services, or both. However, they do not include registered banks. Currently, there are 20 licensed NBDTs operating in New Zealand. As at March 2020, total assets of NBDTs stood at $2.62 billion, of which $1.07 billion was in building societies, and $1.21 billion was in credit unions.

NBLI Lending by Sector (Source: RBNZ)

Importance of Insurance Sector

The insurance sector plays an important role in the financial system by spreading the costs of risk events through time, across the population and, via reinsurance, internationally. A resilient insurance sector facilitates the efficient allocation of resources across the economy through the pricing and redistribution of risk.

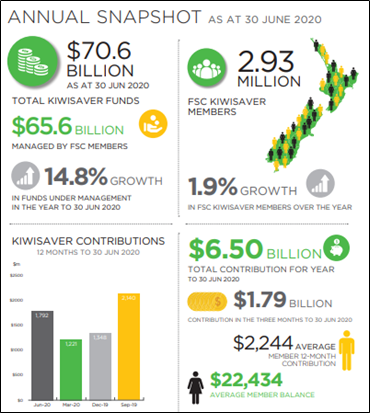

Annual Snapshot (Source: FSC)

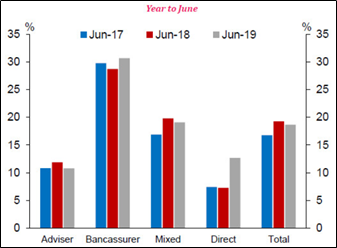

New Zealand’s Life Insurers Enjoy More Profitability

The life insurers of New Zealand are relatively profitable compared to their peers in many developed OECD countries. In 2017, boosted by strong investment returns, the return on equity for New Zealand life insurers was 16.2 percent, which was higher than the median of 12.9 percent.

There is considerable variation in profitability within the life insurance sector. Pure bancassurers, who make up 13 percent of the sector, are the most profitable and have the lowest expenses. Banks have existing distribution networks that allow bancassurers to reach their customers more easily.

Profit after tax as a share of gross premium (Source: RBNZ)

Life Insurance Companies Continues to Provide Support to Kiwis

As per the latest data released by the Financial Services Council, the life insurance industry is continuing to support Kiwis when they need it most. The FSC’s “Spotlight on Insurance 2020” revealed that for the year ended 31 March 2020, the industry paid out $1.49 billion in claims, or just over $4 million a day, which is a $200 million increase from the previous year.

New Zealand life insurers have a return on equity higher than the median, even after allowing for high expenses. The high expenses are driven by high commission rates, soft commissions, some policy replacement activity, and a lack of scale. High expenses have a negative impact on premium affordability and value for money for policyholders.

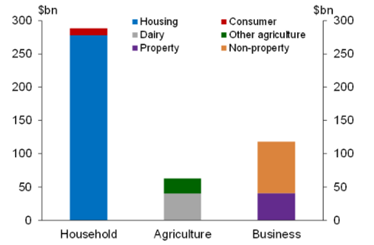

Role of Banks

Banks play a role in providing payment and settlement services which are necessary to settle day-to-day transactions. The banking system is the source of the majority of lending. Direct capital funding and non-bank funding together are accounting for merely 6 percent of non-financial private sector borrowing.

Key Data (Source: RBNZ)

As regards lending, about 62 percent of bank lending is to the household sector. Lending to the business sector accounts for 25 percent of total lending, around 34 percent of which is property related. Lending to the agriculture sector accounts for 13 percent of which the dairy sector accounts for about two-thirds.

Key Data (Source: RBNZ)

Banks remain exposed to offshore funding market volatility despite banks hedging their interest rate risks. Any increased cost of funds can flow through to retail rates.

The banking role has become more significant as the economy is passing through pandemic-led global economic shock. The government has announced a series of measures aimed at protecting businesses, jobs, and the economy. The implementation of all these measures have to happen through the banking system. Banks’ responses for households, SMEs, corporate, commercial property, and agriculture lending are different and focused.

The Finance Ministry has constituted the Business Finance Guarantee scheme which will provide an $8-12 billion wage subsidy scheme ensuring people remain in jobs during the lockdown period.

The Reserve Bank of New Zealand is there to ensure that banks can access enough cash to keep lending at low-interest rates, will provide term funding to banks at a very low- interest rate to help them support the Government’s Business Finance Guarantee Scheme and promote lending to businesses.

Credit Conditions Observed Over the First Six Months of 2020

Credit development provided by Banks has been predominantly demand-driven, post-lockdown. Banks experience demand for loans for working capital from SMEs and corporates to meet fixed expenses. However, the demand for credit for Capex has fallen. Banks have noted that the low-interest rates may support credit demand, however, uncertainty about future demand is causing businesses to review their investment plan. Banks have tightened lending standards to sectors directly exposed to the COVID-19 shock such as tourism, retail, and construction. However, for some sectors such as commercial property and dairy, lending is a continuation of trends that precedes COVID-19.

