I. Sector Landscape and Outlook

The Financial Market Infrastructure Act (FMIs) was converted into law in May 2021 which is to be implemented over an about 18 months transitional period, out of understanding that well-managed FMIs support well-functioning of financial markets and are vital for a sound and efficient financial system. The new Act governs FMIs, a set of critical systems that are occasionally referred to as the plumbing of the financial system. These systems facilitate electronic payments and financial market transactions to occur. The Reserve Bank of New Zealand and the Financial Markets Authority are together the regulators of FMIs under the Act. However, it has been realized that problems at FMIs could lead to adverse impact on financial markets, and hence, the Act provides scrutiny of FMIs and power for the regulators to intervene, if needed.

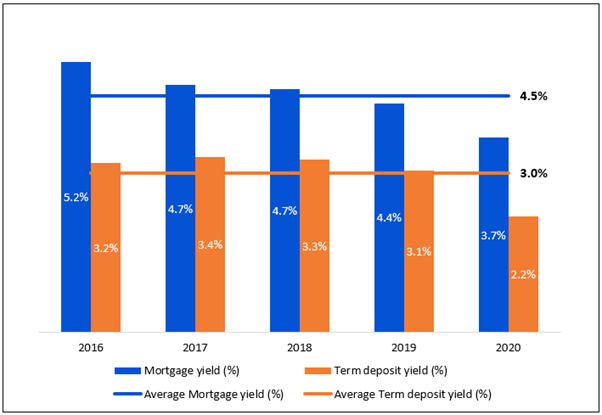

As per the Reserve Bank of New Zealand, the decrease in term deposit and mortgage rates from 2016 to 2020, other things constant, indicates a net positive income gain of 0.1% across all New Zealand households. As per the data, the average mortgage holders experienced a 1% rise in income, while nonmortgage holders realized a 0.4% fall in income. Across the people, the fall in income led by lower term deposit rates exceeded any rise in income from lower mortgage rates for the bottom three income deciles. Nearly half of these households are in the 65+ age bracket. Those in the age bracket of 25-54, gained on average 0.3% while the gross income of the older population aged 55-64 and retirees (65+) declined by 0.1% and by 0.5% respectively.

Exhibit 1: Trend in Mortgage and Term Deposit Rates since 2016

Data Source: This work is based on/includes rbnz data which is licensed by rbnz.govt for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

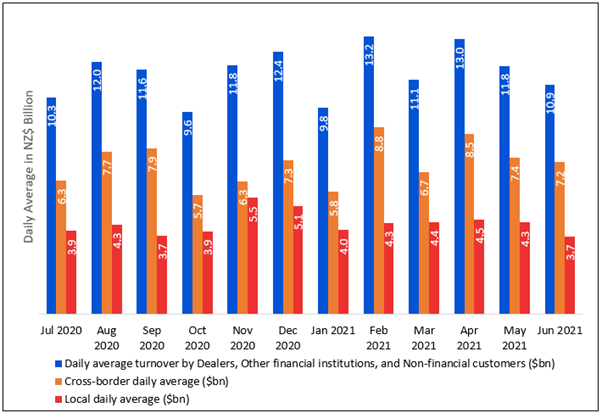

Sector Lending – Housing Lending Increased in May 2021

As per the Reserve Bank of New Zealand, the total housing lending stock grew by $3.0 billion (1.0%) in May 2021, which was identical to the rise seen in April 2021. As of May 2021, total housing lending stock stood at $314.7 billion versus $282.5 billion pcp. Meanwhile, annual growth grew by 11.4% from 11.0% seen in April 2021. However, total consumer lending fell by $39 million (-0.3%) in May 2021 after seeing an increase in April 2021. Annual growth also fell further from -2.4% in April 2021 to -3.1% in May 2021. Further, the total business lending stock saw its biggest monthly increase since March 2020, an increase of $461 million (0.4%) in May 2021, with its annual growth bettering from -5.3% in April 2021 to -3.9% in May 2021. Moreover, total agriculture lending stock increased by $196 million (0.3%) in May 2021 with annual growth from -1.5% in April 2021 to -1.2% in May 2021.

