Investment Summary:

Primary industries in New Zealand is the backbone of broader economic development, and the industry is primarily characterized by Government support, stable business policies, positive global environment and employment opportunities. Resilience of the primary industries is well-supported by the fact that the nation’s food and beverage producing sector managed to continue operating and exporting despite COVID-19 causing considerable logistics challenges along with reducing processing capacity.

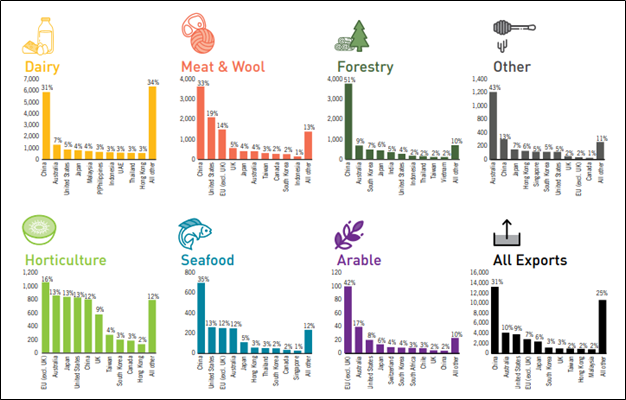

For the year ended June 2019:

Export Destinations, Year ended June 2019 (Source: SOPI)

Dairy Sector Witnessed Decent Demand Growth

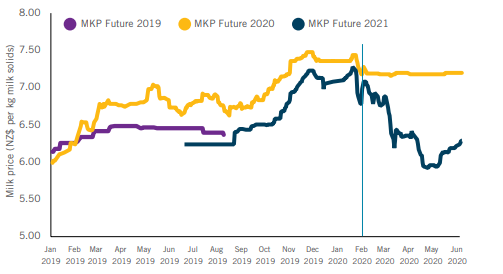

Provisional trade data published by Stats NZ reflects dairy exports were robust from 25th March to 3rd June 2020, up by $519 million as compared to same time of the last year because of strong prices supported by falling New Zealand Dollar.

Weekly milk futures prices (July 2019 to May 2020) (Source: Ministry for Primary Industries)

How Meat and Wool Support Growth of Primary Industries?

As per the latest report published by Meat Industry Association, the country exported $859 million of lamb, mutton, beef, and co-products in the month of April. While the overall value of exports was broadly similar compared to April 2019, there were changes to some major markets due to the impact of COVID-19.

Export values of both chilled sheepmeat and beef dropped compared to last April, down 35 per cent to $52.7 million for sheepmeat and 19 percent to $30.1 million for beef, reflecting the challenges of exporting perishable products during the trade disruptions caused by COVID-19.

Government’s Support Provides Further Boost to Primary Sector

New Zealand’s farmers, growers and producers are expected to play a critical role in the country’s economic recovery and, therefore, the government has decided to invest $232 million to boost jobs and opportunities in the primary sector and rural New Zealand. Budget 2020 will set the primary sector up to seize opportunities for future growth.

Government is investing $38.5 million over four years to ensure that horticulture sector can grow and stay ahead of international competitors with access to safe plant breeding material and a focus on reaching new markets.

The Government of New Zealand has declared a new $500,000 fund that will help farmers and growers prepare their businesses to recover from drought as the economy gets moving again. The fund will provide advisory services that usually cost $5000 to equip rural businesses with professional and technical advice to help them recover from and better prepare for future drought.

Key Risks Affecting Primary Industries in New Zealand

The primary sector is facing the most significant environmental issue. Critics blame the dairy industry as the main source of concern. There are also increasing concerns about the corporatization of primary production. Biosecurity is yet another area of concern for the primary industry. Coming to the impact of COVID-19 on primary industry, as per an analysis from Meat Industry Association (MIA), the monthly value of red meat and co-product exports for April was largely unchanged on pcp despite COVID-19. The industry is benefiting from strong relationships across different export markets which have allowed the industry to weather the impact.

Primary Industries in New Zealand: A Look at Growth Drivers

As we know, primary industry earns billions of dollars each year from exports. There is a strong sense about the criticality of the primary sector to the economy, as it provides employment opportunities and tax revenue. Agriculture assumes a significant position in the New Zealand economy. Year-round grass growth means pastoral farming to produce dairy products, red meat, and wool which is a highly profitable business. The country is the world’s largest exporter of wool and ship meat, whereas dairy provides billions of dollars in export earnings.