Governments across the world are raising debt to pay for increased spending and support for their economies. Developed countries are raising debt despite having an average net debt position above 70% of GDP with the UK about 75%, the US above 80%, Italy above 120%, and Ireland above 50% of GDP. Fortunately, New Zealand has a sound financial position with net debt-to-GDP around 19%, enabling it to fight COVID-19. The international credit rating agency has re-affirmed its highest Aaa credit rating on New Zealand, saying that the economy is expected to remain resilient.

Challenges Faced by Financial Sector

COVID-19 might give rise to credit impairment as the viability of businesses in many sectors are under question. The situation can further deteriorate with a downtrend in economic activities. Loss of income will cause financial distress for a number of households and businesses. The housing and agriculture sector are more prone to risks of a downturn in the economy. A prolonged economic slump will put downward pressure on rents and lead to a rise in empty commercial and residential property. Similarly, agriculture is also vulnerable to a slowdown in the economy, posing risks to the banking sector. Agriculture accounts for around 13% of bank lending, of which around two-thirds is to the dairy sector.

Even though there exists considerable uncertainty about the economic outlook, stress tests conducted for banks in New Zealand suggest that banks can withstand adverse scenarios.

Since we now have a broad idea of the banking and insurance sector, it is important to look at the performance of some companies operating in the same sector (ANZ, WBC, GFL, TWR).

1. Australia and New Zealand Banking Group Limited (Recommendation: Buy, Potential Upside: Lower Double-Digit), (M-Cap: ~NZ$55.737 billion, Dividend Yield: 7.775%)

Business Description: Australia and New Zealand Banking Group Limited (NZX: ANZ) provides banking and financial products and services to individual and business customers and it operates in and across 33 markets.

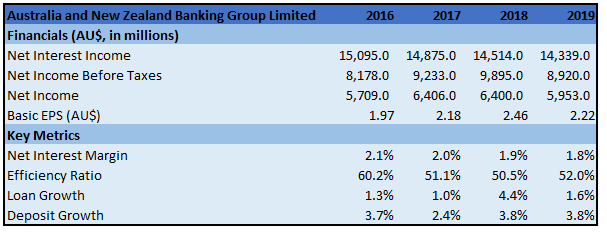

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The bank’s core businesses continued to perform well with targeted balance sheet growth in preferred segments. The bank continued its focus on running the business as efficiently as possible with business as usual costs falling again. The bank’s capital position remains strong, with a Level 2 Common Equity Tier 1 capital (CET1) ratio of 11.1% at 30 June 2020.

Key Risks: Increasing competition and regulatory requirements might impact margins and customer volumes. Demand for home lending in ANZ is impacted by a range of supply and demand factors largely outside the bank’s control, including population growth, housing prices as well as dwelling construction.

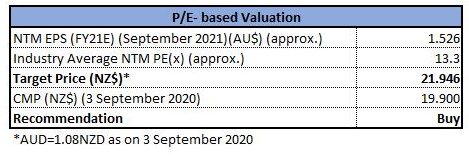

Valuation: We have applied P/E multiple based relative valuation (on an illustrative basis) and the target price reflects a rise of lower double-digit (in % terms).

P/E Based Relative Valuation (Illustrative)

P/E Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Hence, we give a “Buy” recommendation on the stock at the current market price of NZ$19.900 per share, up by 0.91% on September 3, 2020.

2. Westpac Banking Corporation (NZX: WBC) (Recommendation: Buy, Potential Upside: Lower Double-Digit), (M-Cap: ~NZ$68.11 billion, Dividend Yield: 6.43%)

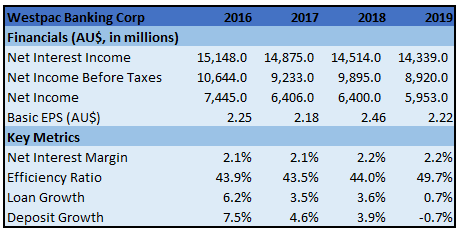

Business Description: Westpac Banking Corporation provides financial services like lending, deposit taking, payments services, investment platforms, superannuation and funds management, insurance services, leasing finance, general finance, interest rate risk management and foreign exchange services.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The most substantial impact on the bank’s performance in 1HFY20 was the COVID-19 crisis, including its effect on employees, customers, and the broader economy. The key capital ratio, the Common Equity Tier 1 capital ratio was 10.8% which, on an internationally comparable basis, places the bank in the top quartile of banks globally.