Exhibit 2: Trend in Lending Since 2017 – Banks and NBLIs

.png)

Data Source: This work is based on/includes rbnz data which is licensed by rbnz.govt for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

Strong Recovery in Foreign Exchange Turnover

As per the Reserve Bank of New Zealand, the average daily foreign exchange turnover from Spot, Forwards, Fx-Swaps, Currency Swaps, and OTC for the month of June 2021 stood at $10.9 billion. Of total turnover, spot turnover witnessed a significant increase by 78.5% over the same month last year. Broadly, the recent recovery in the financial market is an outcome of improved consumer sentiments, better economic data, controlled COVID-19 circumstances, aggressive vaccination of people, and opening of boarders.

Exhibit 3: Daily Average Foreign Exchange Turnover Trend since July 2020 to June 2021

Data Source: This work is based on/includes rbnz data which is licensed by rbnz.govt for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

Index Performance:

The S&P/NZX All Financials Index generated a 1-year return of ~42.67% versus ~9.93% by the S&P/NZX 50 Index. Therefore, S&P/NZX All Financials Index overperformed S&P/NZX 50 Index by ~32.74% in 1-year.

Exhibit 4: S&P/NZX All Financials Index vs S&P/NZX 50 Index

Source: REFINITIV

Key Risks and Challenges:

As per the release by the Reserve Bank of New Zealand dated 14 July 2021, the Monetary Policy Committee agreed to decrease the current monitory stimulatory level to control consumer price and employment over the medium-term. The Reserve Bank is expected to pause additional asset purchases under the Large-Scale Asset Purchase (LSAP) programme while keep the Official Cash Rate (OCR) at 0.25% and the Funding for Lending Programme unaffected.

Meanwhile, the Reserve Bank of New Zealand sees vulnerabilities in the financial system after successful public health measures followed by substantial monetary and fiscal policy support that prevented many business failures and a big rise in unemployment. Further, the regulator is seeing the impact of lower global interest rates resulting in the higher risk-taking appetite of the consumers and higher asset prices, most visible in higher house prices.

An elevated proportion of new lending has had increased debt-to-income and loan-to-value ratios (LVR). This impacts recent borrowers to an increase in mortgage rates and exposes households and the financial system to a decline in house prices. The recent measures in tightening LVR requirements, primarily for investor lending, will mitigate some of these housing risks and support more sustainable house prices.

Exhibit 5. Key Risks in Banking and Financial Services Sector:

Sources: Analysis by Kalkine Group

Outlook:

As per the Reserve Bank of New Zealand, the global economic outlook continues to improve, supporting New Zealand’s export prices for commodities. Global monetary and fiscal stimulus remains at balanced levels supporting the recovery in economic activity. Increased vaccination rates across countries are providing further economic support.

Moreover, recent data indicate that the New Zealand economy remains strong despite the continued impact of international border restrictions. Aggregate economic activity is above its pre-COVID-19 level. Household spending and construction activity are at elevated levels and are expected to continue to grow further. Business investment is indicating capacity pressures and labour shortages, and business sentiments continue to improve.

Apart from the sector-specific factors, we have also analysed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

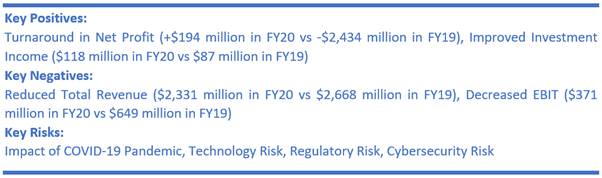

1) AMP Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$3.85 billion, Gross Dividend Yield: 9.462%)

Business Description:

Founded in 1849, AMP Limited (NZX: AMP) is a wealth management company with an accelerating retail banking business and a growing international investment management business.

Outlook:

As per the Q1FY21 AUM and cashflows update released on 22 April 2021, the business performance continued to be resilient in Q1FY21 as it makes extended progress on delivery of transformation strategy to become a simpler, client-led business. In Australia, cashflows are showing signs of improvement, with a decrease in outflows from corporate super mandates and a decreased impact from Protecting the Super legislation. The company supported clients with A$448 million in pension payments. Further, it saw an encouraging performance in AMP Bank with significant loan book growth. Further, it is focused on aligned and external financial advisers in servicing clients and ensuring it continues to be a leading platform. Importantly, the company remained focused on delivering critical priorities to progress transformation over the next quarter and continue positioning the business for future growth.