While the COVID-19 lockdowns and resulting economic impacts are the key drivers for emerging outlook for the primary industries, the fundamental sector-specific drivers will remain crucial. Underlying market factors are favourable for fresh fruit, with strong harvests boosting volumes as well as consumer demand holding up through the early period of trade disruption.

Before the outbreak, Chinese meat imports surged in 2H FY 2019, and underlying animal protein shortage behind this demand happens to be a key market driver. The African swine fever (ASF) outbreak in China as well as across Eurasia caused a large shortfall in production that cannot be addressed without large import volumes. This is expected to help support prices over next year.

New Zealand has a highly productive pastoral farming base which enables large scale milk production possible. Farming is getting supported by a temperate climate and heavy investment in land improvement. The farms support many specialized services: finance, trade, transport, building and construction, and especially, the processing of butter, cheese, and frozen lamb. The country exports wool and processed dairy products. Pastoral farming especially, dairying has remained significant, but other sectors such as forestry, horticulture, fishing, deer farming, and manufacturing has produced a more balanced economy.

Since we now have a broad overview of the primary industries in New Zealand, its time to look at some promising stocks in the same sector (PGW, SCL, TGG, SEK)

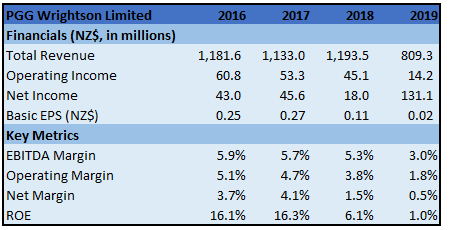

1. PGG Wrightson Limited (NZX: PGW) (Recommendation: Speculative Buy, Potential Upside: Lower Double-Digit) (M-Cap: ~NZ$202.29 Million, Gross Dividend Yield: 8.488%)

Business Description: PGG Wrightson Limited offers a wide range of products and services that allows it to be one of the key suppliers to the agricultural sector in New Zealand.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: In the month of February, the company forecasted operating EBITDA guidance of about $30 million for the financial year to 30 June 2020. However, due to the unprecedented events in recent weeks, the company has decided to withdraw its current guidance and place this under review until such time that the impact on earnings can be more accurately assessed.

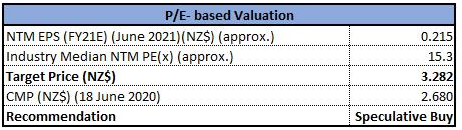

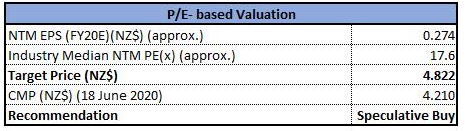

P/E Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Key Risks: The company is exposed to risks like liquidity risk, market risk (foreign currency, price and interest rate), funding and credit risk.

Valuation: The company has a strong balance sheet and has recorded a solid first half result. It played an important role in serving farmers and grower customers through the lockdown period as a provider of essential services to the agricultural sector. Based on this background and its confidence in the future, the company paid an interim dividend of 9 cents per share. We have applied P/E Based Relative Valuation (on an illustrative basis), and the target price reflects a rise of lower double-digit (in % terms).

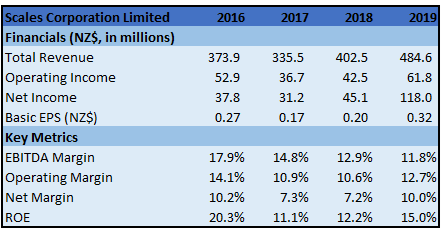

2. Scales Corporation Limited (NZX: SCL) (Recommendation: Speculative Buy, Potential Upside: Lower Double-Digit) (M-Cap: ~NZ$682.44 Million, Gross Dividend Yield: 5.386%)

Business Description: Scales Corporation Limited is a diversified agribusiness company, which comprises of three operating segments: Logistics, Horticulture and Food Ingredients.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: SCL’s business units were classified as ‘essential services’ during the period of lockdown. For the 2020 apple season, the harvest has continued with approximately 40% of the crop harvested and either in storage or shipped. Subject to market conditions, the company currently has adequate resources to cover harvest, packing, cool storage, and shipping. Whilst markets are volatile, the company continues to ship to customers all over the world.