Key Risks: The bank’s business is subjected to various risks that can adversely impact its financial performance, financial condition, and future performance. The business is highly regulated, and it could be adversely affected by changes in laws, regulations, or regulatory policy.

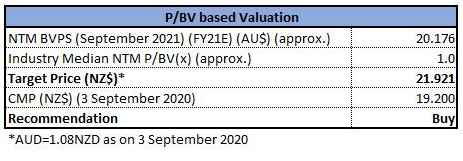

Valuation: We have applied P/BV multiple based valuation (on an illustrative basis) and the target price reflects a rise of lower double-digit (in % terms).

P/BV Based Relative Valuation (Illustrative)

P/BV Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Hence, we give a “Buy” recommendation on the stock at the current market price of NZ$19.200 per share, up by 1.69% on September 3, 2020.

3. Geneva Finance Limited (Recommendation: Buy, Potential Upside: Lower Double-Digit), (M-Cap: ~NZ$30.27 million, Dividend Yield: 6.63%)

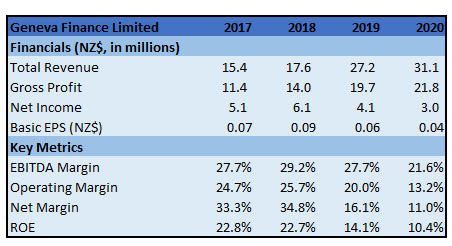

Business Description: Geneva Finance Limited (NZX: GFL) is a finance company which offers finance and financial services to the consumer credit and small to medium enterprise markets.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: FY20 was a difficult year for the company as some operations performed very well while others required restructuring to turn around performance. However, the company is now well-positioned to return to sustainable profit and revenue growth. The company has a strong balance sheet, the receivable ledger is well provisioned, and the company is ready to take advantage of the opportunities the market will offer.

Key Risks: The company is exposed to credit risk, resulting from the non-performance of a counterparty to whom funds have been advanced.

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack.

The stock has closed around 23.6% retracement level of $0.413 which has been held strongly in the past few weeks. The technical indicator RSI with around 45 reading suggests the gaining of bullish momentum.

Going forward, if the 23.6% retracement level of $0.413 is held then it might even retrace up to 38.2% retracement level of $0.459 where it may meet with strong resistance while failure to hold the aforesaid level, might drive the price down to the lower Bollinger band level of $0.387.

Valuation: The company's EV/Sales multiple stood at 1.0x as compared to industry median (Financials) of 9.2x. Also, its P/BV multiple stood at 1.0x while the industry average is 2.3x.

Hence, we give a “Buy” recommendation on the stock at the current market price of NZ$0.415 per share on September 3, 2020.

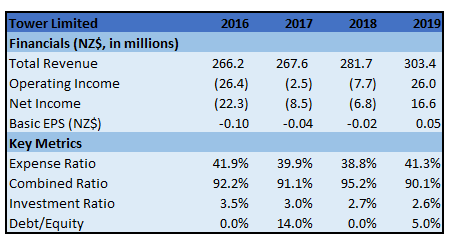

4. Tower Limited (NZX: TWR) (Recommendation: Buy, Potential Upside: Lower Double-Digit), (M-Cap: ~NZ$238.23 million)

Business Description: Tower Limited (NZX: TWR) is primarily engaged in the provision of general insurance. The company mainly operates in New Zealand with some of its operations based in the Pacific Islands region.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The company’s strategy is clearly focussed on becoming a digital challenger brand, taking on the big incumbents, and challenging industry norms. In the month of March, almost 60% of the new business came in through the company’s digital channels. The company is currently working through a process to deliver savings of $7.2 million per year. The company has updated its FY20 guidance of underlying NPAT to $25 million to $28 million.

Key Risks: The financial condition and operating results of the company are affected by a number of key financial and non-financial risks. Financial risks include market risk, credit risk, financing, and liquidity risk. The non-financial risks include insurance risk, compliance risk and operational risk.

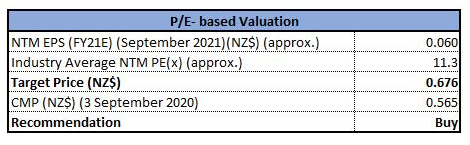

Valuation: We have applied P/E based relative valuation (on an illustrative basis) and the target price reflects a rise of lower double-digit (in % terms).

P/E Based Relative Valuation (Illustrative)

P/E Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Hence, we give a “Buy” recommendation on the stock at the current market price of NZ$0.565 per share, down by 0.88% on September 3, 2020.

Comparative Price Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...