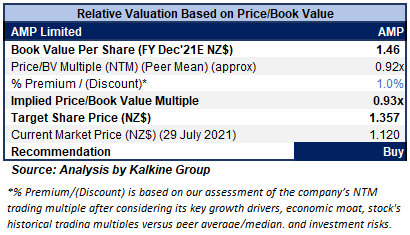

Valuation Methodology: Price/Book Value Based Relative Valuation (Illustrative)

Daily Price Chart

Source: REFINITIV

Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

We have applied Price/Book Value (P/BV) based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied a slight premium to P/BV Multiple (NTM) (Peer Average) considering the rise in Australian wealth management (AWM) assets under management (AUM) to A$125.7 billion in Q1FY21 and an increase in AMP Bank total loan book to A$20.8 billion.

For the valuation purposes, we have taken peers such as Tower Ltd. (TWR.NZ), Harmoney Corp Ltd. (HMY.NZ), and Suncorp Group Ltd. (SUN.AX) to name a few.

Considering the aforesaid facts, we give a “Buy” recommendation on the stock at the current market price of $1.12 per share, down 1.75%, on 29th July 2021.

2) Tower Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$295.15 million, Gross Dividend Yield: 3.623%)

Business Description:

Tower Limited (NZX: TWR) is a New Zealand-based insurance company that operates across New Zealand and the Pacific Islands. It is engaged in providing insurance for houses, cars, content, businesses, and more.

Outlook

As per the release dated 11 June 2021, the company received 164 claims for Canterbury floods, which is expected to cost $2.8-$3 million before tax. In the release of the H1FY21 result, the company provided guidance of underlying NPAT of $25-$27 million, forecasting FY21 large events of $9.7 million. However, driven by the occurrence of the Canterbury floods, the company now assumes FY21 large events of $14 million that are expected to result in an updated underlying NPAT guidance of $22-$24 million for FY21.

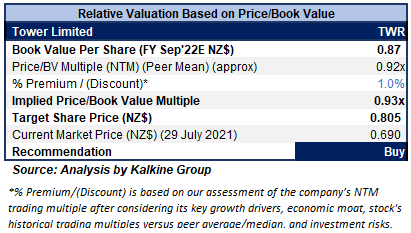

Valuation Methodology: Price/Book Value Based Relative Valuation (Illustrative)

Daily Price Chart

Source: REFINITIV

Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

We have applied Price/Book Value (P/BV) based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied a slight premium to P/BV Multiple (NTM) (Peer Average) considering business growth and ongoing reduction in management expenses.

For the valuation purposes, we have taken peers such as Harmoney Corp Ltd. (HMY.NZ), AMP Ltd. (AMP.NZ) and Suncorp Group Ltd. (SUN.AX) to name a few.

Considering the aforesaid facts, we give a “Buy” recommendation on the stock at the current market price of $0.69 per share (New Zealand Time: 11:26 AM (GMT +12) on 29th July 2021.

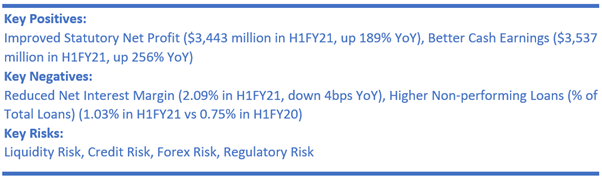

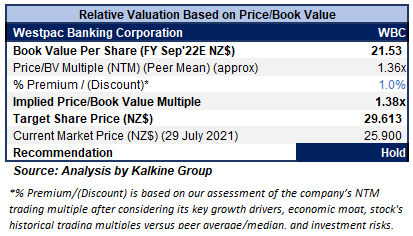

3) Westpac Banking Corporation (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$95.02 billion, Gross Dividend Yield: 3.926%)

Business Description:

Westpac Banking Corporation (NZX: WBC) is one of four major banking organizations in Australia and one of the largest banks in New Zealand. The bank offers a spectrum of consumer, business, and institutional banking and wealth management services.