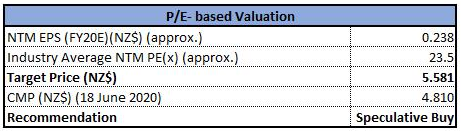

P/E Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Valuation: The 2020 apple harvest has already begun, and early crop indications are positive and in line with forecast. The Logistics and Food Ingredients segment is also operating positively. Underlying net profit guidance has been reconfirmed by the company at between $30 million and $36 million, indicating an Underlying EBITDA range between $49 million and $55 million. We have applied P/E Based Relative Valuation (on an illustrative basis) and the target price reflects a rise of lower double-digit (in % terms). However, the company is exposed to financial risks arising from changes in the climatic conditions, market prices as well as the value of the New Zealand dollar.

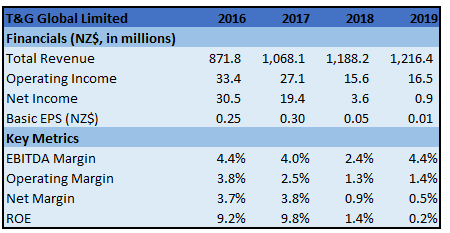

3. T&G Global Limited (NZX: TGG) (Recommendation: Speculative Buy, Potential Upside: Lower Double-Digit) (M-Cap: ~NZ$318.61 Million)

Business Description: T&G Global Limited is one of New Zealand’s largest fresh produce companies - growing, packing, shipping, marketing, and selling delicious fruit and vegetables to consumers around the world.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: T&G’s profit for the year for T&G Group (according to its statutory accounts) is expected to be between $6.0 million and $7.0 million. The improved forecast, compared to the range of $2.0 million to $4.0 million previously announced, reflects the impact of lower than anticipated provisions relating to the New Zealand Pip fruit season and improved trading conditions in December 2019. The company has received the approval to acquire the domestic business of Freshmax New Zealand. This acquisition will bring together two of the country’s top fresh produce companies, offering a superior partnership for retailers and growers. The acquisition comprises three market sites (Christchurch, Auckland, and Wellington), and it also includes distribution services all through New Zealand (Palmerston North, Auckland, and Christchurch).

Key Risks: The company is not immune to current heightened global economic risks, including the impacts of Brexit, Chinese trade negotiations, political uncertainties and, most recently, the potential effect of the coronavirus. Additionally, climatic changes and the intensity of weather events continue to test its operations.

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Green colour lines are Bollinger Bands with upper band suggesting overbought status while lower band oversold status, and yellow lines are Fibonacci retracement lines that measure price rebound and backtrack.

The stock rebounded from its low of $2.35 to 61.8% retracement level of $2.74 but it could not hold on positive momentum and has slipped near to 38.2% retracement level of $2.590 and giving close at $2.60. Technical indicator RSI with 42 reading suggests neutral momentum for the stock.

Going forward, the stock may have resistance around $2.80 while support could be around $2.50.

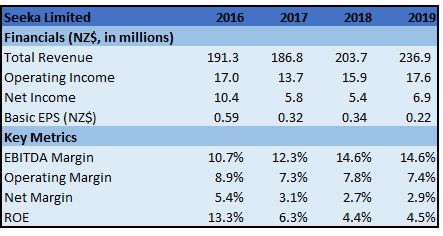

4. Seeka Limited (NZX: SEK) (Recommendation: Speculative Buy, Potential Upside: Lower Double-Digit) (M-Cap: ~NZ$135.20 Million, Gross Dividend Yield: 3.831%)

Business Description: Seeka Limited happens to be integrated horticulture and produce company which is in the business of growing, processing, distributing, and marketing high quality produce to the world markets.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The effects and costs associated with COVID 19 have been significant together with very dry growing conditions in New Zealand and Australia lowering crop volumes. The company has continued to innovate to achieve efficiencies; to continue its strategy of divesting Northland orchards; and has implemented its sale and lease back strategy in Australia. These initiatives, when completed, are expected each to positively impact profit.

P/E Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Key Risks: The company's activities expose it to a variety of risks specific to producing and selling horticultural crops, along with corporate financial risks related to credit, liquidity and capital risk.

Valuation: The company, having considered its current year performance and expecting the completion of its divestment transactions, expects earnings before tax to be in the range between $9 million and $11.0 million for the full 2020 financial year compared to $9.8 million in the previous corresponding period. We have applied P/E Based Relative Valuation (on an illustrative basis) and the target price reflects a rise of lower double-digit (in % terms).

Comparative Price Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...