Outlook

As per the management, the Australian economy is rebounding with strong consumer sentiment. Further, new lending for housing has jumped 49% over the last year, including a 75% jump from the May 2020 low. The company expects a continued increase in home prices, driven by a higher supply of houses for sale. Importantly, the company is focused on implementing its Fix, Simplify and Perform strategic priorities.

Valuation Methodology: Price/Book Value Based Relative Valuation (Illustrative)

Daily Price Chart

Source: REFINITIV

Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

We have applied Price/Book Value (P/BV) based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied a slight premium to P/BV Multiple (NTM) (Peer Average) considering improved ROE at 10.2% in H1FY21, up from 2.9% in H1FY20, and a better CET1 capital ratio of 12.34%, that grew 153 bps in H1FY21 over pcp.

For the valuation purposes, we have taken peers such as Heartland Group Holdings Ltd. (HGH.NZ), National Australia Bank Ltd. (NAB.AX) and Commonwealth Bank of Australia. (CBA.AX) to name a few.

Considering the aforesaid facts, we give a “Hold” recommendation on the stock at the current market price of $25.90 per share, down 0.46% on 29th July 2021.

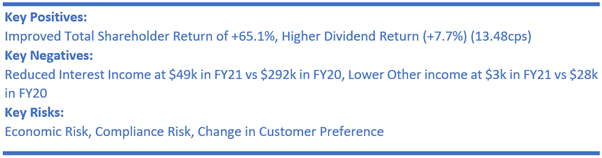

4) Kingfish Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$628.37 million, Gross Dividend Yield: 7.291%)

Business Description:

Kingfish Limited (NZX: KFL) is an investment company with a focus on growing investors' capital through portfolio management and offering regular dividends.

Outlook

As per the management, the company has reported a year of recovery after the COVID impactful performance in FY20. Its focus on investing in agile and prospering companies has again proven the benefits of active investment management and provided shareholders with robust returns. Therefore, the same strategy is expected to continue in the future period.

As per the Q1FY22 newsletter, released on 26 July 2021, the total shareholder return as of 30 June 2021 stood at +8.3%, and adjusted NAV return for the same period was reported at +1.7%.

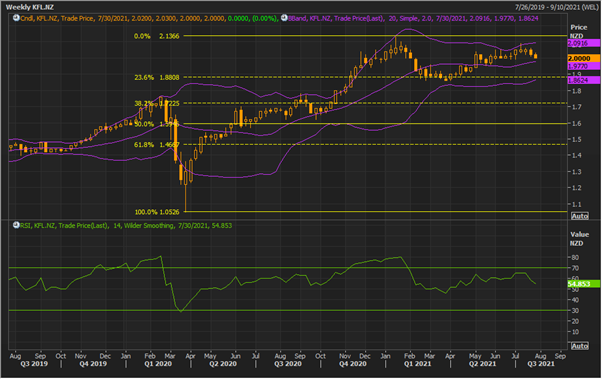

Technical Overview:

Weekly Chart –

Source: REFINITIV

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack. https://www.bollingerbands.com/

The stock has been on a winning streak for several weeks. But for the past two weeks including that of the ongoing week, it has been giving a softer close. The technical indicator RSI with a reading around 55 and a curve at the end pointing down, suggests softening of bullish momentum for the stock.

Going forward, the stock may have resistance around the upper Bollinger Band of $2.09 whereas support could be around the 23.6% retracement level of $1.68.

Stock Recommendation

Driven by the optimism by the management, rebound in market sentiments, current trading levels, and positive long-term outlook, we recommend a ‘Hold’ rating on the stock at the current market price of $2.00 per share, on 29th July 2021.

Note 1: The reference data in this report has been partly sourced from REFINITIV.

Note 2: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the analysis has been achieved and subject to the factors discussed above alongside support levels provided.

Technical Indicators Defined: -

Support: A level where-in the stock prices tend to find support if they are falling, and downtrend may take a pause backed by demand or buying interest.

Resistance: A level where-in the stock prices tend to find resistance when they are rising, and uptrend may take a pause due to profit booking or selling interest.

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...